Understanding the Social Security 50% Spousal Benefit

The Social Security 50% spousal benefit allows married or divorced individuals to receive up to half of their spouse’s full retirement age benefit. This guide explains eligibility rules, timing strategies, and why delaying benefits may not always maximize household income. Learn how filing decisions affect both spouses and how to coordinate benefits for optimal retirement income. Understanding these rules is essential for building an efficient Social Security strategy.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When married couples are deciding when to file for Social Security, there are several strategies to consider. One of the most important — and often misunderstood — is the 50% spousal benefit. This rule can have a major impact on when each spouse should file and how to maximize total household Social Security income over retirement.

In this article, we’ll walk through:

What the 50% spousal benefit is

Special filing rules to qualify

Why “file and suspend” is no longer allowed

Why delaying to age 70 may not always make sense

Special rules for divorced spouses

Other factors to consider when choosing a filing strategy

What Is the 50% Spousal Benefit?

When you are married and eligible for Social Security, you have the option to receive:

100% of your own Social Security benefit, or

50% of your spouse’s benefit, whichever is higher.

You do not get both — Social Security will essentially give you the higher of the two amounts.

Example

Let’s look at an example:

Paul’s Full Retirement Age (FRA) benefit: $3,600 per month

Sharon’s FRA benefit: $800 per month

When Sharon files at her full retirement age (67), she can choose:

Her own benefit: $800/month

50% of Paul’s benefit: $1,800/month

Since $1,800 is higher than $800, she would elect the 50% spousal benefit.

This filing strategy is extremely important in situations where one spouse earned significantly more than the other.

Special Filing Rules

One of the most important rules for the 50% spousal benefit is this:

The higher-earning spouse must be receiving their Social Security benefit in order for the lower-earning spouse to claim the 50% spousal benefit.

Using Paul and Sharon again:

Both are age 67

Paul’s FRA benefit = $3,600

Sharon’s FRA benefit = $800

If Paul decides to delay his Social Security until age 70, Sharon cannot collect the spousal benefit until Paul actually turns his benefit on.

So Sharon would:

Take her own benefit of $800 at 67

Elect the 50% spousal benefit when Paul turn on at age 70 increasing to $1,800

This rule alone often drives a lot of the Social Security filing decision for married couples.

File and Suspend Is No Longer Allowed

Years ago, there was a strategy called “file and suspend.”

This allowed the higher-earning spouse to:

File for Social Security

Immediately suspend their benefit

Allow their benefit to continue growing until age 70

Meanwhile, the lower-earning spouse could collect the 50% spousal benefit

This strategy was very powerful, but the Social Security Administration eliminated the file and suspend strategy. Now, the higher-earning spouse must actually be receiving benefits for the spouse to receive the spousal benefit.

Delaying Until Age 70 May Not Always Make Sense

Many people know that if you delay Social Security past full retirement age, your benefit increases by approximately 8% per year until age 70.

From an individual standpoint, delaying can make a lot of sense. However, for married couples, the spousal benefit changes the math.

Here’s the key rule:

The 50% spousal benefit is based on 50% of the higher earner’s Full Retirement Age benefit, not their age 70 benefit.

Example

Let’s go back to Paul and Sharon:

Paul’s FRA benefit: $3,600/month

Paul’s age 70 benefit: about $4,500/month

Sharon’s own benefit: $800/month

Sharon’s spousal benefit: $1,800/month (50% of $3,600)

If Paul delays until age 70:

Sharon cannot collect the spousal benefit for 3 years

Her spousal benefit does not increase — it stays at $1,800

So the couple must evaluate:

Is the increase in Paul’s benefit worth Sharon not receiving the addition $1,000/month for three years? ($1,800 spousal benefit less Sharon’s $800 FRA benefit)

In situations where the spousal benefit is a large increase for the lower-earning spouse, it may make sense for the higher earner to file earlier, even if that means giving up the delayed credits.

However, if the spousal benefit is only slightly higher than the lower earner’s own benefit, delaying may still make sense.

This is why Social Security filing decisions should always be looked at from a household strategy, not just an individual strategy.

Divorced Couples: Special Consideration

Many people don’t realize that divorced spouses may still be eligible for the spousal benefit.

You may qualify for a 50% spousal benefit on an ex-spouse’s record if:

The marriage lasted at least 10 years

You are currently unmarried

Your own Social Security benefit is less than 50% of your ex-spouse’s benefit

Your ex-spouse is eligible for Social Security (they do not have to be collecting yet if divorced more than 2 years)

Even if your ex-spouse has remarried, you may still be eligible for the spousal benefit based on their record.

Importantly:

Your ex-spouse collecting a spousal benefit does NOT reduce their benefit and does not impact their current spouse.

Other Factors to Consider When Filing for Social Security

The 50% spousal benefit is just one piece of the Social Security planning puzzle. When building a filing strategy, we also consider:

Survivor benefits

Life expectancy of both spouses

Taxation of Social Security

Other retirement income sources

Roth conversion strategy

Required Minimum Distributions (RMDs)

The difference between each spouse’s benefit

The survivor benefit is especially important — when one spouse passes away, the surviving spouse keeps the higher of the two Social Security benefits, which is another reason why delaying the higher earner’s benefit can sometimes make sense.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions About the Social Security 50% Spousal Benefit

- What is the Social Security spousal benefit?The spousal benefit allows a married spouse to receive up to 50% of their spouse's full retirement age Social Security benefit if that amount is higher than their own benefit.

- Do I get my own benefit plus 50% of my spouse's benefit?No. You receive either your own benefit or the spousal benefit - whichever is higher - but not both.

- When can I claim the spousal benefit?You can claim the spousal benefit as early as age 62, but the benefit will be reduced if taken before your full retirement age.

- Does my spouse have to file before I can receive the spousal benefit?Yes. The higher-earning spouse must be actively receiving Social Security benefits before the lower-earning spouse can claim the 50% spousal benefit.

- Is the spousal benefit based on my spouse's age 70 benefit?No. The spousal benefit is based on 50% of your spouse's full retirement age benefit, not their age 70 benefit.

- If my spouse delays until age 70, does my spousal benefit increase?No. Your spousal benefit does not increase if your spouse delays past full retirement age. However, you must wait until they file to receive it.

