Should I Refinance My Mortgage Now?

With all the volatility going on in the market, it seems there is one certainty and that is the word “historical” will continue to be in the headlines. Over the past few months, we’ve seen the Dow Jones Average hit historical highs, the 10-year treasury hit historical lows, and historical daily point movements in the market.

Should I Refinance My Mortgage Now?

With all the volatility going on in the market, it seems there is one certainty and that is the word “historical” will continue to be in the headlines. Over the past few months, we’ve seen the Dow Jones Average hit historical highs, the 10-year treasury hit historical lows, and historical daily point movements in the market. Market volatility will always lead the headlines as it does impact anyone with an investment account. With that in mind, it is important to use these times to reassess your overall financial plan and take advantage of parts of the plan that are in your control.

For a lot of people, their home is their most significant asset and is held for a longer period than any stock or bond they may have. This brings us back to “historical” as mortgage rates continue to drop. Whenever this happens, our clients will call and ask if it makes sense to refinance. In this article, we will help you in making this decision.

3 Important Questions

How much will I be saving annually in interest with a lower rate?

What are the closing costs of refinancing?

How long do I plan on being in the home and how many more years do I have on the mortgage?

If you can answer these questions, then you should have a pretty good idea if it makes sense for you to refinance.

How Much Will I be Saving Annually in Interest with a Lower Rate?

With most financial decisions, dollars matter. So how do you determine how much you will be saving each year with a lower interest rate? Below, I walk through a very basic example, but it will show the possible advantage of the refinance.

One important note with this example is the fact that most loan payments you make will decrease the principal which should decrease the cost of interest. To make this simple, I assume a consistent mortgage balance throughout the year.

Higher Interest Lower Interest

Mortgage Balance: $300,000 Mortgage Balance: $300,000

Interest Rate: 4.5% Interest Rate: 3.5%

Annual Interest: $13,500 Annual Interest: $10,500

By refinancing at the lower rate, the dollar savings in one year was $3,000 in the example when the mortgage balance was $300,000.

Savings over the life of a mortgage at 3.5% compared to 4.5% on a $300,000, 30-year mortgage, should be over $60,000 in interest over that time period if you are making consistent monthly payments.

What are the Closing Costs of Refinancing?

After walking through the exercise above, most people will say “Of course it makes sense to refinance”. Before making the decision, you must consider the cost of refinancing which can vary from person to person and bank to bank. There are several closing costs to consider which could include title insurance, tax stamps, appraisal fee, application fees, etc.

If the cost of closing is $5,000, you will have to determine how long it will take you to make that back based on the annual interest savings. Using the example from before, if you save $3,000 in interest each year, it should take you 2 years to breakeven.

One tip we give clients is to start at your current lender. Banks are in competition with other banks and they usually do not want to lose business to a competitor. Knowing the current interest rate environment, a lot of institutions will offer a type of “rapid refinance” for existing customers which may make the process easier but also give you a break on the closing costs if you are staying with them. This should be taken into consideration along with the possibility of getting an even lower interest rate from a different institution which could save you more in the long run even if closing costs are higher.

How Long do I Plan on Being in the Home and How Many More Years do I have on the Mortgage?

This is important since there is a cost to refinancing your mortgage. If it will take you 10 years to “breakeven” between the closing costs and interest you are saving but only plan on being in the house for 5 more years, refinancing may not be the right choice. Also, if you only have a few years left to pay the mortgage you would have to weigh your options.

In summary, taking advantage of these historical low mortgage rates could save you a lot of dollars over the long term but you should consider all the costs associated with it. Taking the time to answer these questions and shop around to make sure you are getting a good deal should be worth the effort.

