What Retirees Regret Most About the First 10 Years of Retirement

The first decade of retirement offers some of your greatest opportunities. Learn the most common regrets retirees share and how thoughtful planning can help you avoid them.

Ask retirees what they wish they had done differently, and you'll hear many of the same answers.

Rarely do they say they wish they had saved more after retirement.

More often, they regret waiting.

Waiting to travel. Waiting to spend. Waiting to make tax planning decisions. Waiting to enjoy the freedom they spent decades working toward.

While every retirement is different, a few common regrets come up time and time again.

1. Claiming Social Security Too Early

Many retirees claim Social Security as soon as they're eligible without fully understanding how the decision affects lifetime income.

Claiming early can make sense in certain situations, but for others, waiting may provide:

Higher lifetime benefits.

Greater survivor benefits for a spouse.

More guaranteed income later in life.

This is one of the most permanent retirement decisions you'll make, so it's worth evaluating carefully.

2. Being Too Conservative With Investments

It's natural to become more cautious after retiring.

However, some retirees become so conservative that their portfolios struggle to keep pace with inflation.

The goal isn't to avoid all market risk.

It's to build an investment strategy that supports decades of retirement while still providing growth potential.

3. Waiting Too Long to Travel

Many retirees plan to travel "someday."

Unfortunately, health issues often become a limiting factor before finances do.

Example

A couple spends the first eight years of retirement delaying international travel because they're worried about market volatility.

By the time they feel financially comfortable, one spouse develops mobility challenges that make those trips much more difficult.

Key Insight

Your healthiest retirement years are often your most valuable. Don't assume they'll last forever.

4. Delaying Roth Conversions

Many retirees spend the years between retirement and Required Minimum Distributions (RMDs) in relatively low tax brackets.

Some never take advantage of that window.

Later, large RMDs increase:

Taxable income.

Medicare premiums.

Taxes paid by surviving spouses.

Tax burdens for heirs.

Proactive tax planning early in retirement can create flexibility later.

5. Not Simplifying Their Finances

Over the years, it's easy to accumulate:

Multiple retirement accounts.

Old 401(k)s.

Several brokerage accounts.

Numerous bank accounts.

Insurance policies that no longer serve a purpose.

Many retirees wish they had simplified sooner.

Consolidating accounts doesn't just reduce paperwork. It can make managing finances easier for both spouses and eventually for family members.

6. Focusing So Much on Saving That They Forgot to Enjoy Retirement

Perhaps the most common regret has little to do with money.

Many retirees realize they spent decades preparing for retirement but struggled to actually enjoy it.

They postponed experiences because they were afraid of spending too much.

Years later, they recognized they had far more financial security than they believed.

A good retirement plan should provide confidence, not just caution.

Learn While You Have Options

One reason these regrets are so common is that many retirement decisions become harder to change over time.

The first decade of retirement often provides the greatest flexibility for:

Tax planning.

Travel.

Spending decisions.

Lifestyle changes.

Charitable giving.

Family experiences.

Making thoughtful decisions early can have benefits for years to come.

Common Theme: Waiting Too Long

Although every retiree's story is different, many regrets come back to the same idea.

"I wish we hadn't waited."

Whether it's traveling, spending, simplifying finances, or reducing future taxes, opportunities are often greatest when you're healthy and have the most flexibility.

Planning Helps Turn Regret Into Confidence

No retirement plan will eliminate every surprise.

But thoughtful planning can reduce the chances of looking back and wishing you had made different decisions.

At Greenbush Financial Group, we encourage clients to think beyond investment returns. Retirement is about making the most of your time, your resources, and the opportunities that matter most while you still have them.

Final Thoughts

The first 10 years of retirement are often called the "go-go years" for a reason.

They're typically the years when retirees have the most freedom, energy, and flexibility.

Looking back, many retirees don't regret spending too much.

They regret waiting too long to do the things they had always planned to do.

A well-designed retirement plan should help you protect your future while giving you the confidence to enjoy the present.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

- What's the biggest regret retirees have?Many retirees say they waited too long to travel, spend on meaningful experiences, or make important financial planning decisions.

- Is claiming Social Security early always a mistake?No. The best claiming age depends on your health, marital status, income needs, and overall retirement plan.

- Why are the first 10 years of retirement so important?For many people, these are the healthiest and most active years of retirement, making them an ideal time for travel, hobbies, and proactive financial planning.

- Why do retirees regret delaying Roth conversions?Converting retirement assets during lower-income years may reduce future RMDs and lifetime taxes. Waiting can mean losing that planning opportunity.

- How can I avoid common retirement regrets?Create a comprehensive retirement plan that addresses not only investments but also taxes, spending, healthcare, and your personal goals for retirement.

When Retirement Goes Better Than Planned: The Tax Problems of Having Too Much Money

Retirement planning becomes more complex as income, taxes, Social Security, healthcare, and withdrawals begin working together. Learn the signs that professional coordination may help reduce costly mistakes.