- Can a divorced spouse collect a spousal benefit?Yes, if the marriage lasted at least 10 years and the individual is currently unmarried, they may be eligible for a spousal benefit based on their ex-spouse's record.

- Does my ex-spouse need to be collecting for me to claim a spousal benefit?If you have been divorced for more than two years, you may be able to claim a spousal benefit even if your ex-spouse has not filed yet, as long as they are eligible.

- What happens to the spousal benefit if my spouse passes away?The spousal benefit is replaced by a survivor benefit, which allows the surviving spouse to receive up to 100% of the deceased spouse's benefit.

- How do we know when we should file for Social Security?The optimal time to file depends on several factors including life expectancy, income needs, taxes, and the difference between each spouse's benefit. This decision should be evaluated as part of a full retirement income plan.

Rules for Inheriting a Retirement Account from a Sibling

When inheriting an IRA or 401(k) from a sibling, the rules depend heavily on age difference and IRS guidelines under the SECURE Act. This article explains the 10-year rule, Eligible Designated Beneficiary exception, and Required Minimum Distribution requirements. It also outlines tax-efficient withdrawal strategies for both pre-tax and Roth accounts. Understanding these rules can help reduce taxes and maximize long-term value.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When you inherit a retirement account , whether it’s a 401(k), Traditional IRA, or Roth IRA, the rules depend heavily on who you inherited the account from. The rules for inheriting a retirement account from a sibling are very different from inheriting from a spouse, parent, or grandparent, and the distribution rules can have major tax consequences if not handled properly.

In this article, we’re going to walk through the key rules and planning strategies, including:

The 10-year rule for inherited retirement accounts

The age exception for siblings within 10 years

Required Minimum Distribution (RMD) rules

Tax strategies for inherited IRAs and 401(k)s

The 10-Year Rule

The IRS changed the rules for inherited retirement accounts starting in 2020 under the SECURE Act. For most non-spouse beneficiaries, inherited retirement accounts are now subject to the 10-year rule, which means the account must be fully depleted by the end of the 10th year following the year of death.

However, there is an important exception that often applies to siblings.

The Age Exception for Siblings

If you inherit a retirement account from a sibling and you are within 10 years of their age, you may qualify for the Eligible Designated Beneficiary exception. This allows you to use the old stretch IRA rules, instead of the 10-year rule.

This means:

You are not required to empty the account within 10 years

You are required to take annual RMDs based on your life expectancy

The account can continue to grow tax-deferred over your lifetime

Example

Let’s say:

Sue is age 50

Brian is her brother, age 45

Brian inherits Sue’s IRA

Because Brian is within 10 years of Sue’s age, he qualifies for the exception and can stretch distributions over his lifetime instead of following the 10-year rule.

He must begin taking Required Minimum Distributions (RMDs) starting the year after Sue passes away, but he is not forced to liquidate the entire account within 10 years.

Confusion With RMD Rules

This is one of the biggest areas of confusion for sibling beneficiaries.

There are two different sets of rules depending on whether the sibling qualifies for the within 10 year of age rule or not.

Situation 1: Sibling Within 10 Years of Age (Stretch Rules Apply)

If the sibling beneficiary is within 10 years of the person who passed away:

They are using the stretch IRA rules

They must take RMDs every year

RMDs begin the year after death

RMDs are calculated using the IRS Single Life Expectancy Table

They are not required to empty the account within 10 years

This is true regardless of whether the person who died had started RMDs or not.

This is where many people get confused. Under the old stretch rules, RMDs were always required for inherited IRAs, unless the beneficiary was a spouse.

Situation 2: Sibling More Than 10 Years Younger or Older (10-Year Rule Applies)

If the sibling is more than 10 years apart in age, they do not qualify for the exception and are subject to the 10-year rule.

Example:

Tim is age 55

His sister Jen is age 42

Jen inherits Tim’s IRA

Because the age difference is greater than 10 years, Jen must fully deplete the account within 10 years.

Now here’s where RMD rules depend on the age of the person who passed away:

If the person who passed away was not RMD age (under age 73) → No annual RMDs required, but account must be emptied by year 10.

If the person who passed away was already taking RMDs → The beneficiary must continue taking annual RMDs during the 10-year period.

Tax Strategies for Siblings Inheriting Retirement Accounts

This is where planning becomes very important, especially for siblings subject to the 10-year rule.

Strategy for Inherited Pre-Tax IRA or 401(k)

Distributions from inherited pre-tax retirement accounts are taxable income.

If you wait until year 10 and withdraw the entire account at once, that could push you into a very high tax bracket.

So in many cases, it may make sense to:

Take distributions gradually over the 10 years

Spread the tax liability over multiple years

Coordinate withdrawals with lower-income years

Take more in years where income is lower (retirement, job change, etc.)

Strategy for Inherited Roth IRA

If a sibling inherits a Roth IRA and is subject to the 10-year rule:

The account grows tax-free

Withdrawals are tax-free

The strategy is often to wait until year 10 and withdraw the account at the last possible moment to maximize tax-free growth

So the strategy is often:

Pre-tax account → Spread withdrawals out

Roth account → Wait as long as possible

Advanced Tax Strategy: The “Tax Bracket Wash” Strategy

There is also a more advanced strategy for individuals who are still working and inheriting a pre-tax retirement account.

If someone:

Takes a distribution from an inherited IRA (taxable)

Then increases their pre-tax contributions to their employer retirement plan (401(k), 403(b), etc.)

They may be able to offset the taxable income from the inherited IRA distribution with the tax deduction from increasing their pre-tax contributions.

In simple terms, they are:

Taking money out with one hand and putting money back into a retirement account with the other hand, while potentially neutralizing the tax impact.

This can be a very effective strategy for high-income earners who are not already maxing out their employer retirement plans.

Summary

When inheriting a retirement account from a sibling, the most important factor is the age difference between the siblings.

