4 Reasons Why You Would Not Delay Social Security Benefits to Age 70

The Social Security 50% spousal benefit allows married or divorced individuals to receive up to half of their spouse’s full retirement age benefit. This guide explains eligibility rules, timing strategies, and why delaying benefits may not always maximize household income. Learn how filing decisions affect both spouses and how to coordinate benefits for optimal retirement income. Understanding these rules is essential for building an efficient Social Security strategy.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Many people have heard that the optimal strategy is to delay Social Security benefits until age 70 so that you receive the maximum possible benefit. While that can be true in some situations, there are many scenarios where filing before age 70 may actually make more sense from a financial planning standpoint.

In this article, we’re going to walk through five reasons why you may not want to delay Social Security benefits to age 70, and why the decision should be based on your personal financial situation, health, and retirement goals.

1. Health Concerns and Life Expectancy

The decision to file early or delay Social Security is largely based on longevity. If there are health concerns or a shorter life expectancy, it may make more sense to file earlier rather than later.

While Social Security benefits increase over time, if you delay too long and pass away earlier than expected, you may never make up the years of missed payments.

Example

Let’s say someone is entitled to receive:

$3,000 per month at age 67

If they file at age 62, their benefit is reduced by about 30% to $2,100 per month

By filing at age 62 instead of 67, they would receive:

$2,100 × 12 = $25,200 per year

Over 5 years = $126,000 received before age 67

The question becomes: how long do you have to live for waiting to pay off?

The break-even point is typically somewhere between age 80 and 82.

If you live past 82, delaying often results in more lifetime income

If you pass away before 82, taking benefits earlier often results in more total dollars received

So when there are health concerns or reduced life expectancy, filing earlier can make financial sense.

2. The 50% Spousal Benefit

For married couples, the 50% spousal benefit can significantly impact when the higher-earning spouse should file.

Remember:

The lower-earning spouse can receive their own benefit or 50% of their spouse’s benefit, whichever is higher.

However, the lower-earning spouse cannot receive the spousal benefit until the higher-earning spouse files.

Example

Ken and Tracy:

Ken’s Full Retirement Age benefit: $3,000/month

Tracy’s FRA benefit: $1,000/month

Tracy’s 50% spousal benefit: $1,500/month

If Ken files at 67:

Ken receives $3,000

Tracy receives $1,500

Total household benefit = $4,500/month

If Ken delays until 70:

Tracy can only collect her own $1,000 until Ken files

She must wait 3 years before increasing to $1,500

The spousal benefit does not increase based on Ken waiting until 70

So when there is a large gap between the lower-earning spouse’s benefit and the spousal benefit, it can often make sense for the higher-earning spouse to file before age 70 to unlock the spousal benefit earlier.

3. You Need the Income to Retire

Sometimes the decision is simple: you need the income to retire.

Many individuals plan to retire at 62, 65, or 67, and Social Security is a key part of their retirement income plan along with pensions, investments, or other income sources.

If delaying Social Security to age 70 means:

You have to continue working longer than you want, or

You have to withdraw heavily from retirement accounts early,

Then filing earlier may be the better decision because it allows you to retire when you want while maintaining your lifestyle.

In other words, Social Security is not always about maximizing the monthly benefit — sometimes it’s about making retirement possible.

4. Delaying Withdrawals from Investment Accounts

Another reason someone may file earlier is to preserve their investment accounts.

Here’s the math:

Social Security increases about 6% per year before full retirement age

Social Security increases about 8% per year from full retirement age to age 70

If someone has investment accounts that are earning more than 6–8% per year, it may make sense to:

Turn on Social Security earlier

Use Social Security income

Allow investment accounts to continue growing

However, this is not a perfect apples-to-apples comparison because:

Social Security increases are guaranteed

Investment returns are not guaranteed and require market risk

But in strong market environments or for aggressive investors, this strategy can sometimes make sense.

Summary

While delaying Social Security until age 70 can increase your monthly benefit, it is not always the best financial decision. The right decision depends on:

Health and life expectancy

Spousal benefits

Retirement income needs

Investment returns

Estate planning goals

Social Security decisions should be made as part of a full retirement income plan, not in isolation.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions

-

Is age 70 always the best age to take Social Security?No. Age 70 provides the highest monthly benefit, but not always the highest lifetime benefit.

-

What is the Social Security break-even age?Typically between age 80 and 82.

-

When should I take Social Security if I have health issues?Filing earlier may make sense if life expectancy is shorter.

-

How does the spousal benefit affect when we should file?The higher-earning spouse filing earlier may allow the lower-earning spouse to collect a larger spousal benefit sooner.

-

Does Social Security increase every year I wait?Yes, roughly 6% per year before full retirement age and 8% per year after full retirement age until age 70.

-

Should I take Social Security early to preserve my investments?In some cases, yes - especially if your investments are growing faster than the Social Security increase.

-

What happens to my Social Security when I die?Your spouse may be eligible for a survivor benefit equal to your benefit.

-

Can I work and still collect Social Security?Yes, but if you collect before full retirement age, there may be an earnings limit.

-

Is Social Security taxable?Yes, depending on your total income, up to 85% of your Social Security may be taxable at the Federal level.

-

Should I talk to a financial advisor before filing for Social Security?Yes. The timing decision can impact hundreds of thousands of dollars over your lifetime.

Health Savings Account Distribution Tax and Penalty Rules

Health Savings Account (HSA) withdrawals have different tax and penalty rules depending on age and how funds are used. This guide explains the four distribution scenarios, tax treatment before and after age 65, and advanced strategies to maximize tax-free benefits. Learn how HSAs can serve as a powerful retirement healthcare tool and how to avoid common withdrawal mistakes. Ideal for pre-retirees planning tax-efficient income strategies.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available, but the tax treatment of distributions depends on how the money is used and the age of the account owner. There are essentially four different distribution scenarios that HSA owners can run into, and each scenario has different tax and penalty rules that are important to understand.

In this article, we’ll cover:

The four HSA distribution scenarios

Tax treatment before age 65

Tax treatment after age 65

Why HSAs are so valuable for retirement planning

Advanced HSA distribution strategies

Common HSA distribution mistakes to avoid

Frequently asked questions about HSA distributions

Why HSA Accounts Are So Valuable

Health Savings Accounts are unique because they offer a rare triple tax advantage:

Contributions are made pre-tax

The account grows tax-deferred

Distributions are tax-free if used for qualified medical expenses

Very few accounts receive this type of tax treatment. Traditional retirement accounts are tax-deferred, and Roth accounts are tax-free on the way out, but HSAs can be tax-free on both the contribution and distribution side when used correctly.