For decades, retirement planning has centered around one question:

"Will I have enough?"

It's an understandable concern. No one wants to outlive their savings.

But after working with hundreds of retirees, we've noticed another problem that receives far less attention:

What happens when retirement goes better than expected?

Many retirees discover they saved diligently, invested wisely, spent less than anticipated, and watched their portfolios continue to grow throughout retirement. While that's certainly preferable to running out of money, it can create a new set of planning challenges.

Large retirement accounts, growing investment portfolios, and conservative spending habits often lead to higher taxes, increased Medicare premiums, and more complicated estate planning.

In other words, financial success can create tax inefficiencies if it isn't managed strategically.

Why More Money Doesn't Always Mean More Financial Flexibility

Accumulating wealth is only one part of retirement planning.

The other part is figuring out how to use that wealth efficiently.

Many retirees assume that if they don't need to withdraw money from their retirement accounts, they'll simply leave it invested. Unfortunately, the IRS has other plans.

Once Required Minimum Distributions (RMDs) begin, retirees lose much of their control over the timing of taxable withdrawals.

Even if they don't need the income, they're generally required to take distributions from traditional IRAs and many employer-sponsored retirement plans.

Those distributions can create a ripple effect across nearly every aspect of a retirement plan.

The Challenge of Large Required Minimum Distributions

For retirees with substantial tax-deferred savings, RMDs often become the biggest source of taxable income later in retirement.

What starts as a manageable annual withdrawal can grow significantly over time if investment returns outpace distributions.

Example

Mark retires at age 65 with:

$2.8 million in traditional retirement accounts

A paid-off home

A pension

Social Security benefits

He doesn't need to touch his IRA during his first several years of retirement.

By the time RMDs begin, his account has grown to more than $4 million.

Now he's required to withdraw well over $150,000 annually, regardless of whether he needs the money.

Those withdrawals increase:

Federal taxable income

State taxable income (where applicable)

Medicare premiums

Taxes on investment income

Ironically, delaying withdrawals because he didn't need the money ultimately resulted in larger taxable distributions.

Key Insight

Sometimes the biggest tax bill isn't caused by poor planning. It's caused by successful investing combined with years of deferred taxation.

Medicare IRMAA Can Turn Success Into Higher Healthcare Costs

Many retirees are surprised to learn that Medicare isn't priced the same for everyone.

Higher-income retirees pay Income-Related Monthly Adjustment Amount (IRMAA) surcharges on:

Medicare Part B

Medicare Part D

As retirement income increases, so do Medicare premiums.

Large RMDs are one of the most common reasons retirees unexpectedly cross into higher IRMAA brackets.

Unlike income taxes, these higher premiums often feel like an additional tax on retirement success.

Conservative Spending Can Create Bigger Tax Problems Later

Many retirees underspend because they're worried about the future.

They postpone vacations.

Delay home improvements.

Skip experiences they've always wanted.

Meanwhile, their retirement accounts continue growing.

While financial discipline is admirable, consistently spending far less than your plan allows can unintentionally increase future tax liabilities.

Example

Susan budgets $130,000 annually for retirement but only spends about $75,000 because she's afraid of running out of money.

As a result:

Her IRA continues growing.

Future RMDs become much larger.

She pays more in taxes.

Medicare premiums increase.

She ultimately leaves a larger tax-deferred account to her children.

The money she spent decades saving may eventually be taxed at higher rates than if she had withdrawn it more strategically during retirement.

A Large Traditional IRA May Not Be the Gift You Think It Is

Many retirees view their IRA as a legacy for their children.

While those accounts can certainly provide meaningful inheritances, they also come with tax consequences.

Under current law, most non-spouse beneficiaries must fully distribute inherited retirement accounts within ten years.

For adult children in their peak earning years, those required withdrawals can push them into much higher tax brackets.

Example

A daughter earning $250,000 inherits a $1.5 million traditional IRA.

Over the next ten years, she must withdraw those funds according to current distribution rules.

Those withdrawals may be taxed at some of the highest marginal rates she'll ever pay.

Meanwhile, a Roth IRA inherited under similar circumstances may provide significantly greater tax flexibility.

Important Note

Leaving pre-tax retirement assets to heirs often transfers a future tax liability along with the inheritance.

Tax Diversification Matters Just as Much as Investment Diversification

Many retirees have diversified portfolios but not diversified tax treatment.

It's common to see wealth concentrated in:

Traditional IRAs

401(k)s

403(b)s

While these accounts provide valuable tax deferral during working years, relying too heavily on them can reduce flexibility in retirement.

A diversified retirement income strategy may include assets held in:

Tax-deferred accounts

Roth accounts

Taxable brokerage accounts

Cash reserves

Having multiple sources of retirement income allows retirees to better manage taxable income from year to year.

Why Roth Conversions Become More Valuable

One of the best opportunities to manage future taxes often occurs before RMDs begin.

Many retirees experience several years between retirement and the start of mandatory distributions when taxable income is relatively low.