There are two main categories:

If Siblings Are Within 10 Years of Age:

Eligible Designated Beneficiary

Can use the stretch IRA rules

Must take annual RMDs

Do not have to empty the account within 10 years

If Siblings Are More Than 10 Years Apart:

Subject to the 10-year rule

Must empty the account within 10 years

May or may not have to take annual RMDs depending on the age of the sibling who passed away

Because inherited retirement accounts can have significant tax consequences, beneficiaries should strongly consider working with a financial advisor and tax professional to determine the best withdrawal strategy.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions

-

Do siblings have to follow the 10-year rule when inheriting an IRA?Only if they are more than 10 years apart in age.

-

What happens if siblings are within 10 years of age?They can stretch distributions over their lifetime and take RMDs each year.

-

When do RMDs start for stretch rule inherited IRAs?Typically starting the year after the original owner passes away.

-

Do I have to take RMDs if I'm subject to the 10-year rule?It depends on whether the person who passed away had started RMDs.

-

Are inherited IRA distributions taxable?Yes, if it is a pre-tax IRA or 401(k).

-

Are inherited Roth IRA distributions taxable?No, Roth IRA distributions are typically tax-free.

-

Should I take money out each year or wait until year 10?It depends on your tax bracket and whether the account is pre-tax or Roth.

-

What is the stretch IRA rule?It allows beneficiaries to take RMDs over their lifetime instead of emptying the account in 10 years.

-

Can I reduce taxes from an inherited IRA?Yes, by spreading distributions over multiple years, waiting until lower income years to process distributions, or coordinating with retirement plan contributions.

-

Should I talk to a financial advisor about inherited retirement accounts?Yes, because the withdrawal strategy can significantly impact how much tax you pay.

Self-Employment Side Hustle? Benefits of a Solo 401(k) Plan

A Solo 401(k) offers business owners and side hustlers a powerful way to reduce taxable income and accelerate retirement savings. This guide explains contribution limits, tax strategies, and how to choose between pre-tax and Roth contributions in 2026. Learn how to build a tax-efficient retirement plan and potentially eliminate income taxes on self-employment income. Discover why Solo 401(k) plans can outperform SEP IRAs in many cases.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Today, more and more individuals have side hustles in addition to their main W-2 jobs. Others may be full-time business owners but only generate a modest amount of self-employment income. In both cases, one of the most powerful retirement and tax planning tools available is the Solo 401(k) plan.

In this article, we’re going to walk through some of the tax strategies and wealth accumulation strategies we use with clients who have self-employment income and may benefit from a Solo 401(k). Specifically, we’ll cover:

What a Solo 401(k) plan is

How a Solo 401(k) can reduce tax liability

How to use a Solo 401(k) to build a larger Roth bucket

How to decide between pre-tax vs. Roth contributions

What happens when the Solo 401(k) is terminated

What Is a Solo 401(k) Plan?

A Solo(k) plan, also called an Individual(k), is a retirement plan designed for owner-only businesses. This means the business cannot have any full-time employees working more than 1,000 hours per year, other than the owner and possibly their spouse.

Because these plans only cover the business owner, they are typically simple to administer, often have little to no administrative costs, and still provide the full benefits of a traditional 401(k) plan.

Solo 401(k) plans include:

Pre-tax employee deferrals

Roth employee deferrals

Employer contributions

Potential 401(k) loan provisions

Contribution Limits (2026)

Solo 401(k) plans allow for relatively high contribution limits. For 2026:

Employee deferral limit: $24,500 (under age 50)

Age 50+ catch-up: $32,500 total deferral

Employer contribution: Up to 20% of net self-employment income (sole proprietor/partnership)

S-Corp employer contribution: Up to 25% of W-2 wages

Example

Let’s say a sole proprietor generates $40,000 in net self-employment income and is under age 50.

They could contribute:

$24,500 as an employee deferral

$8,000 as an employer contribution (20% of $40,000)

That’s a total of $32,500 going into a retirement account from just $40,000 of side hustle income.

That’s a powerful savings and tax planning opportunity.

Reducing Tax Liability

One of the primary reasons business owners establish Solo 401(k) plans is to reduce their overall tax liability.

If someone has:

W-2 income: $200,000

Self-employment income: $40,000

That self-employment income gets stacked on top of their W-2 income and may be taxed at a high marginal tax rate.

However, if that business owner contributes $30,000 of that $40,000 into a Solo 401(k) using pre-tax contributions, they may only pay income tax on $10,000 instead of the full $40,000.

That can result in significant tax savings.

Solo(K) Plans Can Potentially Eliminate Federal & State Income Taxes

If a business owner has less than the annual employee deferral limit in net income, they may be able to defer 100% of their self-employment income into the Solo 401(k).

Example:

Net self-employment income: $20,000

Employee deferral limit: $24,500

Since the income is lower than the limit, they could defer the entire $20,000 pre-tax, avoiding federal and state income tax on that income.

Note: They still must pay self-employment tax, but they can avoid income tax on that portion.

Building a Larger Roth Bucket

Another major benefit of a Solo 401(k) is the ability to build Roth retirement assets, which can be extremely valuable long-term.

Roth contributions are made after-tax, but:

The money grows tax-deferred

Withdrawals after age 59½ are tax-free

One major advantage of a Roth Solo 401(k) is:

There are no income limits for Roth 401(k) contributions.

This is very important because many high-income earners are phased out of Roth IRA contributions, but they can still contribute to a Roth Solo 401(k).

Example

Imagine a 29-year-old business owner with a side hustle contributing $24,500 per year to a Roth Solo 401(k). The money grows tax-deferred for 30 years and then all of the earning in the account can be withdrawn tax free after age 59½.

We also see this strategy used for retirees who do consulting work. If someone is 65+ and earning self-employment income but doesn’t need the income, they can contribute to a Roth Solo 401(k) and move that money into a tax-free growth bucket instead of a taxable brokerage account.

This can be a powerful long-term tax strategy regardless of age of the business owner.

To Roth or Not to Roth?

Remember, there are two types of contributions to a Solo 401(k):

1. Employee Deferral → Can be Pre-Tax or Roth

2. Employer Contribution → Typically Pre-Tax

For sole proprietors and partnerships:

Employer contribution = 20% of net earned income

For S-Corps:

Employer contribution = 25% of W-2 wages

Important: Only W-2 wages count — not S-Corp distributions

While SECURE Act 2.0 opened the door for Roth employer contributions, we are still waiting on full IRS guidance for this to be widely implemented in Solo 401(k) plans. So for now, employer contributions are generally still pre-tax, while employee deferrals can be Roth or pre-tax.