Because of this, many financial planners recommend not spending HSA funds during working years if possible, and instead allowing the account to grow and using it later in retirement when healthcare costs are typically much higher.

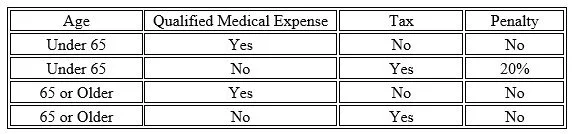

The Four HSA Distribution Scenarios

There are four main distribution scenarios that determine whether you owe taxes and/or penalties on HSA withdrawals:

Let’s walk through each scenario.

Distributions Prior to Age 65 (Qualified Medical Expenses)

If you take a distribution from an HSA before age 65 and use the money for a qualified medical expense, the distribution is:

Tax-free

Penalty-free

This is the ideal use of an HSA. Qualified expenses can include:

Doctor visits

Deductibles and coinsurance

Dental and vision care

Hearing aids

Prescription medications

Medicare premiums (after age 65)

Medical equipment

In these cases, the HSA functions exactly as intended — a tax-free healthcare account.

Distributions Prior to Age 65 (Non-Qualified Expenses)

If you take a distribution before age 65 and the expense is not qualified, the distribution is:

Subject to ordinary income tax

Subject to a 20% penalty

For example, if someone is in a 30% tax bracket and takes a non-qualified distribution:

30% tax

20% penalty

Total loss = 50% of the distribution

This is why it is usually recommended to preserve HSA funds for medical expenses whenever possible.

Distributions Age 65 or Older (Qualified Medical Expenses)

This scenario works the same as before age 65.

If the distribution is used for qualified medical expenses, the withdrawal is:

Tax-free

Penalty-free

This is why HSAs are often used as a retirement healthcare fund.

Common qualified expenses in retirement include:

Medicare Part B premiums

Medicare Part D premiums

Medicare Advantage premiums

Out-of-pocket medical expenses

Deductibles and coinsurance

Dental and vision care

Hearing aids

Medical equipment

Distributions Age 65 or Older (Non-Qualified Expenses)

This is where the rules change.

After age 65, if you take money from an HSA for non-qualified expenses:

You pay ordinary income tax

No 20% penalty

At this point, the HSA starts to function similarly to a Traditional IRA. The money can be used for anything, but it becomes taxable income if not used for medical expenses.

This provides flexibility in retirement in case the funds are needed for non-medical expenses.

Important Rule: Reimbursed Expenses Do NOT Qualify

One important rule that retirees need to be aware of:

If a medical expense is reimbursed by insurance or a former employer, you cannot also take a tax-free HSA distribution for that same expense.

For example:

Some retirees have employer retiree health plans that reimburse Medicare premiums.

If the retiree is reimbursed for Medicare Part B or Part D, those expenses cannot also be reimbursed from the HSA tax-free.

This would be considered a non-qualified distribution, and taxes would apply.

Advanced HSA Distribution Strategies

There are several advanced strategies that can make HSAs even more powerful:

1. Save Receipts and Reimburse Yourself Later

There is no time limit on when you reimburse yourself from an HSA for a qualified expense, as long as:

The expense occurred after the HSA was established

You kept the receipt

This means someone could:

Pay medical expenses out-of-pocket during working years

Allow the HSA to grow

Reimburse themselves years later tax-free

This effectively turns the HSA into a tax-free retirement account.

2. Use HSA for Medicare Premiums

HSA funds can be used tax-free for:

Medicare Part B

Medicare Part D

Medicare Advantage

(This becomes a built-in retirement healthcare fund.)

3. Treat HSA Like a Backup Traditional IRA

After age 65, if needed, HSA funds can be withdrawn for non-medical expenses and simply taxed as income, with no penalty.

Common HSA Distribution Mistakes

Some of the most common mistakes include:

Using HSA funds for non-qualified expenses before 65

Losing receipts for reimbursement

Using HSA funds for reimbursed expenses

Spending HSA funds during working years instead of investing them

Not investing HSA funds for long-term growth

Forgetting that non-qualified withdrawals before 65 have a 20% penalty

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Do I pay taxes on HSA distributions?Only if the distribution is used for a non-qualified expense.

-

What is the penalty for non-qualified HSA withdrawals before age 65?A 20% penalty plus ordinary income tax.

-

What happens to the penalty after age 65?The 20% penalty goes away, but distributions are still taxable if not used for medical expenses.

-

Can I use my HSA for Medicare premiums?Yes, for Medicare Part B, Part D, and Medicare Advantage.

-

Can I reimburse myself years later from my HSA?Yes, as long as the expense occurred after the HSA was established and you kept the receipt.

-

Are HSA distributions reported on a tax return?Yes, distributions are reported on IRS Form 8889.

-

Can I use my HSA for my spouse's medical expenses?Yes, even if your spouse is not on your health insurance plan.

-

What happens to my HSA when I turn 65?You can still use it tax-free for medical expenses, and penalty-free for non-medical expenses (taxable).

-

Can I use my HSA for dental and vision expenses?Yes, most dental and vision expenses qualify.

-

Is an HSA better than a 401(k)?For medical expenses, an HSA can be more tax-efficient because it is tax-free on both contributions and qualified distributions.

Should You Spend or Save Your HSA Account?

Health Savings Accounts offer a unique triple tax advantage, making them one of the most powerful retirement planning tools available. This article explains when to spend versus save your HSA, how to invest it for long-term growth, and how it can be used for healthcare costs in retirement. You’ll also learn the 2026 HSA contribution limits and strategies to maximize your account’s value. Understanding how to use your HSA properly can significantly improve retirement income planning and reduce future medical expenses.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available, yet many people still wonder whether they should use the HSA now for medical expenses or save it for retirement. The answer depends on your financial situation, but in many cases, saving your HSA for the future can provide significant long-term benefits.