Public Service Announcement: Like the stock market, it is hard to say anyone has the capability of knowing for sure when interest rates will hit their lows. Make sure you are comfortable with the decision you are making and if you do refinance try not to have buyer’s remorse if the historical lows today turn into new historical lows next year.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

How To Use Your Retirement Accounts To Start A Business

One of the most challenging aspects of starting a new business is finding the capital that is needed to support your expenses as you begin to build up a revenue stream since it’s not always easy to ask friends and family for money to invest in a startup business. Luckily, for new entrepreneurs, there are some little-known ways on how you can use

One of the most challenging aspects of starting a new business is finding the capital that is needed to support your expenses as you begin to build up a revenue stream since it’s not always easy to ask friends and family for money to invest in a startup business. Luckily, for new entrepreneurs, there are some little-known ways on how you can use retirement accounts as a funding source for your new business. However, before you cash out your 401(k) account to start a business, you have to fully understand the pros and cons of each option.

ROBS Plans

ROBS stands for “Rollover for Business Startups”. ROBS is a special program that allows you to use the balance in your 401(k) or IRA account to fund your new business while avoiding having to pay taxes and the 10% early withdrawal penalty for business owners under age 59.5. Unlike a 401(k) loan that has limits, loan payments, and interest, ROBS plans allow you to use your full retirement account balance without having to enter into a repayment plan.

Why do business owners use ROBS plans?

The benefits are fairly obvious. First off, by using your own retirement assets to fund your new business, you don’t have to ask friends and family for money. Secondly, if you were to embark on the traditional lending route from a bank for your start-up, most would require you to pledge personal assets, such as your house, as collateral for the loan. Doing this puts an added pressure on the new entrepreneur because if the business fails you not only lose the business, but potentially your house as well. By using the ROBS plan, you are only risking your own assets, you have quick and easy access to those funds, and if the business fails, worst case scenario, you just have to work longer than you expected.

Is this too good to be true?

When I explain this funding strategy to new business owners, the question I usually get is, “Why haven’t I heard of these plans before?”, and here are a few reasons why. To begin, you are using retirement plan dollars and accessing the tax benefits, and in doing so there are a lot of complex rules surrounding these types of plans. It’s not uncommon for accountants, third-party administrators, and financial advisors to not know what a ROBS plan is, let alone understand the compliance rules surrounding these plans; thus, it’s rarely presented as a viable option. Over the course of this article we will cover the pros and cons of this funding mechanism.

How do ROBS plans work?

The concept is fairly simple, your retirement account essentially buys shares of stock in your new business which provides the business with the cash needed to grow. You do not have to be a publicly traded company for your retirement account to buy shares, however, you are required to establish your new company as a C-Corp in order for this plan to work.

This process entails incorporating your new business, as well as establishing a new 401(k) plan within that business, that contains the special ROBS features. Then, you can transfer assets from your various retirement accounts into the new 401(k) plan allowing the 401(k) plan to then buy shares in your new company. While this sounds easy, I cannot stress enough that you must work with a firm that fully understands these types of plans and the funding strategy. These plans are perfectly legal, but there are a lot of rules to follow. Since this funding strategy allows you to access retirement account dollars without having to pay tax to the IRS, the IRS will sometimes audit these plans hoping that you did not fully understand or comply with the rules surrounding the establishment and operations of these ROBS plans.

The steps to set up a ROBS plan

Here are the steps for setting up the plan:

1) Establish your new business as a C-Corp.

2) Establish a new 401(k) plan for your new business

3) Process direct rollovers from your 401(k) accounts and IRA accounts into your new 401(k) plan

4) Use the balance in your 401(k) account to purchase shares of the corporation

5) Now you have cash in your business checking account to pay expenses

You must be a C-Corp

The only type of corporate structure that works for a ROBS plan is a C-Corp because only a C-Corp can sell shares of the business to a retirement account legally. That means that LLCs, sole proprietorships, partnerships or even S-Corps will not work for this funding option.

Establishing the new 401(k) plan

ROBS plans have all the same features and benefits of a traditional 401(k) plan, profit-sharing plan, or defined benefit plan, except they also have special features that allow the plan to invest plan assets in the privately held C-Corp.