General Rule of Thumb

You might consider:

Pre-tax contributions if you are in a high tax bracket today

Roth contributions if you are in a lower tax bracket today or want tax-free income later

This is where tax planning and coordination with a financial advisor and CPA becomes very important.

What Happens When the Solo 401(k) Is Terminated?

Eventually, the self-employment income may stop. When that happens, the Solo 401(k) is typically terminated, and the assets are rolled into IRAs.

Typically:

Pre-tax Solo 401(k) money → Traditional IRA

Roth Solo 401(k) money → Roth IRA

The money can then continue growing in those IRA accounts, and the Solo 401(k) plan is closed.

Working With an Advisor Who Understands Solo 401(k) Plans

Solo 401(k) plans are extremely powerful, but there are important rules and nuances business owners must be aware of.

For example:

If you hire employees, you may have to discontinue the plan

Plan documents must be set up properly

Once plan assets exceed $250,000, you must file Form 5500 annually

There are coordination issues between your CPA and financial advisor

You must choose between pre-tax vs. Roth strategies

You must compare Solo 401(k) vs. SEP IRA vs. SIMPLE IRA

Because of these moving parts, it’s important to work with an advisor who understands how to design and manage Solo 401(k) plans properly as part of an overall financial and tax strategy.

Our firm offers free consultations for business owners and individuals with side hustle income who want to evaluate whether a Solo 401(k) plan makes sense for their situation. If you’d like help determining whether this strategy is right for you, we’d be happy to help you build a plan around your specific goals. Feel free to schedule your complementary consult via our website.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions About Solo 401(k) Plans

-

Who qualifies for a Solo 401(k)?Business owners with no full-time employees working more than 1,000 hours per year.

-

Can I have a W-2 job and a Solo 401(k)?Yes. As long as you have self-employment income, you can open a Solo 401(k) for that income.

-

How much can I contribute to a Solo 401(k)?In 2026, employee deferrals are $24,500 (under 50), plus employer contributions up to 20% of income (or 25% of W-2 wages for S-Corps).

-

Can I contribute 100% of my side hustle income?Yes, if your income is below the employee deferral limit, you may be able to defer the entire amount.

-

Do Solo 401(k) contributions reduce taxes?Yes, pre-tax contributions reduce your taxable income.

-

Can I make Roth contributions to a Solo 401(k)?Yes, employee deferrals can be Roth, with no income limits.

-

What happens when I stop my side hustle?The Solo 401(k) is typically rolled into a Traditional IRA and/or Roth IRA.

-

Is a Solo 401(k) better than a SEP IRA?In many cases, yes, because it allows Roth contributions and higher contributions at lower income levels.

-

Do I have to file anything for a Solo 401(k)?Once the account exceeds $250,000, you must file Form 5500 annually.

-

Can I take a loan from a Solo 401(k)?Some Solo 401(k) plans allow participant loans, similar to traditional employer 401(k) plans.

What Causes the Price of Gold to Go Up and Down?

Gold prices are influenced by several key factors, including interest rates, inflation, and the strength of the U.S. dollar. While gold is often viewed as a safe haven, it can be highly volatile and may not perform as well as stocks over the long term. This article explains what causes gold to rise and fall, how it compares to other commodities, and how it can be used for diversification. Understanding these drivers can help investors make more informed decisions about including gold in their portfolio.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Over the last few years, gold has experienced a significant rally, followed by periods of sharp volatility—including some recent price declines that have caught investors’ attention. As a result, we’ve been having more frequent conversations with clients about what actually causes gold prices to rise and fall, and whether a recent dip represents an opportunity or a warning sign.

In this article, we’re going to walk through the same conversations we’ve been having with clients and explain the major variables that impact the price of gold. Specifically, you’ll learn:

Why gold is often viewed as a safe haven

How the value of the U.S. dollar affects gold prices

Why interest rates play a major role in gold movements

Whether gold is a good long-term investment

How gold compares to other commodities like silver, copper, and platinum

How gold can fit into a diversified portfolio

Gold as a Safe Haven

Gold is often referred to as a “safe haven” asset. What that means is when there is volatility in the global economy—or sometimes in the U.S. stock market—investors may sell riskier assets like stocks and move money into gold in an attempt to protect their principal.

In certain periods in history, this strategy has worked well. When markets become unpredictable, gold can hold its value or even increase while stocks are falling.

However, investors need to be careful with the idea of gold as a safe haven. While gold is sometimes viewed as a “safer” asset than stocks, it is still a very volatile asset class. It is not unusual for gold to move more than 10% in a short period of time. That’s a big difference compared to bonds, which are also considered conservative investments but typically experience much smaller price swings over short time periods.

So while gold can sometimes be a successful safe haven during global volatility, investors must remember that gold itself can be volatile. It should be viewed as a portfolio diversifier, not a guaranteed protection strategy.

Inverse Relationship to the Value of the Dollar

Historically, gold has had an inverse relationship with the value of the U.S. dollar.

In simple terms:

When the dollar goes down, gold tends to go up

When the dollar goes up, gold tends to go down

Why does this happen?

If paper currency is losing value (purchasing power), investors often move money into physical assets like gold to preserve wealth. Gold is viewed as a store of value that cannot be printed or created like paper money.

On the flip side, when the dollar is strengthening and purchasing power is increasing, investors may feel less need to hold gold, which can lead to falling gold prices.

So historically speaking, movements in the dollar are one of the biggest drivers of gold prices.

Interest Rate Fluctuations

Interest rates are another major factor that influences gold prices, largely because of their relationship with the value of the dollar.

Typically:

When the Federal Reserve lowers interest rates, the dollar often weakens, and gold may rise

When the Federal Reserve raises interest rates, the dollar often strengthens, and gold may fall

One of the primary reasons attributed to gold's rapid appreciation over the last year was due to interest rates coming down, which weakened the dollar and pushed gold prices higher.

Looking forward, if inflation continues to cool and interest rates decline later into 2026 (outside of the recent Iran events), gold could recover much of what was lost in recent weeks. However, investors must also be aware of long-term inflation risks. If inflation rises again and the Federal Reserve is forced to increase interest rates, that could strengthen the dollar and become a major headwind for gold prices.