These years may provide an opportunity to convert portions of traditional retirement accounts into Roth IRAs.

The goal isn't simply to reduce taxes this year.

Instead, Roth conversions may help:

Reduce future RMDs.

Lower lifetime taxable income.

Improve Medicare premium planning.

Leave more tax-efficient assets to heirs.

Increase flexibility when generating retirement income.

Every conversion should be evaluated within the context of the retiree's overall tax situation and long-term objectives.

The Emotional Side of Having "Too Much"

Many retirees struggle with a mindset they developed during decades of saving.

They spent their careers accumulating wealth.

Then retirement arrives, and they're suddenly expected to spend it.

That's easier said than done.

Some retirees continue saving out of habit, even when they have more than enough to support their lifestyle.

Others hesitate to enjoy experiences they've worked decades to afford because they're focused on preserving every dollar.

Financial security is important.

But retirement planning should also support the life those savings were meant to fund.

Common Mistakes Successful Retirees Make

Retirees with significant assets often make similar planning mistakes, including:

Assuming tax-deferred always means tax-free.

Waiting until RMDs begin before addressing taxes.

Focusing only on investment returns instead of after-tax income.

Ignoring future Medicare premium increases.

Leaving large traditional IRAs to children without considering the tax burden.

Becoming so focused on preserving wealth that they never enjoy it.

Planning Strategies for High-Net-Worth Retirees

Every situation is unique, but retirees with substantial assets should regularly evaluate strategies such as:

Multi-year Roth conversion planning.

Coordinating withdrawals across different account types.

Harvesting capital gains strategically.

Qualified Charitable Distributions (QCDs) after becoming eligible.

Reviewing estate plans alongside tax projections.

Modeling lifetime taxes instead of focusing only on annual tax returns.

The objective isn't necessarily to minimize taxes every year.

It's to reduce taxes over the course of retirement while creating greater flexibility for both retirees and their heirs.

More Wealth Should Create More Choices

One of the greatest benefits of financial success is flexibility.

Unfortunately, taxes can quietly reduce that flexibility if they aren't considered alongside investment performance.

Retirement planning doesn't end once you've accumulated enough assets.

In many ways, that's when some of the most important decisions begin.

At Greenbush Financial Group, we often remind clients that successful retirement planning isn't measured by the size of a portfolio. It's measured by how efficiently that wealth supports your lifestyle, your family, and your long-term goals.

Final Thoughts

Running out of money isn't the only retirement risk.

For many successful retirees, accumulating substantial wealth creates a different challenge: managing taxes, Medicare costs, Required Minimum Distributions, and legacy planning in a tax-efficient way.

With thoughtful planning, retirees may be able to reduce lifetime taxes, preserve greater flexibility, and leave a more efficient legacy for future generations. The goal isn't simply to build wealth. It's to make the most of it.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

- Can you have too much money in a traditional IRA?While it's difficult to have "too much" money, very large traditional IRAs can lead to substantial Required Minimum Distributions and higher lifetime taxes if no planning is done.

- Why do large RMDs increase taxes?Required Minimum Distributions are generally taxed as ordinary income. Larger distributions can push retirees into higher tax brackets, increase Medicare premiums, and affect other tax calculations.

- Should wealthy retirees still consider Roth conversions?In many cases, yes. Roth conversions may help reduce future RMDs, improve tax diversification, and create more tax-efficient inheritances. The right strategy depends on the retiree's projected tax situation.

- Can leaving an IRA to my children create tax problems?Potentially. Most non-spouse beneficiaries must distribute inherited retirement accounts within ten years under current law, which can increase their taxable income during peak earning years.

- Is underspending in retirement a problem?It can be. While spending conservatively provides peace of mind, consistently underspending may lead to larger retirement account balances, higher future RMDs, and missed opportunities to enjoy retirement.

- What's the difference between investment success and tax efficiency?Investment success focuses on growing assets. Tax efficiency focuses on how much of those assets you actually keep after taxes over your lifetime and how efficiently they're passed to future generations.