You need to work with a firm that knows these plans well because not all custodians will allow you to hold shares of a privately held corporation in a qualified retirement account. For many investment firms and custodians, this is considered either a “private placement” or an “alternative investment”. There is typically a special approval process that you must go through with the custodian before they allow your 401(k) account to purchase the shares of stock in your new company. Be ready, there are a lot of mainstream 401(k) providers that will not only not know what a ROBS plan is, but they often times limit the plan investment options to mutual funds; to avoid this, make sure you are aligning yourself with the right provider.

Transferring funds from your retirement accounts to your new 401(k) plan

Your new investment provider should assist you with coordinating the rollovers into your 401(k) account to avoid paying taxes and penalties. Also, if you have 401(K) Roth or after-tax money in your retirement accounts, special preparations need to be made prior to the rollover occurring for those sources.

Purchasing stock in the business

It’s not as easy as simply transferring money into the business checking account since you have to go through the process of issuing shares to the 401(k) account. In most cases, the percentage of ownership attributed to the 401(k) plan is based upon your total funding picture to start up the company. If your retirement accounts are the sole resource to fund the business, then technically your 401(k) plan owns 100% of the company. It’s not uncommon for new business owners to use multiple funding sources including personal savings, funding from friends and family, or a home-equity loan. In these instances, a ROBS plan is still allowed but the plan will own less than 100% of the business.

I don’t want to get too deep in the weeds with this point, but it’s usually advisable not to issue 100% of the shares of the business to your 401(k) plan. This could limit your ability to raise additional capital down the road because you don’t have any additional shares to issue to new investors or to share equity with a new partner.

Using the capital to grow your business

Once the share purchase is complete, the cash will be transferred from your retirement account into the business checking account allowing use those funds to start growing the business.

There is a very important rule when it comes to what you can use these funds for within the new business. First and foremost, you cannot use these funds to pay yourself compensation as the business owner. This is probably the biggest ‘no-no’ associated with these types of plans. The IRS does not want you circumnavigating income taxes and penalties just to pay yourself under a ROBS plan. In order to pay yourself as the business owner, you have to be able to generate revenue from the business. The assets from the stock purchase can be used to pay all of your expenses but before you’re able to take any money out of the business to pay yourself compensation you have to be showing revenue.

Once new business owners hear this, it’s often disheartening. It’s great that they have access to capital to build their business, but how do they pay their bills while they’re building up the revenue stream? Luckily, I have good news on this front. We have additional strategies that we can implement using your retirement accounts outside of the ROBS plan that will allow you to pay yourself compensation as the owner and it can work out better tax wise than paying yourself as a W2 income through the C-corp.

Requirements for ROBS plans

There are a few requirements you have to meet for this funding strategy to work.

1) The funds have to be held in a pre-tax retirement account. This means that money in Roth IRA’s and Roth 401(k)’s are not eligible for this funding strategy.

2) You typically need at least $50,000 in your new 401(k) account for the ROBS plan to make sense since there are special costs associated with establishing and maintaining a ROBS 401(k) plan. If your balance is less than $50,000, the cost to establish and maintain the plan begins to outweigh the benefit of executing this funding strategy.

3) If you’re rolling over a 401(k) plan to fund your ROBS 401(k) plan, it cannot be from a current employer. In other words, if you are still working for a company and you’re running this new business on the side, you are not able to rollover your 401(k) balance into your newly established 401(k) plan and implement this ROBS strategy. The 401(k) account must be coming from a former employer that you no longer work for.

4) You have to be an active employee in the business

There are special IRS rules that define if an employee is actively or materially participating in a business. Since ROBS plans do not work for passive business owners, it is difficult to use these plans for real estate investments unless you can prove that you are an active employee of that real estate corporation. If your new business is your only employer, you work over 1000 hours per year, and it’s your primary source of revenue, then you should not have a problem qualifying as an active employee. If you have multiple businesses however, you really need to consult your accountant and ROBS provider to make sure you satisfy the IRS definition of materially participating.