In many ways, rising interest rates can be one of the biggest enemies of gold.

Gold as a Long-Term Investment

When we look at long-term annualized returns, gold has not historically been a great long-term investment compared to stocks. Over 20- and 30-year periods, the S&P 500 has outperformed gold.

However, that does not mean gold has no place in a portfolio.

Gold can be useful for:

Diversification

Protection during market volatility

Hedging against a declining dollar

Hedging against certain inflationary environments

Gold tends to have lower correlation to stocks and bonds, which means it doesn’t always move in the same direction as traditional investments. Because of that, gold can be a useful component within a diversified portfolio, but investors should be cautious about allocating too much to gold due to its volatility and lower long-term expected returns compared to equities.

Gold Compared to Other Commodities

Clients will often ask: why gold instead of silver, platinum, or copper?

The main reason is predictability.

Gold is primarily viewed as a store of wealth. Its price is largely influenced by:

The value of the dollar

Interest rates

Inflation

Global uncertainty

Central bank policies

However, other metals like silver, platinum, and copper have significant industrial uses. That means their prices are influenced not just by currency and global events, but also by:

Manufacturing demand

Technology demand

Construction activity

Supply chain issues

More variables typically mean more unpredictable price movements.

There are years when gold performs very well and other metals do not, and there are also years where metals like copper or silver outperform gold. In investment management, we often give extra weight to assets that are easier to analyze and understand.

Special Disclosure

This article is meant to educate investors on the price fluctuations in gold based on our experience in investment management over the past number of years. This is not a recommendation to buy or sell gold or any other commodity. Every investor’s situation is different, and decisions should be made based on your individual financial plan, time horizon, and risk tolerance.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions About Gold

-

Why does gold go up when the market goes down?Gold is often viewed as a safe haven, so investors sometimes move money into gold during stock market volatility.

-

What is the biggest factor that affects gold prices?The value of the U.S. dollar and interest rates are two of the biggest drivers of gold prices.

-

Does gold go up when inflation rises?Often it does, because gold is viewed as a store of value when purchasing power declines.

-

Why does gold fall when interest rates rise?Rising interest rates typically strengthen the dollar, which historically puts downward pressure on gold.

-

Is gold a good long-term investment?Historically, stocks have outperformed gold over long periods, but gold can still be useful for diversification.

-

Is gold safer than stocks?Not necessarily, gold is still a very volatile asset class.

-

Why not invest in silver or copper instead of gold?Those metals have industrial uses, which makes their prices more unpredictable compared to gold.

-

How much gold should be in a portfolio?It depends on the investor, but many diversified portfolios only allocate a small percentage to gold (under 15%).

-

What causes gold to drop quickly?A rising dollar, rising interest rates, or reduced global uncertainty can all cause gold prices to fall.

-

Is a drop in gold a buying opportunity?It depends on the reason for the drop. Investors should look at interest rates, the dollar, and global conditions before making a decision.

The Hidden Tax Problem in the FIRE Movement (and How to Fix It)

Many FIRE investors overuse tax-deferred accounts without realizing the long-term consequences. Learn how to avoid this common tax trap and build a more flexible early retirement strategy.

The Financial Independence, Retire Early (FIRE) movement has inspired countless professionals to save aggressively, invest efficiently, and exit the workforce decades ahead of schedule. But there’s one tax mistake many FIRE followers don’t recognize until it’s too late: overloading their savings in tax-deferred accounts.

By focusing too heavily on 401(k)s and traditional IRAs, early retirees often create a tax trap that limits flexibility before age 59½ and exposes them to higher tax bills later in life. Here’s what that mistake looks like—and how strategic balance can prevent it.

How the FIRE Tax Trap Happens

The FIRE community is built on discipline: save 50–70% of income, invest consistently, and let compounding do the rest. The problem is where those savings go. Many early retirees direct most of their contributions into pre-tax accounts to minimize taxes today—but that strategy can backfire once they stop working.

Here’s why:

Withdrawals from traditional 401(k)s and IRAs are fully taxable as ordinary income.

You generally can’t access these funds before age 59½ without penalties (unless you use special exceptions).

After reaching age 73, you must start taking required minimum distributions (RMDs), which can trigger higher brackets and Medicare surcharges later.

As a result, someone retiring at 45 may find most of their wealth locked inside accounts they can’t touch for 15 years—unless they want to pay a 10% early withdrawal penalty.

At Greenbush Financial Group, we have seen FIRE followers realize this only after leaving the workforce—when their living expenses suddenly need to come from taxable or penalty-free sources they don’t have.

The Hidden Cost of Being “Too Tax-Deferred”

In the early accumulation years, it feels great to lower your tax bill with pre-tax contributions. But down the road, the strategy flips. You may have built a seven-figure retirement account, yet each withdrawal comes out as taxable income.

Example:

Imagine a 45-year-old who retires with $1.5 million, all in a traditional 401(k). They need $60,000 per year to live on. Every dollar they withdraw is taxed as ordinary income. Even at a modest 22% bracket, that’s over $13,000 in annual federal taxes—without counting state taxes or future rate increases.

The bigger the pre-tax balance, the larger the future tax burden becomes. What feels like “saving on taxes” during the accumulation phase often becomes deferring a much larger tax bill into your 50s, 60s, and 70s.

What You Should Do Instead

The key is diversification—not just by asset class, but by tax treatment.

Here’s how FIRE investors can fix or prevent the mistake:

Build a Roth bucket early.

Contribute to Roth IRAs or make Roth 401(k) contributions if your income allows. Qualified Roth withdrawals are tax-free in retirement.Create a taxable bridge account.

Invest in a regular brokerage account for flexibility. Long-term capital gains and qualified dividends are taxed at lower rates—and you can access this money anytime.Plan Roth conversions strategically.

After leaving work but before Social Security or RMDs begin, your income may temporarily drop. That’s an ideal time to convert pre-tax assets to Roth at lower brackets.Use the 72(t) rule cautiously.

The IRS allows early withdrawals from IRAs using Substantially Equal Periodic Payments (SEPPs), but they’re inflexible and complex. We usually recommend using this only as a last resort.Think long-term tax balance.