In this article, you’ll learn:

How HSAs receive triple tax advantages

When it makes sense to spend vs. save your HSA

How HSAs can be used for healthcare expenses in retirement

Why investing your HSA can dramatically increase its value

2026 HSA contribution limits

A real-life example showing long-term HSA growth

A hybrid strategy that works for many households

Understanding the Triple Tax Advantage of an HSA

HSAs are unique because they offer what is often called a triple tax benefit:

Contributions are made pre-tax

The money grows tax-deferred

Withdrawals are tax-free if used for qualified medical expenses

Very few accounts offer this type of tax treatment. Traditional retirement accounts are tax-deferred, Roth accounts are tax-free on withdrawal, but HSAs offer both benefits — which is why many financial planners consider HSAs one of the most powerful long-term savings tools available.

Should You Spend or Save Your HSA?

The original purpose of an HSA was to pay for current medical expenses with pre-tax dollars. However, a larger planning opportunity exists:

If you can afford to pay medical expenses out-of-pocket today, it may make sense to leave your HSA invested and growing for retirement.

Why? Because healthcare costs tend to increase significantly as we age, especially in retirement. Having a dedicated account for healthcare expenses reduces the risk that large medical costs will disrupt your retirement income plan.

What Can HSAs Be Used for in Retirement?

Many people don’t realize how many retirement healthcare expenses can be paid from an HSA, including:

Medicare Part B premiums

Medicare Part D premiums

Medicare Advantage premiums

Dental expenses

Vision expenses

Hearing aids

Long-term care insurance premiums (within limits)

Medical equipment (wheelchairs, walkers, etc.)

Deductibles and copays

Prescription medications

Because these expenses can be paid tax-free from an HSA, it effectively makes those healthcare costs tax deductible in retirement.

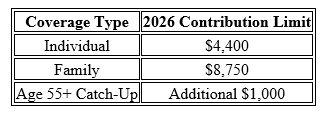

2026 HSA Contribution Limits

For 2026, the IRS increased HSA contribution limits:

These limits include both employee and employer contributions combined.

The Power of Investing Your HSA

If you plan to use your HSA more than 5 years in the future, it often makes sense to invest the HSA rather than leaving it in cash or a money market account. The reason is simple: compound interest.

Example:

If you are age 40, contribute $4,000 per year, and earn 8% annually, by age 62 your HSA could grow to approximately:

Total account value: $243,000

Total contributions: $92,000

Investment growth: $151,000

In this example, most of the account value came from investment growth, not contributions. That is the real power of using an HSA as a long-term healthcare investment account.

Not All HSA Providers Allow Investing

Some HSAs only allow cash savings, while others allow full investment access similar to a retirement account. Some popular HSA providers that offer investment options include:

Fidelity Investments

Charles Schwab

HealthEquity

If your HSA is through your employer, it often makes sense to:

Contribute through payroll to capture tax benefits

Then periodically transfer funds to an HSA provider with investment options

This strategy allows you to get the best of both worlds — tax savings and investment growth.

A Hybrid Strategy May Work Best

Not everyone can afford to pay medical expenses out-of-pocket. That’s where a hybrid strategy can work well:

Use your HSA for large medical expenses

Pay smaller expenses out-of-pocket when possible

Try to preserve and invest as much of the HSA as possible for retirement

This approach balances current needs with long-term planning.

Final Thoughts

Healthcare is one of the largest expenses in retirement. Having a dedicated, tax-free account to pay for those costs can significantly improve retirement security. For many individuals, the HSA becomes less of a short-term spending account and more of a long-term healthcare retirement account.

If used strategically, an HSA can become a healthcare safety net, helping reduce the financial risk of rising medical costs later in life.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Should I max out my HSA every year?If you can afford to, many financial planners recommend maxing out your HSA due to the triple tax advantage.

-

Is an HSA better than a 401(k)?They serve different purposes, but an HSA often has better tax treatment if used for medical expenses.

-

Can I use my HSA for Medicare premiums?Yes, you can use HSA funds for Medicare Part B, Part D, and Medicare Advantage premiums.

-

Can I invest my HSA?Yes, but only if your HSA provider allows investment options.

-

What happens if I use HSA money for non-medical expenses?Before age 65, you pay income tax plus a 20% penalty. After age 65, you only pay income tax.

-

Do HSA funds expire?No. HSA funds roll over every year and stay with you for life.

-

Can I reimburse myself later for medical expenses?Yes. As long as you kept the receipt, you can reimburse yourself years later.

-

Should I invest my HSA or keep it in cash?If the money won't be used for several years, investing often makes sense due to compound growth.

-

Can I have more than one HSA account?Yes. You can contribute to one and transfer to another.

-

What is the biggest benefit of an HSA?The triple tax advantage: pre-tax contributions, tax-deferred growth, and tax-free withdrawals for medical expenses.

College Savings or Retirement First? How to Decide in 2026

Should you save for your child’s college or your own retirement first? It’s one of the most common questions we hear from families trying to balance competing financial goals. Our analysis at Greenbush Financial Group shows that in most cases, prioritizing retirement creates greater long-term security—while still leaving room to build meaningful college savings over time. This guide explains why the order matters, how 529 plans fit in, and how to create a balanced strategy that protects both your future and your child’s opportunities.

One of the most common financial planning questions we hear at Greenbush Financial Group is whether to prioritize saving for your children’s college or for your own retirement. Both goals are important—but when resources are limited, the right order can make a major difference in your long-term security. In most cases, it makes sense to secure your retirement first, then allocate additional savings toward education goals. Here’s why that order matters and how to balance both effectively.

Why Retirement Comes First

Retirement should almost always take priority for one simple reason: there are no loans for retirement. Your future financial independence depends on your ability to replace your income when you stop working—and that window to save is limited.

Key Reasons to Prioritize Retirement

You can’t borrow for it. Your children can access student loans, grants, or scholarships; you cannot do the same for retirement income.

Compounding works best early. The earlier you contribute to retirement accounts like a 401(k) or IRA, the more time your investments have to grow tax-deferred or tax-free.

Employer matches add free money. If you skip retirement contributions to fund college, you may also miss out on employer matching contributions that could increase your savings rate.

Tax advantages are stronger. Retirement accounts typically offer better tax deferral and protection benefits than education accounts.

The Case for Funding College Early

While retirement usually takes priority, it’s also important to plan for education costs strategically. A balanced approach can help you avoid high student loan debt while still protecting your own future.

Benefits of Starting College Savings Early

Tax-free growth. 529 plans grow tax-free and withdrawals are tax-exempt when used for qualified education expenses.