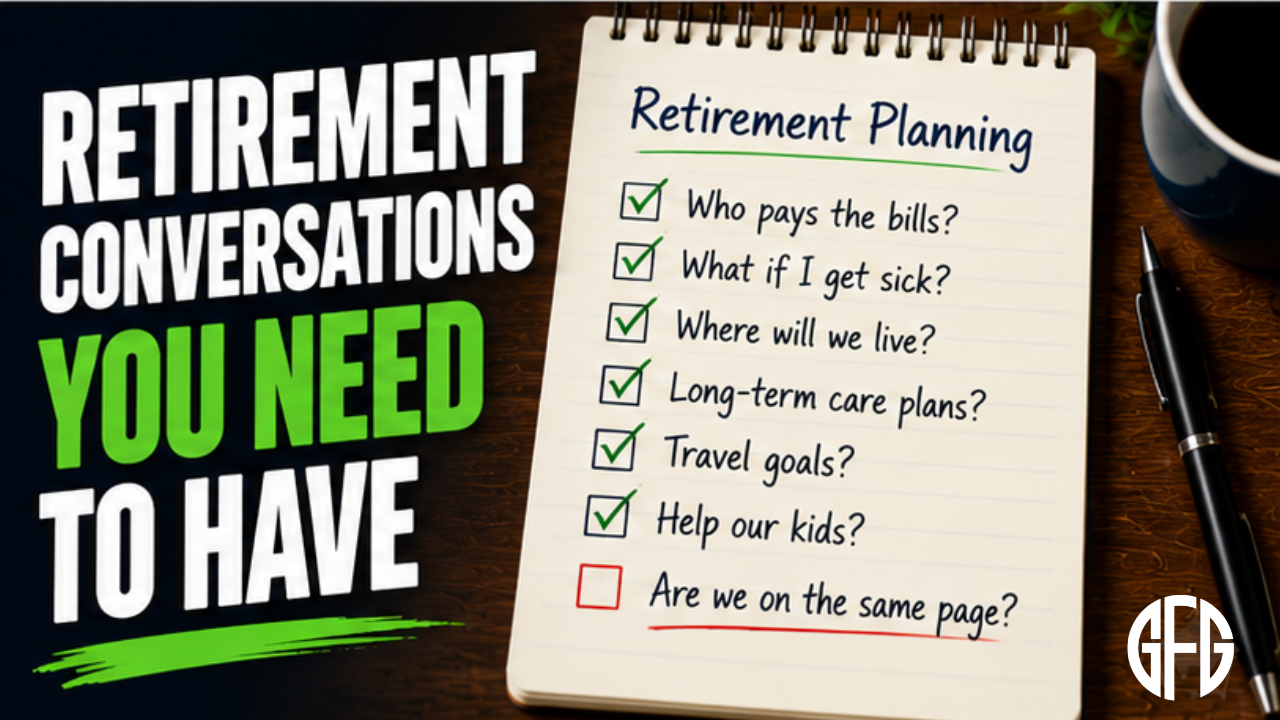

The Retirement Conversations Every Couple Should Have Before It's Too Late

Retirement planning isn't just about saving money. Learn the essential conversations every couple should have about finances, healthcare, spending, and legacy before life forces difficult decisions.

Most couples spend time preparing for retirement by saving, investing, and updating estate planning documents.

But many overlook something just as important:

Having meaningful conversations about what retirement should actually look like.

These aren't discussions about wills or powers of attorney. They're conversations about expectations, responsibilities, and what each spouse wants if life doesn't go according to plan.

Having them early can make future decisions much easier.

1. Who Handles the Finances?

In many households, one spouse naturally takes the lead on financial matters.

That's perfectly fine, until that person becomes ill or passes away.

Ask yourselves:

Do both spouses know where the accounts are?

Can each person pay the bills if necessary?

Does each spouse know who to call for financial or tax advice?

Are important documents easy to find?

The goal isn't for both spouses to do everything. It's to ensure neither feels overwhelmed if circumstances change.

2. What Happens If One of Us Becomes Incapacitated?

Retirement planning isn't just about death. It's also about the possibility that one spouse may be unable to make financial or healthcare decisions.

Discuss questions like:

Who will manage the finances?

When should family members become involved?

Would you prefer to stay at home if possible?

Who should make medical decisions?

These conversations are easier before they're needed.

3. How Do We Want to Spend Our Money?

It's common for spouses to have different priorities.

One may value travel, while the other prefers financial security.

Talk about:

Travel goals

Major purchases

Helping children or grandchildren

How much flexibility your retirement budget should have

A shared vision helps reduce disagreements later.

4. How Much Do We Want to Leave to Our Children?

Many retirees want to leave an inheritance.

But it's worth asking:

Is leaving a large estate our highest priority?

Would we rather spend more on experiences together?

Should we help family members while we're living?

There isn't a right answer, but there should be a shared one.

5. What Are Our Long-Term Care Preferences?

Few people enjoy talking about aging.

Unfortunately, avoiding the conversation doesn't make the decisions easier.

Consider discussing:

Would you prefer care at home if possible?

When would assisted living make sense?

How would care be paid for?

Who should be involved in those decisions?

Knowing each other's wishes can remove uncertainty during an emotional time.

6. What Does Retirement Success Look Like?

Not everyone defines a successful retirement the same way.

For one spouse, it may mean traveling the world.

For another, it could mean spending more time with family or volunteering.

Talk about:

What excites you most about retirement?

What worries you?

What do you want your days to look like?

What goals do you still hope to accomplish?

These conversations help ensure you're planning for the same future.

Don't Wait for a Crisis

Many couples don't have these conversations until a health issue or unexpected loss forces them to.

By then, decisions are often made under stress and with limited time.

Talking through these topics while you're both healthy gives you the opportunity to think clearly and update your plans as your priorities evolve.

Common Mistakes Couples Make

Some of the most common oversights include:

Assuming the other spouse knows all the financial details.

Avoiding difficult conversations about aging.