The goal is to retire with assets spread across three types of accounts—pre-tax, Roth, and taxable—so you can manage your income (and taxes) in any given year.

Our analysis at Greenbush Financial Group shows that households with this “three-bucket” approach could save hundreds of thousands in lifetime taxes compared to those with all assets tied up in pre-tax accounts.

What to Watch Out For

Even within the FIRE community, not all withdrawal strategies are equal. Watch for these pitfalls:

Underestimating future tax brackets – Low brackets today don’t guarantee low brackets later. Once RMDs and Social Security start, taxable income can spike.

Neglecting ACA subsidies – For those buying health insurance through the Affordable Care Act, high pre-tax withdrawals can disqualify you from premium tax credits.

Ignoring Roth conversion windows – The best time to convert is usually the first few years after leaving work, before other income streams begin.

The Bottom Line

Reaching financial independence takes planning, discipline, and sacrifice—but staying financially independent requires thoughtful tax strategy. The biggest mistake FIRE followers make is deferring too much for too long, only to face tax inflexibility later.

By intentionally building a mix of pre-tax, Roth, and taxable assets, you can control when and how you pay taxes, keeping more of your hard-earned savings over a lifetime of early retirement.

If you’re pursuing financial independence or considering an early retirement, our advisors at Greenbush Financial Group can help you run detailed tax projections and withdrawal strategies to help your FIRE plan burn bright without burning through your savings.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: FIRE Movement Tax Planning

-

Why is relying only on a traditional 401(k) risky for early retirees?Because you can't access most of those funds without penalties until 59 1/2, and every withdrawal is taxable as income.

-

How can I access retirement savings early without penalty?Use taxable brokerage accounts, Roth contributions (not earnings), or the 72(t) rule for limited access.

-

Are Roth IRAs better for early retirement (pre-59 1/2)?Yes. Withdrawals are tax-free, and contributions can be withdrawn anytime, offering flexibility.

-

What's a good account mix for FIRE planning?A balanced approach-roughly one-third pre-tax, one-third Roth, one-third taxable-provides strong tax diversification.

-

Can Roth conversions help early retirees?Absolutely. Converting pre-tax funds during low-income years can reduce lifetime taxes and future RMDs.

The SECURE Act 10-Year Rule Explained: Higher Taxes for Kids Who Inherit IRAs

The SECURE Act 10-year rule forces heirs to withdraw inherited retirement accounts faster, often increasing taxes. Learn how it works and strategies to reduce the impact on your family.

When Congress passed the SECURE Act, one of the most significant changes for families came from the new 10-year rule for inherited IRAs. The rule eliminated the ability for most non-spouse beneficiaries, especially adult children, to stretch required distributions over their lifetime. Now, they must empty the account within 10 years of inheriting it.

While this might sound simple, the tax impact can be severe. Compressed distribution windows often push heirs into higher brackets, accelerating income tax on decades of savings. Here is what the rule actually requires and how strategic planning can reduce the hit.

What the SECURE Act’s 10-Year Rule Says

Under the SECURE Act, when a child or other non-spouse inherits an IRA or 401(k), they must withdraw all funds by December 31 of the 10th year following the account owner’s death.

Before 2020, many beneficiaries could stretch required minimum distributions over their own life expectancy, sometimes 30 years or more, allowing continued tax-deferred growth. The SECURE Act ended that option for most heirs.

The result is that your kids will likely pay taxes on inherited retirement funds faster, and at potentially higher marginal rates, than they would have under the old rules.

Who the Rule Applies To

The 10-year rule applies to most non-spouse beneficiaries, but there are exceptions.

The rule applies to:

• Adult children or grandchildren

• Siblings, nieces, nephews, or other non-spouse heirs

• Trusts named as beneficiaries unless they qualify as see-through trusts

The rule does not apply to:

• Surviving spouses

• Minor children until they reach age 21, when the 10-year clock starts

• Disabled or chronically ill beneficiaries

• Beneficiaries less than 10 years younger than the account owner

The Hidden Tax Trap

For many families, the problem is not just the loss of tax deferral. It is the timing of the withdrawals. Most heirs inherit these accounts in their 40s or 50s, right in their peak earning years. Adding large inherited IRA distributions on top of salary and bonuses can easily push them into higher tax brackets.

Example:

If your child earns $120,000 per year and inherits a $1 million traditional IRA, they have just 10 years to withdraw it. Even spreading it evenly means an extra $100,000 in taxable income per year, enough to move them into a much higher bracket and increase Medicare or Net Investment Income taxes if applicable.

Our analysis at Greenbush Financial Group shows that this compression effect often results in 5 to 10 percent higher effective tax rates on inherited IRA dollars compared to pre-SECURE Act rules.

Planning Strategies to Reduce the Impact

There are several ways to mitigate the 10-year rule’s tax impact:

Roth conversions during your lifetime

Converting pre-tax IRAs to Roths allows your children to inherit tax-free assets. They will still follow the 10-year withdrawal rule, but distributions will be tax-free.Strategic beneficiary designations

Leave portions of retirement assets to lower-income heirs or to charitable remainder trusts.Staggered inheritances

Use taxable accounts, life insurance, or non-retirement assets to balance out future income for your kids.Pre-death withdrawals

Taking larger distributions during your own lower-income retirement years can smooth taxes across generations.Trust planning

Review existing conduit trusts. Many written before 2020 no longer operate as intended under the 10-year rule.

At Greenbush Financial Group, we often run multi-scenario tax projections showing how different withdrawal schedules, Roth conversions, or charitable strategies affect heirs’ long-term tax burdens.

Why This Matters for Your Estate Plan

The 10-year rule changed how retirement wealth passes between generations. What used to be a slow, tax-efficient transfer can now create a rapid, high-tax inheritance event.

Updating your beneficiary designations, estate documents, and withdrawal strategy is critical if you want your children to keep more of what you have saved. Even a modest Roth conversion plan or trust revision can reduce total taxes by hundreds of thousands of dollars over time.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: SECURE Act 10-Year Rule

-

Do my kids have to take money out every year?Maybe. Annual required minimum distributions may be required if the decedent was of RMD age at passing. The RMD amount is likely less than one tenth of the account. The beneficiaries must still empty the inherited IRA by the end of year 10, so creating a strategy to reduce the overall tax burden is recommended.