High contribution limits. You can contribute up to $19,000 per year per parent ($38,000 for married couples) in 2026 without triggering the gift tax, and you can front-load five years’ worth at once.

State tax benefits. Many states offer income tax deductions or credits for 529 plan contributions.

Investment flexibility. Funds can be used for tuition, room and board, and even graduate school.

For families with younger children, consistent 529 contributions—even modest ones—can grow meaningfully over 15–18 years while you continue building your retirement savings.

Balancing Both Goals

It doesn’t have to be all-or-nothing. You can take a blended approach:

Maximize employer match in your 401(k) or SIMPLE IRA first.

Open a 529 plan and set up automatic contributions (even $100 per month makes a difference).

Reevaluate each year—as income rises, you can shift additional funds toward college savings.

Use windfalls wisely. Bonuses, tax refunds, or side-income can go toward education savings without disrupting retirement.

Encourage student participation. Teen jobs, scholarships, or community college for core credits can reduce overall cost.

At Greenbush Financial Group, we often model side-by-side scenarios showing how redirecting amounts from retirement to college savings can alter your future income security.

How Retirement Savings Can Help with College

One overlooked advantage: saving for retirement can indirectly help with college funding.

Lower FAFSA impact: Retirement assets aren’t counted toward federal financial aid formulas, while 529 balances are.

Penalty-free withdrawals: The IRS allows penalty-free (but taxable) withdrawals from IRAs for qualified education expenses if needed later.

Future flexibility: A strong retirement foundation may let parents help pay off loans later without jeopardizing their future.

Action Steps to Get Started

Review your retirement contribution rate and increase it until you reach your employer’s match or target savings goal.

Set up a 529 plan for each child, even if contributions start small.

Reassess annually as college costs and retirement targets evolve.

Meet with a financial planner to model the long-term trade-offs of different savings rates.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: College Savings vs. Retirement

-

Should I ever prioritize college savings over retirement?Only if your retirement plan is fully funded or you’re on track with a strong pension. Otherwise, we believe that your future security should come first.

-

Can I use my IRA for college expenses?Yes, you can withdraw IRA funds penalty-free (though taxable) for qualified higher education costs, but this should often be a last resort.

-

How much should I contribute to a 529 plan?Many families aim for about one-third of projected costs; the rest can come from cash flow, aid, or loans. Even small, consistent contributions grow substantially over time.

-

What if I can’t afford both?Focus on retirement first. You could potentially help your child repay loans later, but you can’t finance your own retirement.

-

Are there other college savings options besides 529s?Yes—Coverdell ESAs and custodial UGMA/UTMA accounts can also be used, though they have different tax and financial aid impacts.

2026 Mandatory Roth Catch-Up Contributions for Higher Earners: What the New Rules Mean for Retirement Savers

Starting in 2026, higher-income workers age 50 and older will be required to make retirement plan catch-up contributions on a Roth (after-tax) basis under SECURE Act 2.0. This change impacts 401(k), 403(b), and governmental 457(b) plans and could increase current taxable income for many pre-retirees. Our analysis at Greenbush Financial Group explains who is affected, how the rule works, and the planning strategies that can help turn this tax shift into a long-term advantage.

Beginning in 2026, higher-earning workers will be required to make all retirement plan catch-up contributions on a Roth (after-tax) basis. This rule, created under SECURE Act 2.0, applies to individuals earning above a specific wage threshold and affects 401(k), 403(b), and governmental 457(b) plans. Our analysis at Greenbush Financial Group shows that while the change increases current taxable income, it can also create meaningful long-term tax benefits if planned correctly. This article explains who is impacted, how the rule works, and what planning steps to consider before 2026.

What Is the Mandatory Roth Catch-Up Rule in 2026?

The mandatory Roth catch-up rule requires certain high earners to make all catch-up contributions as Roth contributions, rather than pre-tax.

Under prior rules, employees age 50 and older could choose whether catch-up contributions were pre-tax or Roth. Starting in 2026, that choice is removed for higher earners.

At Greenbush Financial Group, this is one of the most common sources of confusion we see among pre-retirees who are aggressively saving in the final working years.

Who Is Subject to Mandatory Roth Catch-Up Contributions?

The rule applies if both of the following are true:

You are age 50 or older

Your prior-year wages exceed $150,000, indexed for inflation

Wages are based on W-2 compensation

Income from self-employment or investments does not count toward this threshold

If your wages are at or below the threshold, you may still choose between pre-tax or Roth catch-up contributions.

Which Retirement Plans Are Affected by the Rule?

Mandatory Roth treatment applies to catch-up contributions made to:

401(k) plans

403(b) plans

Governmental 457(b) plans

It does not apply to:

IRAs (Traditional or Roth)

SEP IRAs

SIMPLE IRAs (which follow separate contribution rules)

Catch-Up Contribution Limits for 2026

While final IRS-indexed numbers will be confirmed closer to 2026, current rules provide context for how the change applies.

General framework:

Standard elective deferral limit (under age 50): indexed annually

Catch-up contributions (age 50+): additional amount above the standard limit

Ages 60–63: enhanced catch-up limits under SECURE Act 2.0, also subject to Roth-only treatment for higher earners

Our analysis at Greenbush Financial Group suggests that many high earners will still benefit from maximizing these Roth catch-up dollars despite losing the immediate tax deduction.

Why Congress Implemented the Mandatory Roth Requirement

The shift to Roth catch-up contributions serves two primary purposes:

Increases near-term tax revenue for the federal government

Expands long-term tax-free retirement savings for participants

Because Roth contributions are taxed upfront, the rule accelerates tax collection while potentially reducing future required minimum distributions.

Tax Impact: Higher Income Today, Lower Taxes Later

Mandatory Roth catch-ups create a trade-off.

Short-term impact:

Higher taxable income

Reduced ability to lower current-year tax bills

Long-term benefits:

Tax-free growth

Tax-free withdrawals in retirement

Reduced exposure to future tax rate increases

Potentially lower Medicare IRMAA and Social Security taxation later in life

At Greenbush Financial Group, we often see this rule align well with broader Roth conversion strategies already being implemented for higher-income households.

Employer and Plan Administration Considerations

Employers must ensure their retirement plans are properly updated to allow Roth catch-up contributions.