Never discussing spending priorities.

Failing to communicate healthcare preferences.

Waiting until a crisis to involve adult children.

A Financial Plan Should Reflect Both Spouses

A retirement plan is more than numbers on a page.

It should reflect your shared goals, values, and priorities.

At Greenbush Financial Group, we've found that some of the most valuable client meetings aren't about investment performance. They're the ones where couples gain clarity about the future they want to build together.

Final Thoughts

Estate planning documents are essential, but they can't replace honest conversations.

The more you understand each other's expectations today, the more confident you'll feel navigating whatever retirement brings tomorrow.

Those conversations may be some of the most valuable planning you ever do.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

- When should couples have these conversations?Ideally before retirement, but it's never too late. The earlier you discuss expectations, the more time you have to make thoughtful decisions together.

- What if one spouse handles all the finances?That's common, but both spouses should understand the family's financial picture and know where important information is kept.

- Should adult children be included in these discussions?Not always. However, if they may eventually help with financial or healthcare decisions, involving them at the appropriate time can be beneficial.

- Are these conversations a substitute for estate planning?No. They complement legal documents like wills, trusts, and powers of attorney by helping couples communicate their wishes before decisions need to be made.

- How often should couples revisit these discussions?Every few years or after major life events such as retirement, health changes, the birth of grandchildren, or the death of a loved one.

Should You Spend More in Retirement? The Case for Enjoying Your Money

Retirement planning becomes more complex as income, taxes, Social Security, healthcare, and withdrawals begin working together. Learn the signs that professional coordination may help reduce costly mistakes.

One of the biggest surprises in retirement isn't that people spend too much.

It's that many spend too little.

After decades of saving and living within a budget, it can be difficult to switch from accumulating wealth to spending it. Even retirees with healthy portfolios often hesitate to travel, remodel their home, or enjoy experiences they've worked their entire lives to afford.

Being financially responsible is important. But if fear keeps you from enjoying retirement, it may be time to revisit your plan.

Why Many Retirees Underspend

Saving becomes a habit over a 30- or 40-year career. Retirement requires a different mindset.

Common reasons retirees spend less than they could include:

Fear of running out of money

Concern about future healthcare costs

Uncertainty about market downturns

A desire to leave as much as possible to their children

These are valid concerns, but they shouldn't automatically prevent you from enjoying your retirement years.

How Do You Know If You Can Spend More?

The answer isn't based on your account balance alone.

Instead, it comes down to whether your financial plan shows your income and assets can support your goals over the long term.

Some encouraging signs include:

Your retirement income consistently exceeds your spending.

Your portfolio continues to grow despite withdrawals.

You've planned for healthcare and long-term care costs.

Your withdrawals remain well within sustainable levels.

If that's the case, spending a little more may not jeopardize your financial security.

The Cost of Waiting

Many retirees postpone experiences until "someday."

They delay travel, put off family vacations, or avoid spending on hobbies because they're worried they'll need the money later.

The reality is that your ability to enjoy those experiences may decline with age.

Example

Jim and Linda planned to travel extensively in retirement but kept delaying trips because the market felt uncertain.

By their late 70s, health issues made many of those trips unrealistic.

Their savings had grown well beyond what they expected, but the opportunities they had planned for were no longer available.

Key Insight

Money can often be replaced through investment returns. Time cannot.

Spending More Doesn't Mean Spending Carelessly

This isn't an argument for reckless spending.

It's about spending intentionally on the things that matter most.

That could mean:

Traveling while you're healthy.

Helping grandchildren with education.

Renovating your home to age in place.

Pursuing hobbies or lifelong interests.

Creating meaningful family experiences.

The goal isn't to spend more simply because you can. It's to use your money in ways that improve your quality of life.

Don't Let Taxes Make the Decision for You

Ironically, spending too little can sometimes create larger tax issues later.

If you rarely withdraw from traditional retirement accounts, those balances may continue growing until Required Minimum Distributions (RMDs) force larger taxable withdrawals.

In some cases, strategic withdrawals earlier in retirement can improve long-term tax efficiency while also providing money to enjoy retirement.

Balancing Lifestyle and Legacy

Many retirees want to leave an inheritance, and that's a worthwhile goal.

But it's also important to ask:

Are you sacrificing the retirement you envisioned to leave behind more than your family expects or needs?

In many families, children would rather see their parents enjoy retirement than leave the largest possible inheritance.

A thoughtful financial plan can help balance both objectives.

Common Signs You're Underspending

You may be living more conservatively than necessary if:

You're consistently spending less than your financial plan anticipated.

Your portfolio continues growing year after year.

You regularly postpone meaningful purchases out of fear.

You avoid experiences you've always wanted despite being financially able to afford them.

These patterns don't automatically mean you should spend more, but they're worth discussing with your financial advisor.

Planning Creates Confidence

The best spending decisions aren't driven by emotion. They're supported by a well-designed retirement plan.

When you understand how much you can safely spend, you're less likely to make decisions based solely on fear.