A ROBS plan can be used for more than just start-ups

While we have talked a lot about using ROBS plans to start up a business, they can also be used for other purposes. These plans can be a funding source to:

1) Buy an existing business

2) Recapitalize a business

3) Build a franchise

These plans can offer fast access to large amounts of capital without having to go through the traditional lending channels.

Cost of setting up and maintaining a ROBS plan

It typically costs $4,000 – $5,000 to set up a ROBS plan and you cannot use the balance in your retirement account to pay this fee. It must be paid with outside funds.

As for ongoing fees, you will have the regular administrative, recordkeeping, and investment advisory fees associated with sponsoring a 401(k) plan which vary from provider to provider. You may also have additional fees charged each year by the custodian for holding the privately held C-Corp shares in your retirement account. Make sure you clearly understand what the custodian will require from you each year to value those shares. If you wind up with a custodian that requires audited financial statements, this could easily run you an additional $8,000+ per year to obtain those audited financial statements from an accounting firm. If you are sponsoring one of these plans, you probably want to try to avoid this large additional cost.

Complications if you have employees

For start-up companies or established companies that have employees that would otherwise be eligible for the 401(k) plan, there are special issues that need to be addressed. The rules within the 401(k) world state that all investment options available within the plan must be made available to all eligible employees. That means if the business owner is able to purchase shares of the company within the retirement plan, the other eligible employees must also be given the same investment opportunity. You can see immediately where this would pose a challenge to the ROBS plan if you have eligible employees.

However, investment options can be changed which is why ROBS plans are the most common in start-ups where there are no employees yet, allowing the 401(k) plan to setup the only eligible plan participant, the business owner, allowing them to buy shares of the company. Once the share purchases are complete, the business owner can then remove those shares as an investment option in the plan going forward.

The Cons of a ROBS plan

Up until now we have presented the advantages of the ROBS plan but there are some disadvantages.

1) The first one is pretty obvious. You are risking your retirement account dollars in a start-up business. If the business fails, not only will you be looking for a new job, but you’ve depleted your retirement assets.

2) You are required to sponsor a C-Corp which may not be the most advantageous corporate structure.

3) You are required to sponsor a 401(k) plan. When running a start-up business, it’s sometimes more advantageous to sponsor a Simple IRA or SEP IRA which requires less cost and time to maintain, but you don’t have that option using this funding strategy.

4) The business owners can’t pay themselves compensation from the stock purchase

5) The cost to setup and maintain the plan. Paying $5,000 just to establish the plan isn’t exactly cheap. Plus, you’re looking at $2,000+ in annual maintenance costs for the plan. Other options like taking a home-equity loan or establishing a Solo 401(K) plan and taking a $50,000 401(k) loan from the plan may be the better funding option.

6) Audit risk. While it’s not the case that all these plans are audited, they do present an audit opportunity for the IRS given the compliance rules surrounding the operation of these plans. However, this risk can be managed with knowledgeable providers.

7) Asset sale of the business becomes complex. If 10 years from now you sell your company, there are two ways to sell it. An asset sale or a stock sale. While a stock sale jives very easily with this ROBS funding strategy, an asset sale becomes more complex.

Summary

Finding the capital to start up a business is never easy. Each funding option comes with its own set of pros and cons. The ROBS plan is just another option for consideration. While I have greatly simplified how these plans work and how they operate, if you are strongly considering using this plan as a funding vehicle for your new business, please reach out to us so we can have an open discussion about what you are trying to accomplish, and how the ROBS plan stacks up against other funding options that you may have available.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Will There Be A Santa Claus Rally This Year?