Key considerations:

Plans that do not allow Roth contributions may need amendments

Failure to comply could eliminate the ability to make catch-up contributions entirely

Payroll and recordkeeping systems must track Roth-only catch-ups correctly

This is an important operational issue for both employers and employees to confirm well before 2026.

Planning Strategies Before 2026

There is still time to plan proactively.

Strategies to consider:

Evaluating partial Roth conversions during lower-income years

Coordinating catch-up contributions with overall tax bracket management

Reviewing whether employer plans are Roth-enabled

According to guidance from the Internal Revenue Service, compliance will be strictly tied to wage reporting, making advance planning essential.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions About Mandatory Roth Catch-Up Contributions

-

What is the mandatory Roth catch-up rule starting in 2026?It requires higher-earning employees age 50+ to make all retirement plan catch-up contributions on a Roth (after-tax) basis.

-

What income level triggers mandatory Roth catch-ups?The rule applies to individuals with prior-year W-2 wages above $150,000 (2025 amount), indexed for inflation.

-

Does this rule apply to IRAs?No. The mandatory Roth catch-up requirement only applies to employer retirement plans, not IRAs.

-

Can I still make pre-tax contributions if I’m a high earner?Yes. The rule only affects catch-up contributions; standard employee deferrals may still be pre-tax.

-

What happens if my employer’s plan doesn’t offer Roth contributions?If Roth contributions are not available, catch-up contributions may not be permitted until the plan is amended.

-

Is mandatory Roth catch-up a bad thing for retirees?Not necessarily. While taxes may increase today, Roth catch-ups can significantly reduce taxes in retirement if used strategically.

2026 New York State Mandatory IRA Rules: What Employers Must Do to Stay Compliant

New York State’s Secure Choice IRA program is creating new compliance requirements for many employers beginning in 2026. Businesses with 10 or more employees that do not already offer a qualified retirement plan may be required to enroll workers in this state-facilitated Roth IRA program. Our analysis at Greenbush Financial Group explains who must comply, employer responsibilities, potential penalties, and why alternative retirement plans like SIMPLE IRAs or 401(k)s may offer greater long-term value.

New York State now requires many employers to offer a retirement savings option through the state-mandated Secure Choice IRA program. If your business has at least 10 employees and does not already offer a qualified retirement plan, participation is mandatory. Our analysis at Greenbush Financial Group shows that understanding who must comply, how the program works, and what alternatives exist can help business owners avoid penalties while improving employee retention. This article explains New York’s mandatory IRA rules and outlines smarter planning options for employers.

What Is the New York State Mandatory IRA Program?

The New York State mandatory IRA requirement applies through the New York State Secure Choice Savings Program, a state-facilitated retirement savings option for private-sector employees.

Secure Choice is designed for workers who do not have access to an employer-sponsored retirement plan. Employers act as facilitators, while the state oversees the program’s administration.

Key characteristics:

Roth IRA structure for employees

Automatic payroll deductions

No employer contributions required

State-administered investment options

Which New York Employers Are Required to Offer a Mandatory IRA?

Under New York law, participation is mandatory if all of the following apply:

You have 10 or more employees

You have been in business for at least two years

You do not currently offer a qualified retirement plan such as a 401(k), SIMPLE IRA, or SEP IRA

At Greenbush Financial Group, we commonly see confusion around part-time and seasonal employees. For Secure Choice purposes, employees are generally counted if they are on payroll, regardless of hours worked.

Which Businesses Are Exempt From the Requirement?

You are exempt from the New York mandatory IRA requirement if your business already offers:

A 401(k) or Safe Harbor 401(k)

A SIMPLE IRA

A SEP IRA

A defined benefit or cash balance pension plan

Offering any qualified retirement plan removes the obligation to participate in Secure Choice. This exemption often creates an opportunity for employers to choose a more flexible and customizable plan instead.

How the Secure Choice IRA Works for Employees

Eligible employees are automatically enrolled unless they opt out.

Default program features include:

Automatic enrollment at a preset contribution rate

Contributions made on a Roth (after-tax) basis

Employee-owned accounts that move with them if they change jobs

Limited investment menu selected by the state

Employees can:

Change contribution amounts

Opt out at any time

Withdraw funds subject to Roth IRA rules and penalties

Employer Responsibilities Under the Mandatory IRA Law

Although employers do not contribute financially, they still carry administrative responsibilities.

Employer duties include:

Registering with the Secure Choice program

Providing employee information

Processing payroll deductions

Submitting contributions on schedule

Distributing required employee notices

Failure to comply may result in state enforcement actions once deadlines are fully phased in.

Deadlines and Penalties for Non-Compliance

New York’s rollout is being phased in by employer size, with enforcement expected to increase through 2026.

Potential consequences of non-compliance include:

Monetary penalties

State enforcement notices

Increased scrutiny for repeat violations

Our analysis at Greenbush Financial Group suggests that many business owners delay action simply because they are unaware the rule applies to them.

Is Secure Choice the Best Option for Employers?

For some businesses, Secure Choice meets the minimum requirement. However, it may not be the best long-term solution.

Limitations of the mandatory IRA include:

No employer contribution flexibility

Roth-only structure

Limited investment choices

Reduced perceived benefit compared to a 401(k)

In contrast, alternatives such as SIMPLE IRAs or 401(k) plans can:

Increase tax deductions for employers

Improve employee recruitment and retention

Offer higher contribution limits

Allow customized plan design

At Greenbush Financial Group, we often help employers compare Secure Choice with private retirement plans to determine the most cost-effective and strategic solution.

Planning Considerations for Business Owners

When deciding how to comply, consider:

Your employee demographics and turnover

Tax deductions available to the business

Administrative complexity

Long-term growth and scalability

Choosing the right retirement plan is not just about compliance; it is a strategic business decision.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions About New York State Mandatory IRAs

-

Is the New York State Secure Choice IRA mandatory for all businesses?No. It is only mandatory for businesses with 10 or more employees that do not already offer a qualified retirement plan.

-

Do employers have to contribute to the Secure Choice IRA?No. Employers are not allowed or required to make contributions; only employee payroll deductions are permitted.

-

What happens if my business ignores the mandatory IRA requirement?Non-compliance may result in penalties and enforcement actions as the state increases oversight.

-

Can employees opt out of the New York mandatory IRA?Yes. Employees are automatically enrolled but may opt out or change contributions at any time.