At Greenbush Financial Group, we believe retirement planning isn't just about preserving wealth. It's about helping clients use their resources to create the retirement they've spent decades working toward.

Final Thoughts

Saving for retirement requires discipline. Enjoying retirement requires confidence.

If your financial plan shows you have more than enough, it may be time to give yourself permission to spend on the people, experiences, and goals that matter most.

After all, the purpose of building wealth isn't simply to accumulate it. It's to use it to support a fulfilling retirement.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Frequently Asked Questions

- Is it common for retirees to underspend?Yes. Research consistently shows many retirees spend less than they can afford because they're concerned about outliving their savings.

- How can I tell if I'm spending too little?A retirement income plan can project whether your current spending is sustainable. If your assets continue growing despite withdrawals, you may have room to spend more.

- Should I prioritize spending or leaving an inheritance?It depends on your goals. Most retirees can strike a balance between enjoying retirement and leaving a meaningful legacy with proper planning.

- Can spending too little create tax problems?Potentially. Delaying withdrawals from traditional retirement accounts can lead to larger RMDs and higher taxes later in retirement.

- What's the biggest mistake retirees make with spending?Many assume they need to preserve every dollar, even when their financial plan shows they can comfortably afford to enjoy more of their retirement.

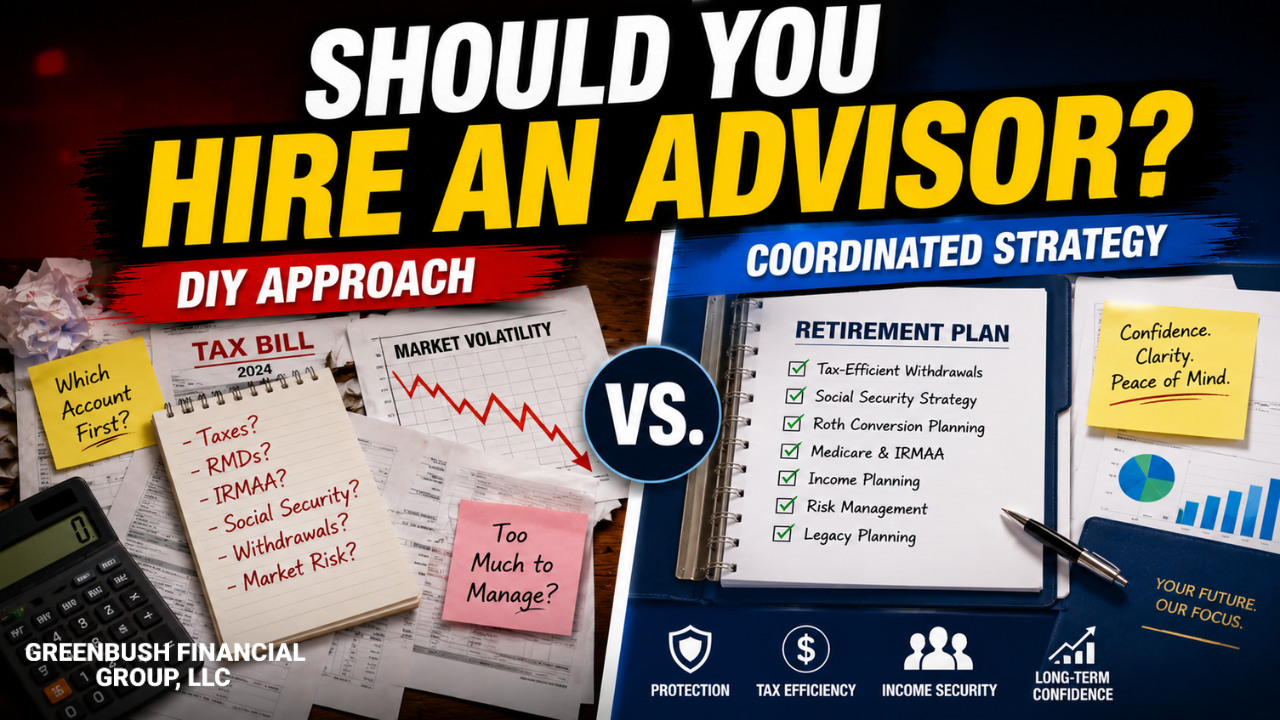

The Closer You Get to Retirement, the More Expensive Mistakes Become

Retirement planning becomes more complex as income, taxes, Social Security, healthcare, and withdrawals begin working together. Learn the signs that professional coordination may help reduce costly mistakes.

Many people successfully manage their finances for decades while saving for retirement. But as retirement approaches, decisions around taxes, Social Security, healthcare, withdrawals, and income planning become more interconnected and harder to reverse. The question is not whether someone is smart enough to manage retirement alone. The question is whether the complexity of retirement planning has reached the point where professional coordination could improve outcomes. At Greenbush Financial Group, we often find that retirees seek guidance not because they lack discipline, but because retirement introduces decisions that can affect income, taxes, and financial confidence for decades.