Going back 120 years, December has traditionally been a very good month for the stock market. Within the last 120 years the S&P 500 has been positive in December 73% of the time. The Russell 2000, which is the index for small cap stocks, has been up 87% of the time in December. This boost in the final month of the year is known to traders as the

Going back 120 years, December has traditionally been a very good month for the stock market. Within the last 120 years the S&P 500 has been positive in December 73% of the time. The Russell 2000, which is the index for small cap stocks, has been up 87% of the time in December. This boost in the final month of the year is known to traders as the “Santa Claus Rally”. Should investors expect a Santa Claus rally in 2018 given the recent sell off in the markets? The answer may hinge on the results of the Federal Reserve Meeting on December 19th.

The Fed Decision

The fate of the Santa Claus rally may very well be in the hands of the Federal Reserve Committee this year. The Committee’s decision regarding the Fed Fund Rate could either cause the market to rally if the Fed decides to keep rates unchanged or it could push the markets lower if they decide to move forward with the anticipated quarter point rate hike. The Fed has a really tough decision to make this year. The goal of the Fed is to keep interest rates at a level that promotes full employment and a target inflation rate of 2%. In periods of economic expansion, it’s the Fed’s job to make sure the economy does not overheat which in turn could lead to prices of goods and services in the U.S. spiraling out of control.

Over the past few years, the U.S. economy has continued to expand and the Fed has been raising rates in quarter point increments. A very slow pace by historic standards. The Fed has already raised the Fed Funds Rate three times in 2018. What are the chances that the Fed raises rates again in December?

Solid Employment & Inflation In Check

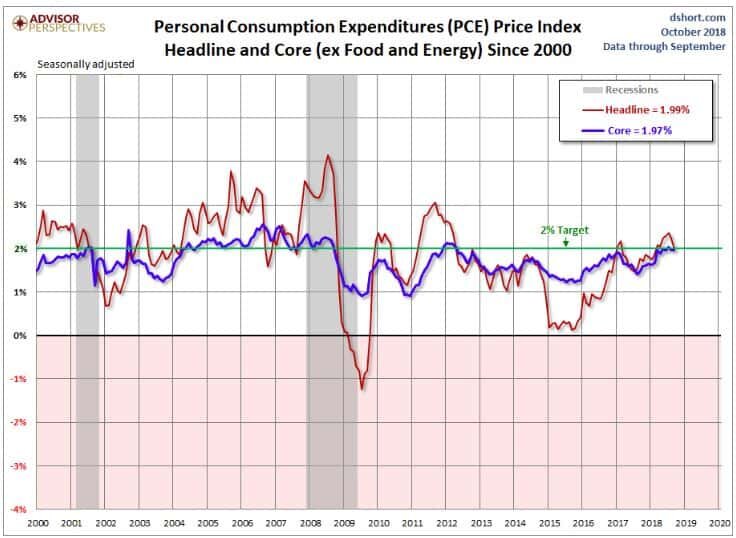

The good news is there is not a lot of pressure for the Fed to raise rates in December. As of October, the unemployment rate sits at 3.7% and the employment data that we have seen throughout November has been strong. Historically, a strong job market usually results in higher wages for employees which is the main driver of inflation. So in the current economic environment, the Fed’s main focus is keeping inflation within its 2% target range. The Fed’s measuring stick for the rate of inflation is the Personal Consumption Expenditures Index. Otherwise known as the “PCE”.

There is a “Headline PCE” and a “Core PCE”. The Core PCE excludes prices for food and energy which is the Fed’s main barometer. Why does the Fed use Core PCE? Food and Energy prices can fluctuate significantly over short periods of time which can distort the results of the PCE index.

Below is a chart of both the Headline PCE and the Core PCE:

As you can see in the chart, the blue line that represents the Core PCE is right below the Fed’s 2% target. The PCE index is reported monthly and in October the PCE came in at a year-over-year change of 1.97%. Also you will see in the chart, due to the drop in the price of oil over the past two months, the Headline PCE is also dropping. While Headline PCE is not the Fed’s main measuring stick, there does seem to be a correlation between Headline PCE and Core PCE. It makes sense because regardless of the price of the product that you are taking a sample of, that product needs to be transported from the producer to the end user, and that transportation cost, which is largely influenced by the price of oil, will have an impact on the price of product within the Core PCE index.