-

Does the 10-year rule apply to Roth IRAs?Yes, but Roth withdrawals are tax-free. Heirs still need to empty the account within 10 years.

-

How does this affect trusts as IRA beneficiaries?Many conduit trusts written before 2020 now force the entire balance out in year 10, losing the intended protection and control. These should be reviewed.

-

Can I avoid the 10-year rule for my kids?Not directly, unless your child qualifies as an eligible beneficiary such as a minor or disabled dependent. Strategic Roth conversions or life insurance can help achieve similar goals.

-

Should I change my IRA beneficiaries now?Possibly. If your current structure assumed lifetime stretch distributions, it is time to review it under the new law.

Borrowing from Your 401(k)? One Wrong Move Could Trigger a Massive Tax Bill

Borrowing from your 401(k) may seem simple, but one mistake, like leaving your job, can trigger taxes, penalties, and long-term damage to your retirement savings. Understanding the rules before you borrow is critical.

Borrowing from your 401(k) might seem like an easy way to access cash, no credit check, low interest, and you’re paying yourself back. But one wrong move can trigger immediate taxes, penalties, and a permanent hit to your retirement savings. The IRS has strict rules on how 401(k) loans must be repaid and what happens if you leave your job before it’s paid off. Understanding those rules before you borrow can help you avoid costly surprises.

How 401(k) Loans Work

Most employer-sponsored 401(k) plans allow participants to borrow up to the lesser of $50,000 or 50% of their vested balance. Loans typically have to be repaid within five years through automatic payroll deductions, and the interest you pay goes back into your account.

On paper, it looks simple. You’re borrowing from yourself and putting the money back over time. But the biggest risk comes if your employment status, or repayment schedule, changes.

The Costly Mistake: Leaving Your Job Before Repayment

If you leave your employer, voluntarily or otherwise, with an outstanding 401(k) loan, the clock starts ticking. Under IRS rules, you must repay the entire remaining balance by the tax-filing deadline of the following year.

If you don’t repay it in time, the IRS classifies the unpaid balance as a “deemed distribution.” That means:

The outstanding amount is treated as taxable income in that year.

If you’re under age 59½, you’ll also face a 10% early withdrawal penalty.

Example:

If you owe $20,000 on a 401(k) loan when you change jobs and don’t repay it, that $20,000 becomes taxable income. Assuming a 22% federal bracket, you’ll owe $4,400 in federal tax, plus a $2,000 early withdrawal penalty—a total of $6,400 lost instantly.

Our analysis at Greenbush Financial Group shows that many borrowers underestimate this risk, particularly if they expect to switch jobs or retire early.

Why the Real Cost Is Even Higher

Taxes and penalties are only part of the loss. When you default on a 401(k) loan:

You lose future growth on the money permanently removed from your retirement plan.

You can’t simply “rollover” the unpaid balance into an IRA—it’s treated as distributed cash.

In long-term projections, a $20,000 distribution today can mean over $60,000 less in retirement savings 20 years from now, assuming a 7% annual return.

Smart Ways to Borrow Without Derailing Your Retirement

If you’re considering a 401(k) loan, these steps can help minimize the risk:

Understand your plan’s terms. Confirm repayment rules, interest rates, and whether you can continue contributing while repaying the loan.

Have a backup plan. Keep cash reserves or other assets available in case you leave your job unexpectedly.

Avoid borrowing for depreciating expenses. Using retirement funds for short-term needs like vacations or vehicles can compound long-term losses.

Check your employment stability. If you expect to change jobs soon, it’s better to wait or use other financing options.

Compare alternatives. A home equity line of credit (HELOC) or personal loan may cost less in taxes and missed growth over time.

At Greenbush Financial Group, we often help clients run side-by-side projections showing the real long-term cost of borrowing from their 401(k) compared to other options. In most cases, the total impact of lost compounding far outweighs the short-term benefit of easy access to funds.

The Bottom Line

A 401(k) loan can make sense in limited cases, such as paying off high-interest debt or covering an emergency expense when other options are exhausted. But understanding the repayment rules—and the risk of job loss—is critical. One mistake, like leaving your employer before repaying the loan, can trigger thousands in taxes and permanently shrink your retirement balance.

Before taking out a loan, it’s worth modeling different scenarios with a financial planner to ensure your short-term decision doesn’t create a long-term setback.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: 401(k) Loan Rules and Risks

-

What’s the maximum I can borrow from my 401(k)?Generally, up to $50,000 or 50% of your vested balance, whichever is less.

-

How long do I have to repay a 401(k) loan?Most plans require repayment within five years, except when borrowing to purchase a primary residence.

-

What happens if I default on my loan?The unpaid balance is treated as a taxable distribution and may incur a 10% early withdrawal penalty if you’re under age 59½.

-

Can I roll my 401(k) loan into an IRA or new employer plan?No, loans cannot be rolled over. The balance must be repaid directly to avoid taxes.

-

Should I ever take a 401(k) loan?Only if the need is critical and you’re confident you’ll remain employed through the repayment period.

Is the Market About To Stage A Huge Rally?

The recent stock market pullback has been driven by rising oil prices, inflation concerns, and geopolitical tension involving Iran. As oil surged and uncertainty increased, markets reacted with increased volatility.

However, history shows that declines tied to geopolitical events are often temporary. This raises a key question for investors: is this a warning sign, or a setup for a potential market rally?

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

If the recent market volatility has made you uneasy, you’re not alone. Over the last few weeks, markets have reacted to rising oil prices, inflation concerns, and geopolitical tension in Iran. When volatility returns after a relatively calm period, it can feel like something is seriously wrong, but history tells us this is a normal part of investing, and specifically in this case, the market could be poised to rally in the coming weeks.

In this article, we’ll cover:

Forces at work in the market that have created the recent selloff

Whether the market may be near a bottom

What assets classes are performing well YTD in 2026

Charts to guide us as to where the market could go from here

What’s Causing the Market Sell-Off?

The recent market pullback hasn’t been caused by just one issue, but rather a combination of global events and economic pressures.