Retirement Planning Changes Once Paychecks Stop

Many successful professionals and disciplined investors manage their finances perfectly well during their working years.

Saving for retirement is often relatively straightforward:

Earn income

Contribute to retirement accounts

Invest consistently

Avoid major mistakes

Retirement changes the equation.

Now the questions become:

Which accounts should income come from first?

When should Social Security begin?

How do Roth conversions fit into the plan?

How much cash should be kept available?

How do withdrawals affect taxes?

What happens if markets decline early in retirement?

Would a surviving spouse still be financially secure?

This is why many people who comfortably handled accumulation planning begin questioning whether retirement distribution planning requires additional coordination.

Hiring a financial advisor is not about intelligence.

It is about complexity.

Retirement Planning Is More Than Investment Management

One of the biggest misconceptions about financial advisors is that their role is simply picking investments.

For retirees and pre-retirees, the larger value often comes from coordinating multiple moving parts together.

Retirement Planning Often Involves:

Income withdrawal sequencing

Social Security timing

Roth conversion analysis

Medicare IRMAA planning

Tax-efficient withdrawals

Required Minimum Distribution (RMD) planning

Survivor planning

Estate coordination

Long-term care considerations

Investment allocation

Sequence-of-returns risk management

As retirement approaches, these decisions begin affecting one another.

That complexity is often what pushes people toward seeking professional guidance.

Some People May Not Need a Financial Advisor

This is important to acknowledge honestly.

Not every retiree needs ongoing financial advisory services.

Some households may have:

Simple financial situations

Strong financial knowledge

Minimal tax complexity

Pension income covering most expenses

Small withdrawal needs

Comfort managing investments independently

For disciplined retirees with straightforward situations, DIY retirement planning may work perfectly well.

The question is not:

“Can someone manage their own finances?”

The better question is:

“Has retirement planning become complex enough that coordination mistakes could become expensive?”

Why Retirement Mistakes Become More Expensive Later

During working years, mistakes are often easier to recover from because future earnings continue.

Retirement changes that dynamic.

Once paychecks stop:

Tax mistakes can compound

Poor withdrawal timing becomes harder to reverse

Market declines may affect withdrawals

Social Security decisions become permanent

Healthcare costs become more important

Sequence risk matters more

The closer someone gets to retirement, the fewer opportunities there may be to correct major planning errors later.

7 Signs Retirement Planning May Be Becoming Too Complex to Handle Alone

1. You’re Unsure How to Create Retirement Income

Many retirees know how to save.

Far fewer know how to create sustainable retirement income.

Questions often include:

Which account should I withdraw from first?

How much cash should I keep?

Should I delay Social Security?

How do taxes affect withdrawals?

If retirement income feels improvised instead of coordinated, that may indicate planning complexity has increased.

2. You Have Large IRA Balances

Large pre-tax retirement accounts can create future tax issues many retirees underestimate.

Potential concerns include:

Large RMDs later

Higher Medicare premiums

Widow’s tax trap

Increased Social Security taxation

This is where Roth conversion planning often becomes important.

The challenge is not just reducing taxes this year.

It is coordinating taxes across decades.

3. One Spouse Handles Most Financial Decisions

This is extremely common.

Often one spouse manages:

Investments

Taxes

Bills

Account access

Financial planning

That system may work well until a health issue or death creates a sudden transition.

Many couples seek financial guidance because they want:

Shared understanding

Organized planning

Continuity for the surviving spouse

Good retirement planning should work for both spouses, not just the financially engaged one.

4. You’re Concerned About Market Volatility Near Retirement

Market declines feel different once retirement approaches.

During working years, paychecks continue.

Near retirement, people often worry:

“What happens if the market drops right after I retire?”

“How much risk should I still take?”

“Should I move more to cash?”

These concerns are reasonable.

A strong retirement plan balances:

Growth

Income

Cash reserves

Withdrawal flexibility

Emotional comfort

Not just investment returns.

5. You’re Unsure About Social Security Timing

Social Security decisions can permanently affect:

Household income

Survivor benefits

Taxes

Withdrawal needs

Many retirees underestimate how much claiming timing affects long-term outcomes.

Especially for married couples, survivor planning becomes critical.

6. Your Financial Life Has Become More Complicated

Complexity often increases because of:

Business sales

Inheritances

Multiple investment accounts

Real estate holdings

Pension decisions

Stock compensation

Widow/widower concerns

Blended families

At a certain point, coordination becomes more valuable than simply managing investments independently.

7. You’re Worried You May Be Missing Something Important

This may be the most common reason retirees seek help.

Not because they feel incapable.

But because retirement decisions become interconnected.

Many retirees quietly wonder:

“Am I withdrawing efficiently?”

“Could I lower taxes long term?”

“What happens if one of us dies?”

“Are we taking too much risk?”

“Could one mistake hurt us later?”

Those are reasonable questions.