This is good news for the stock market going into the December Fed meeting. With the Core PCE running just below the Fed’s target 2% rate and the Headline PCE declining, there is not a big push for the Fed to raise the Fed Funds Rate in December. I would even make the argument that raising the Fed Funds Rate in December would be a mistake.

The Fed & The Stock Market

The Fed is not a slave to the stock market. It’s not the Fed’s job to make sure the stock market continues to go up. Just because the stock market has experienced a large sell off over the past two months does not mean that the Fed will come to the market’s rescue and not raise rates. But remember, the Fed’s job is to keep the U.S. economy at full employment and keep inflation in check. Since inflation remains in check, it would seem that the prudent decision would be for the Fed to pause in December. If the Fed decides to raise rates in December, I have a difficult time understanding the catalyst for that decision.

Drivers Of The Recent Sell Off

It’s been a frustrating year for investors. Over the past 7 weeks, the U.S. large cap index, mid cap index, and small cap index have forfeited all of their gains for the year. International equity markets have been crushed this year. In a year like this, normally investors could turn to the bond portion of their portfolio for some support but that has not been the case this year either. The Barclays US Aggregate Bond index is down 2.38% year-to-date in 2018. It’s been a return drought this year with a double dose of volatility.

While the rapid rise in interest rates at the beginning of October may have triggered the market sell off, the downturn has been sustained by revisions to the forward guidance offered by corporations within their third quarter earnings report. While it has been another solid quarter of earnings for U.S. corporations, many of the companies that have been leading the bull market rally revised their forward earnings guidance down for the next few quarters. U.S. corporations seem to be embracing the uncertainty created by the trade wars and the tight labor market going into 2019.

It’s important to understand that as of today corporate earnings have not fallen short of expectations. As of November 14, 2018, 456 of the 500 companies in the S&P 500 had reported 3rd quarter earnings. 77.6% of those companies reported earnings above analyst expectations. This is above the long-term average of 64% and in line with the prior four quarter averaging of 77% exceeding expectations.

What really changed was the gross revenue numbers. Of those 456 companies that reported, 60.4% of those companies reported Q3 revenue above analyst expectations. That puts it in-line with the long-term average of 60% but below the average of the prior four quarters at 73%. While the U.S. economy continues to show strength, U.S. corporations have largely built an “earnings buffer” into their forecasts.

Economic Expansions Do Not Die Of Old Age

Everyone is on the lookout for the next recession. Each market sell off that we experience in this prolonged bull market rally makes investors question if they should run for hills. As one would expect, as you enter the later innings of an economic expansion the markets will begin to become more volatile. It’s easy for investors to hold their positions when the markets are going straight up with no volatility like 2017. It’s much more difficult to hold positions when it feels like you’re on a boat, in a storm, in the middle of an ocean. The temptation to try and jump in and out of the market in these volatile market conditions becomes much greater.

It’s very difficult to predict the future direction of the stock market using the recent fluctuations in the stock market as your barometer for future performance. If we look at many of the economic expansions in the past, we historically do not enter recession because the market calls it a day and just decides to go into a downward death spiral. In the past, there was typically a single event or a series of events that caused the economy to go from a period of expansion to a period of contraction. It’s for this reason that during these periods of heightened volatility that we rely heavily on the economic indicators that we track to determine how worried we should really be.