The biggest driver has been the conflict involving Iran, which has pushed oil prices significantly higher. At the start of the year, oil was around $57 per barrel, and as of March 23, 2026, oil has risen to roughly $90 per barrel. When oil prices rise that quickly:

The cost of transporting goods increases

The cost of producing goods increases

Inflation fears begin to rise

The Federal Reserve becomes less likely to cut interest rates

This is why markets have reacted negatively in the short term.

However, based on analyst expectations, there is a high probability that the Iran conflict will be resolved in the reasonably near future. If that happens, oil prices could fall, transportation costs could decline, and inflation fears could ease, which could put the Federal Reserve back on a path toward lowering interest rates.

And that combination has historically been very positive for markets.

It’s also important to remember that we’ve seen this movie before. Recent geopolitical events involving Greenland and Venezuela caused short-term market drops, but the markets recovered very quickly once those situations stabilized. Geopolitical events tend to create temporary volatility, not permanent declines.

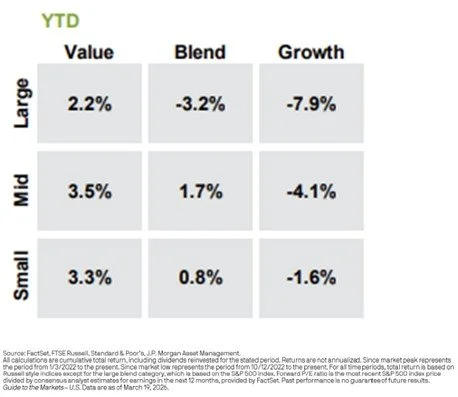

An Interesting Trend in 2026: Value vs. Growth

One of the most interesting trends this year has been the difference between large cap growth and large cap value.

As of last week:

Large cap growth is down about 7.9% year-to-date

Large cap value is up about 2.2% year-to-date

This shouldn’t be a huge surprise. Large cap value includes sectors like energy, which have performed very well due to rising oil prices. Meanwhile, many large cap growth and technology companies, including several of the “Magnificent Seven” stocks, have pulled back this year.

This is a great real-world reminder of why diversification matters.

When one part of the market struggles, another part of the market may be doing well. A properly diversified portfolio helps smooth out the ride when unexpected events occur.

Remember: Volatility Is Normal

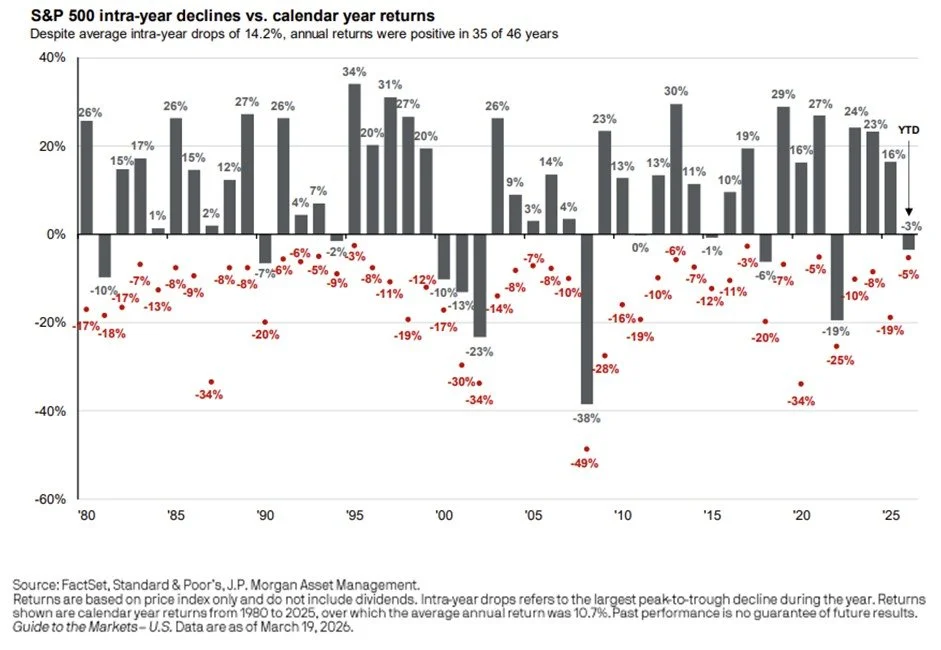

The chart below is a great reminder that selloffs and market volatility are normal even during good years for the stock market.

The chart shows two things going back to 1980:

The gray bars show the S&P 500 return for the full year

The red dots show the largest drop that occurred at some point during that year

For example:

In 2025, the market finished up 16%, but at one point during the year, it dropped by 19%

In 2024, the market finished up 23%, but had an 8% correction during the year

When you look at the last 45 years, a clear pattern emerges:

Most years the market finishes positive, but most years also have a signification correction at some point during the year.

This is the price of admission for investing. You don’t get the long-term returns of the market without experiencing volatility along the way.

Emotions and Panic Are the Enemy of Good Investment Decisions

The media and the markets will give investors something to worry about every single day.

Some of those concerns are legitimate. Many are not. The key is determining whether a current event represents a temporary disruption or a permanent change to the global economy.

Right now, the concern is Iran, oil prices, and inflation. A few months from now, it will likely be something else. That has always been the case, and it will continue to be the case.

One thing investors cannot forget is that we are currently in a massive wave of innovation and growth driven by artificial intelligence, automation, and robotics. These trends will likely have a much larger long-term impact on markets than most short-term geopolitical events.

This doesn’t mean markets won’t fall. They will.

It doesn’t mean volatility won’t happen. It will.

It doesn’t mean corrections won’t occur. They will.

But it does mean that panic-driven decisions are often the biggest mistake investors make.

Is the Market Close to the Bottom?

No one can consistently predict the exact bottom of a market correction. However, market declines driven by geopolitical events and oil shocks have historically recovered relatively quickly once the situation stabilizes. The Iran conflict is not likely be to any different.

If the Iran conflict cools down, and:

Oil prices fall

Transportation costs fall

Inflation fears ease

Then the current market pullback could reverse faster than many investors expect.

Market pullbacks often create opportunities that weren’t available when markets were at all-time highs just a few months ago.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.