-

Does offering a SIMPLE IRA exempt my business from Secure Choice?Yes. Offering a SIMPLE IRA, 401(k), or SEP IRA fully satisfies the requirement.

-

Is Secure Choice better than a 401(k) for small businesses?Not always. While Secure Choice is simple, many businesses benefit more from private plans with higher limits and tax advantages.

How Rich Retirees Use Debt to Save on Taxes and Protect Their Investments

Borrowing in retirement might seem surprising, but for high-net-worth retirees, strategic debt can be a powerful financial planning tool. Instead of triggering large capital gains taxes by selling investments, many wealthy retirees use low-cost borrowing to access liquidity while keeping their portfolios fully invested. In this article, Greenbush Financial Group explains how securities-backed lines of credit, HELOCs, margin loans, and other strategies can help retirees manage taxes, preserve growth, and maintain financial flexibility.

It might sound counterintuitive: if you’ve saved millions for retirement, why borrow money at all? Yet many wealthy retirees intentionally use debt as a financial planning tool. Strategic borrowing can help preserve portfolio value, manage taxes, and access liquidity without triggering large capital gains.

The key isn’t whether you borrow—but how and when. Here’s why financially independent retirees still use leverage, and how they do it at the lowest possible cost.

The Strategy Behind Borrowing in Retirement

For many retirees, the instinct is to pay off all debt before leaving the workforce. That’s smart for high-interest loans or unstable budgets—but not always for those with significant assets. Wealthy retirees often continue borrowing because it offers flexibility that selling investments does not.

The main reasons include:

Avoiding large taxable sales in brokerage or trust accounts

Keeping investments fully invested during market growth

Accessing liquidity for real estate, business, or family needs

Taking advantage of low interest rates or deductible borrowing options

At Greenbush Financial Group, we see this most often with clients who have appreciated portfolios or taxable trusts—they’d rather borrow temporarily than realize large capital gains and lose compounding potential.

Why Borrowing Can Be Cheaper Than Selling

Borrowing money doesn’t trigger taxes; selling investments does. If you sell appreciated assets to raise cash, you could owe capital gains tax of up to 23.8% federally (20% long-term plus 3.8% Net Investment Income Tax), plus potential state taxes.

Example:

A retiree with $1 million in long-term appreciated stock may owe over $200,000 in taxes if sold outright. Borrowing $250,000 against a portfolio or property can access cash immediately—often at interest rates of 5–6%—while deferring or avoiding that tax bill entirely.

For many, the after-tax cost of borrowing is lower than the effective tax cost of liquidation.

Common Low-Cost Borrowing Strategies for Retirees

There are several ways high-net-worth retirees access cash without disrupting their investment or tax strategy.

1. Securities-Backed Lines of Credit (SBLOCs)

An SBLOC allows you to borrow against your taxable investment portfolio, typically up to 50–70% of its value.

Rates often range between 5–7%, depending on the lender.

Interest-only payments are common, offering flexibility.

No credit check or underwriting is required beyond the assets themselves.

Caution: if markets decline sharply, the lender can require additional collateral or partial repayment.

2. Home Equity Lines of Credit (HELOCs)

Even wealthy retirees may use HELOCs to fund large expenses such as renovations, second homes, or bridge financing.

Interest may be deductible if used for home improvements.

Flexible draw periods make it easy to access only what you need.

Current rates vary, but fixed options can provide predictability.

3. Margin Loans for Portfolio Liquidity

Margin loans through brokerage accounts allow investors to borrow directly against securities.

Typically used for short-term needs or opportunistic purchases.

Rates depend on account size—often lower for high-net-worth clients.

Requires careful monitoring to avoid margin calls during volatility.

4. Cash Value Life Insurance Loans

Retirees with permanent life insurance policies can borrow against accumulated cash value tax-free.

No credit check or repayment schedule.

Interest accrues against the policy, not external debt.

Works best when used sparingly and managed over decades.

5. Family or Trust Lending

Some retirees lend to children or family trusts using IRS-approved Applicable Federal Rates (AFRs)—currently well below most commercial lending rates.

Can serve estate-planning goals while keeping assets in the family.

Requires formal loan documents and consistent payment terms.

When Borrowing Makes Sense (and When It Doesn’t)

Borrowing in retirement can be powerful, but it’s not for everyone.

It can make sense if:

You have a large taxable portfolio or illiquid real estate holdings

You expect long-term investment growth exceeding borrowing costs

You’re managing capital gains, Roth conversions, or Medicare thresholds

It’s risky if:

You need stable monthly cash flow

Your investments are volatile or highly concentrated

You’re carrying multiple types of debt already

Borrowing should support—not replace—a comprehensive income plan.

How Rich Retirees Keep Borrowing Costs Low

Wealthy retirees often have access to rates below what most consumers see because they borrow against assets, not income. Lenders view a $3 million portfolio differently than a paycheck.

Ways they minimize cost include:

Negotiating private banking relationships for rate discounts

Keeping large asset balances at lending institutions

Using securities-based lines instead of personal loans

Deducting certain interest payments when eligible under IRS rules

At Greenbush Financial Group, we often coordinate between a client’s lender, tax preparer, and investment advisor to ensure each borrowing decision fits their larger tax and income strategy.

The Bottom Line

Even for retirees who are financially independent, liquidity and tax management matter. Borrowing can be a smart, temporary tool to access cash without dismantling a well-built portfolio. When used strategically, the right type of low-cost loan can help preserve wealth, reduce taxes, and maintain flexibility.

The key is to treat debt as part of a coordinated plan, not a shortcut. A thoughtful lending strategy can make your money work harder—even when you no longer need a paycheck.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQs: Borrowing in Retirement

-

Why would a wealthy retiree take on debt?To access liquidity without selling investments and triggering capital gains taxes.

-

What’s the difference between an SBLOC and a margin loan?Both use investments as collateral, but SBLOCs are separate from trading accounts and often carry more flexible terms.

-

Can retirees deduct interest on borrowed funds?In some cases, yes—if the loan proceeds are used for investment or home improvement purposes.

-

Is borrowing against investments risky?It can be if markets decline and collateral values drop, so monitoring and limits are essential.

-

What’s the cheapest way for retirees to borrow?Securities-backed credit lines and family lending arrangements typically offer the lowest rates for high-net-worth households.