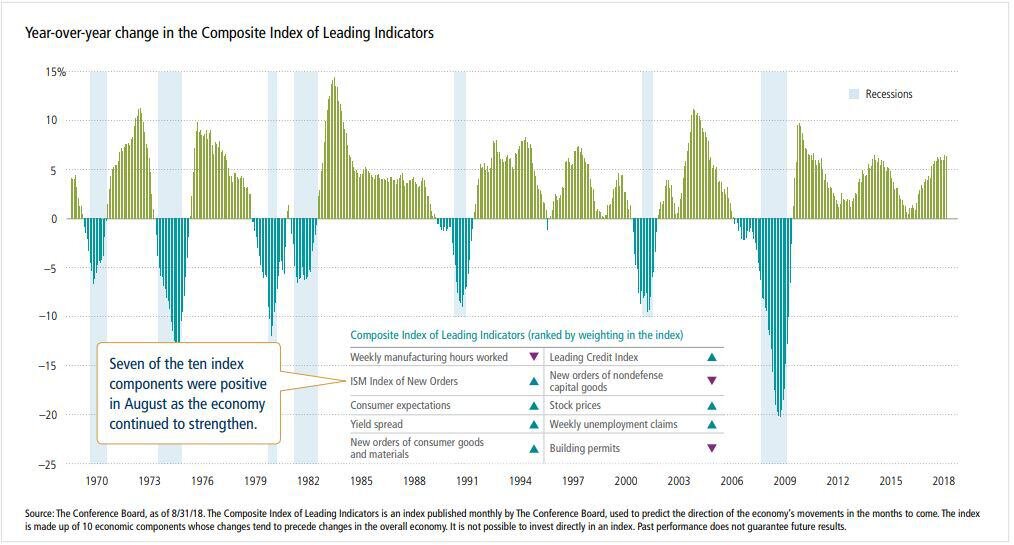

One of the main indicators that we track that I have shown you in previous updates is the Composite of Leading Indicators. It aggregates a number of forward looking economic and market indicators in an effort to provide a measurement of the health of the U.S. economy. See the chart below.

Each of the light blue areas shows when a recession took place going back to 1970. As you will see, in most cases this indicator turned negative before the economy entered a recession. If you look at what this indicator is telling us now, not only is the U.S. economy healthy, but over the past year it has strengthened. If you look at where we are now, there has never been a time since 1970 that this economic indicator has been at its current level, and a recession just shows up out of nowhere 12 months later.

Conclusion

We have no way of knowing what action the Fed will take on December 19th. However, given the tame level of inflation and the 3.7% unemployment rate, we would not be surprised if the Fed pauses at the December meeting which could lead to a health rally for the markets in December. Even if the Fed throws the market a curve ball and moves forward with the quarter point rate hike, while this move may seal the markets hopes of posting a positive return for the 2018 calendar year, the economy is still healthy, the probability of a recession within the next 12 months is still very low, and interest rates, although rising, are still at historically low levels. This economic environment may reward investors that have the discipline to make sound investment decision during these periods of heightened market volatility. The “easy years” are clearly behind us but that does not mean that the economic expansion is over. Have a safe and happy Thanksgiving everyone!!

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

The House Passed The Tax Bill. What's The Next Step?

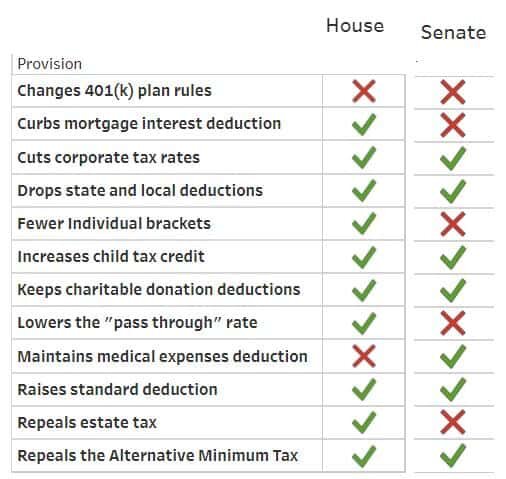

Last night the house passed the Tax Cut & Jobs Act Bill with ease. Next up is the Senate vote. It’s important to understand the House and the Senate are voting on two different tax reform bills. Below is a chart illustrating the main differences between the House version and the Senate version of the tax reform bill.

Last night the house passed the Tax Cut & Jobs Act Bill with ease. Next up is the Senate vote. It’s important to understand the House and the Senate are voting on two different tax reform bills. Below is a chart illustrating the main differences between the House version and the Senate version of the tax reform bill.

As you can see, there are a number of dramatic differences between the two bills. The easy part was getting the House to approve their version because the Republican Party own 239 of the 435 seats. In other words, they own 55% of the votes.

The Senate Vote

Next, the Senate will put their tax reform bill to a vote. The vote is expected to take place during the week of Thanksgiving. However, in the Senate , which the Republican have the majority, they only have 52 of the 100 seats. In this case, they would need at least 50 “Yes” votes to get the bill approved in the senate. It’s 50, not 51 votes, because in the event of a “tie”, the Vice President gets a vote to break the tie and he is likely to vote “Yes” to keep tax reform moving along.

Reconciliation Process

Once the House and Senate have approved their own separate tax bills, they will then have to begin the reconciliation process of blending the two bills together. This will be the difficult part. The two tax bills are dramatically different so there will be a fair amount of grappling between the House and the Senate committees as to which features stay and which features get tossed out or adjusted as part of the final tax bill. In the end, the final tax reform bill cannot add more than $1.5 Trillion to the national debt over the next 10 years. Otherwise, the bill would need to return to the Senate and would require “60” votes to approve the bill. There is a slim too no chance of that happening.

Tax Reform by Christmas

President Trump wants the bill on his desk to sign into law before Christmas. While it seems likely that the Senate will pass their tax bill next week, the battle will take place in the reconciliation process that will begin immediately after that vote. It’s a tall order to fill given that there are only six weeks left in the year and how different the two bills are in their current form. However, don’t underestimate how badly the Republican party wants to put a run on the scoreboard before the end of the year. If they get tax reform through in the last week of the year, it’s an understatement to say that it will be an intense final week of December for year-end tax planning. Stay tuned for more………

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Can I Negotiate A Car Lease Buyout?

The short answer is "yes", but the approach that you take will most likely determine whether or not you are successful at purchasing your vehicle for a lower price than the amount listed in the lease agreement. When you lease a car, the lease agreement typically includes an amount that you can purchase the car for at the end of the lease. That amount is

The short answer is "yes", but the approach that you take will most likely determine whether or not you are successful at purchasing your vehicle for a lower price than the amount listed in the lease agreement. When you lease a car, the lease agreement typically includes an amount that you can purchase the car for at the end of the lease. That amount is essentially a guess by the bank that is providing the financing for the lease as to what the future value of your vehicle will be at the end of the lease.

Lease Buyout Calculation

Step number one in the negotiation process is to determine what your vehicle is worth. Did the bank guess right or wrong? If the purchase amount in your lease agreement is $25,000 but you find that the vehicle, based on current market conditions, is only worth $18,000, you probably have room to negotiate the purchase price of your vehicle but you have to do your homework. Compare your vehicle's purchase price to the retail value of local auto dealers. If you can show the bank that there is a local auto dealer trying to sell the exact make and model of your leased car with similar mileage, the bank will be more likely to accept a lower purchase price realizing that they guessed wrong.

Deal Directly With The Bank

You may have noticed that I continue to reference the "bank" in the negotiation process and not the "dealer". This is intentional. Some leasing banks allow dealers to increase the cost of the lease buyout to make a profit. Dealers can also charge document fees, which are taxable in most states. It may also be advantageous to line up your own financing for the lease purchase amount before entering into the negotiation process. If the dealer arranges the financing for you, it can sometimes increase your interest rate to make more money on the purchase. By dealing directly with the leasing bank you can cut out these additional costs.

You Make The Offering Price

Start by making an offer to the leasing bank based on your market research. Also make sure you contact the leasing bank well in advance of the lease "turn-in date". The bank may not be able to provide you with an immediate response to your offer so give yourself plenty of time for the negotiation process to work.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog. I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.