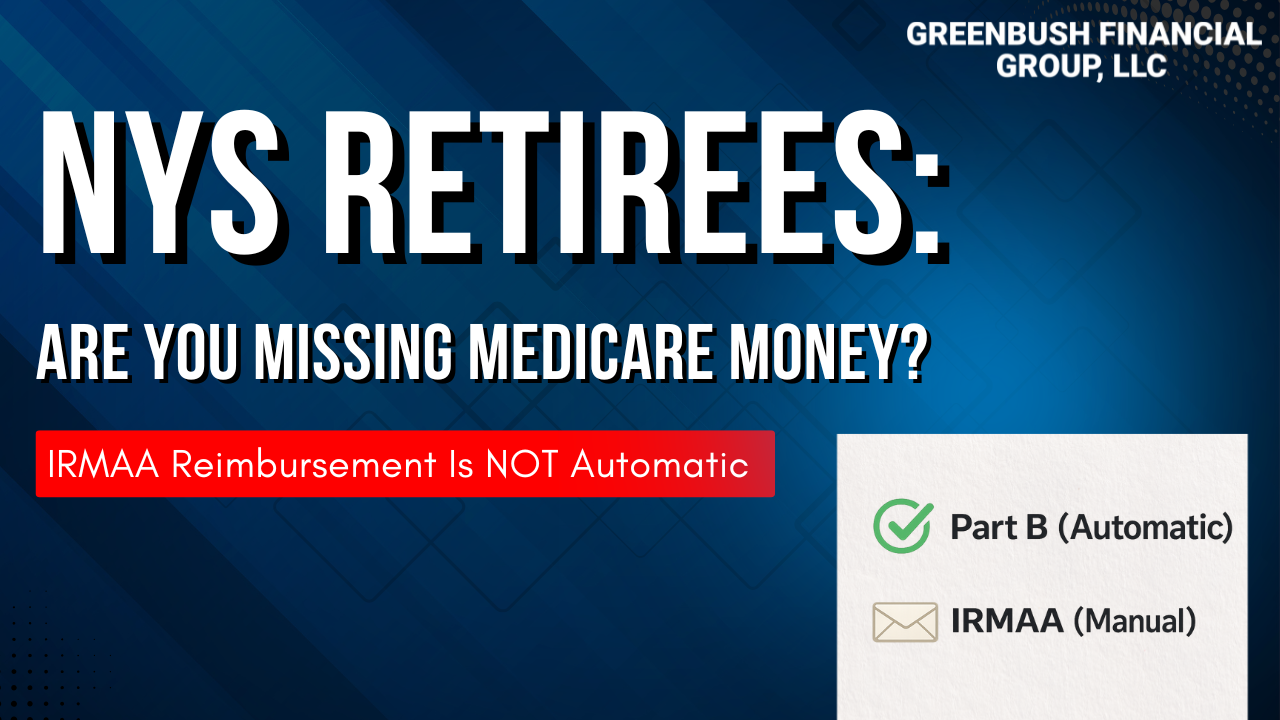

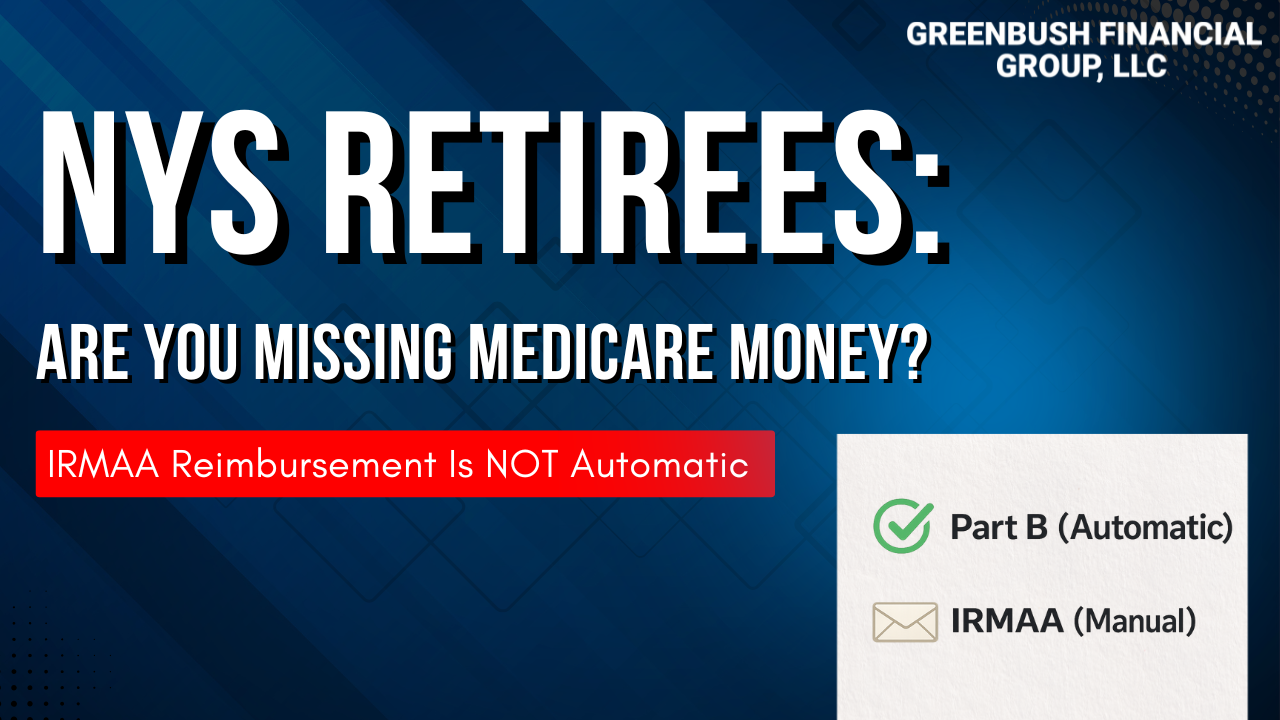

NYS Retiree Medicare Part B and IRMAA Reimbursement Process Explained

New York State retiree health benefits include a powerful perk: reimbursement for Medicare Part B premiums after age 65. But many retirees don’t realize that IRMAA surcharges can also be reimbursed — and that process is manual. This guide explains how NYS Part B reimbursement works automatically through pension increases, how IRMAA (Income-Related Monthly Adjustment Amount) raises Medicare premiums for higher earners, what form you must file to get IRMAA money back, and how to claim up to four years of missed reimbursements.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

For individuals who retire from New York State service, the retiree health benefits are among the most generous in the country. One of the most valuable — and often misunderstood — features is how Medicare Part B premiums and IRMAA surcharges are reimbursed after age 65.

This article explains, in plain language:

How New York State automatically reimburses retirees for Medicare Part B premiums

How IRMAA (Income-Related Monthly Adjustment Amount) works and why higher earners pay more

The manual process required to get reimbursed for IRMAA

How far back you can go to reclaim missed IRMAA reimbursements

What retirees (and spouses) need to do each year to stay reimbursed

How Does New York State Reimburse Retirees for Medicare Part B Premiums?

Once a New York State retiree reaches age 65 and enrolls in Medicare, the Medicare Part B premium reimbursement is automatic.

There is no form to file and no annual application required for the base Medicare Part B premium.

Here’s how it works:

When you turn 65 and enroll in Medicare Part B during your open enrollment window

New York State automatically increases your monthly pension by the amount of the standard Medicare Part B premium

This applies to:

The retiree

A spouse who is covered under the New York State retiree health plan

That automatic pension increase is why New York State retiree health benefits are considered so lucrative — the reimbursement applies to both the retiree and their spouse, which can amount to thousands of dollars per year.

2026 Medicare Part B Example

In 2026, the base Medicare Part B premium is $202.90 per month.

Example:

A New York State retiree is receiving a pension of $2,000 per month

Upon turning 65 and enrolling in Medicare Part B

Their pension automatically increases to $2,202.90 per month

That increase directly offsets the Medicare Part B premium that is being deducted from their Social Security check.

If you are only paying the standard Medicare Part B premium, no action is required beyond enrolling in Medicare on time.

Understanding IRMAA: Why Higher-Income Retirees Pay More for Medicare

Medicare premiums are income-based. As income rises, so does the Medicare Part B premium — this additional charge is known as IRMAA (Income-Related Monthly Adjustment Amount).

2026 IRMAA Income Thresholds

For 2026, IRMAA begins when income exceeds:

Single filers: $109,000

Married filing jointly: $218,000

Above those levels, Medicare Part B premiums increase in steps as income rises.

IRMAA Example for a NYS Retiree

Let’s say:

A single New York State retiree

With retiree health benefits

Earns $200,000 in 2026

Instead of paying the base $202.90 per month, their Medicare Part B premium increases to $527.50 per month due to IRMAA.

That’s an additional $324.60 per month, or nearly $3,900 per year, in extra Medicare costs.

How IRMAA Reimbursements Work for New York State Retirees

New York retirees are often pleasantly surprised to find out that the retiree health plan not only reimbursement them for the standard Medicare premium but also the IRMAA amount but the IRMAA reimbursement process is not automatic.

What Happens Automatically vs. Manually

✅ Base Medicare Part B premium

Reimbursed automatically through an increased pension payment

❌ IRMAA surcharge

Requires a physical application each year

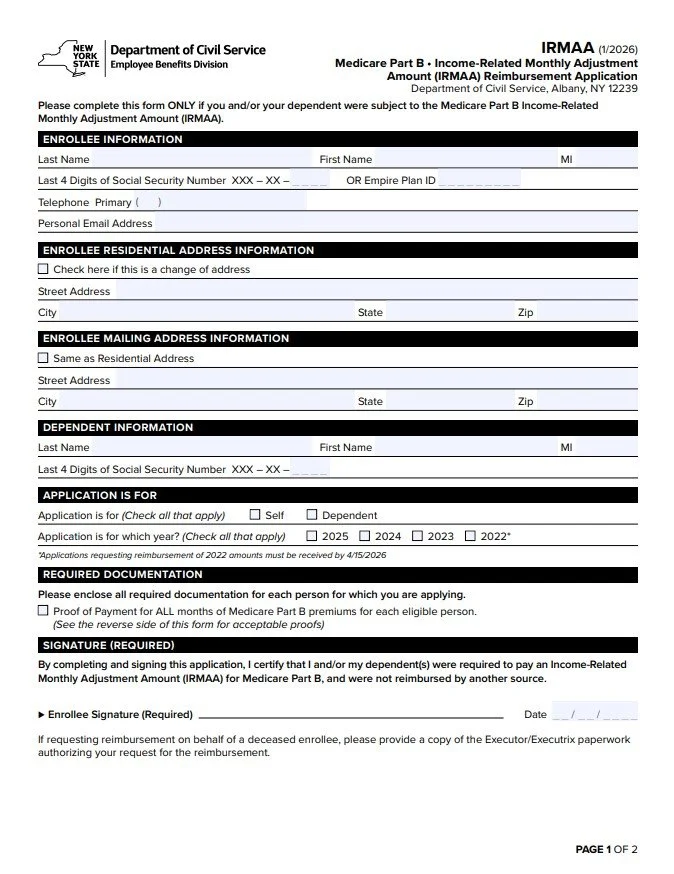

To receive reimbursement for IRMAA, the retiree must:

Complete the IRMAA reimbursement form from the New York State Department of Civil Service (below is a picture of the form)

Attach documentation from Social Security showing:

The Medicare Part B premiums paid for the year

Mail the form and documentation to New York State

Receive reimbursement by check

You Can Go Back Up to Four Years to Reclaim Missed IRMAA Reimbursements

If you’re reading this and realizing you’ve been paying IRMAA for years without reimbursement — there’s good news.

New York State allows retirees to go back up to four years to recoup IRMAA premiums already paid.

On the IRMAA reimbursement form, you can:

Check the boxes for each year you were subject to IRMAA

Submit the required Social Security tax documentation for each year

When approved, New York State will issue reimbursement checks for those prior years.

A Simple Annual Reminder Strategy

For our clients who we know will be subject to IRMAA every year, we recommend a very simple system:

Set a recurring reminder for January or February

When your Social Security tax form arrives showing Medicare premiums paid:

Complete the IRMAA reimbursement form

Attach the documentation

Mail it to New York State

That’s it.

New York State does not advertise this process — which is exactly why many retirees miss out on thousands of dollars they’re entitled to receive.

If you’re a New York State retiree — especially one with higher retirement income — understanding this process can mean thousands of dollars back in your pocket every year.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.