A Simple Retirement Situation vs. A More Complex One

Example #1: Simpler Retirement Scenario

A retiree may have:

Pension income

Social Security

Small IRA balances

Minimal taxes

Stable spending needs

This household may require relatively little ongoing planning complexity.

Example #2: More Complex Retirement Scenario

A married couple has:

$2 million invested

Large IRAs

Brokerage accounts

Deferred compensation

Rental property

Delayed Social Security decisions

Roth conversion opportunities

Widow planning concerns

Now retirement planning involves:

Tax coordination

Withdrawal sequencing

Survivor planning

Medicare considerations

Estate organization

At this stage, the value of coordination may increase significantly.

What Good Financial Advisors Actually Help With

A good retirement-focused advisor should help coordinate:

Taxes

Retirement income

Investment allocation

Withdrawal strategy

Long-term planning

Estate coordination

Survivor preparation

The value is often not “beating the market.”

The value is reducing costly mistakes and improving long-term decision coordination.

Not All Advisors Provide the Same Value

This is important.

Retirees should understand that advisors vary significantly.

Some primarily focus on:

Investment products

Asset gathering

Insurance sales

Others focus on comprehensive retirement planning.

Important Questions to Ask

Before hiring someone, retirees should understand:

Are they acting as a fiduciary?

How are they compensated?

Do they provide tax-aware planning?

Do they coordinate retirement income strategy?

How do they communicate during market volatility?

Do they help with survivor planning?

Will both spouses understand the plan?

A good advisor relationship should create clarity, not confusion.

Common Mistakes Retirees Make When Hiring Advisors

1. Focusing Only on Investment Returns

Retirement planning is broader than portfolio performance alone.

2. Hiring Someone Without Understanding Fees

Transparency matters.

Retirees should clearly understand:

Advisory fees

Product commissions

Insurance incentives

Planning costs

3. Assuming All Advisors Coordinate Taxes

Many do not.

Tax planning often becomes one of the most valuable retirement planning areas.

4. Waiting Until a Crisis Happens

Some retirees delay planning until:

A spouse dies

Markets decline

RMDs begin

Taxes spike

Health changes occur

Planning is often easier before pressure builds.

Questions to Ask Yourself Before Hiring an Advisor

Consider questions like:

Is retirement planning becoming emotionally stressful?

Am I confident about withdrawal strategy?

Do I understand future tax exposure?

Would my spouse know what to do without me?

Am I coordinating Social Security properly?

Do I have a plan for market downturns?

Are estate documents and beneficiaries organized?

The answers may help clarify whether professional coordination could add value.

Final Thoughts

Many people successfully manage their finances during their working years.

But retirement planning often becomes more interconnected and more difficult to reverse once income, taxes, Social Security, healthcare, and withdrawals all begin interacting simultaneously.

At Greenbush Financial Group, we often find that retirees seek guidance not because they want to give up control, but because they want greater clarity and confidence as retirement decisions become more complex.

Hiring a financial advisor is not automatically necessary for everyone.

But for some retirees, especially those approaching major retirement decisions, thoughtful coordination may help reduce costly mistakes and improve long-term financial flexibility.

The goal is not dependency.

The goal is making informed decisions during one of the most financially important transitions of life.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

When should someone hire a financial advisor before retirement?Many people consider hiring an advisor within 5-10 years of retirement, especially when decisions around taxes, withdrawals, Social Security, and healthcare become more complex.

-

Do all retirees need a financial advisor?No. Some retirees with simple financial situations and strong financial knowledge may manage retirement successfully on their own.

-

What is the difference between investment management and retirement planning?Investment management focuses primarily on portfolios. Retirement planning coordinates income, taxes, withdrawals, Social Security, healthcare, estate planning, and long-term sustainability.

-

Why does retirement planning become more complicated?Because decisions become interconnected. Withdrawals, taxes, Social Security, Medicare premiums, and market performance can all affect one another.

-

What are signs retirement planning may be too complex to handle alone?Common signs include large IRA balances, uncertainty around withdrawals, tax concerns, widow planning issues, and anxiety about market volatility.

-

Should DIY investors feel pressured to hire an advisor?No. Many successful DIY investors continue managing their finances independently. The question is whether retirement complexity has reached a level where coordination may improve outcomes.

-

What should retirees look for in a financial advisor?Retirees should evaluate fiduciary responsibility, fee transparency, retirement income planning experience, tax coordination, communication style, and survivor planning expertise.

-

What is the biggest mistake retirees make before hiring an advisor?One of the biggest mistakes is assuming retirement planning is only about investments instead of coordinating taxes, income, healthcare, and long-term financial decisions together.

When One Social Security Check Disappears: What Retired Couples Need to Plan For

Many couples plan carefully for retirement together but overlook the financial realities of retirement alone. Learn how survivor Social Security benefits, taxes, healthcare costs, and estate planning can impact a surviving spouse.

Many married couples plan carefully for retirement together but spend very little time preparing for the financial realities of retirement alone. When one spouse dies, income may drop faster than expenses, taxes can increase, and important financial decisions suddenly fall on one person. Understanding survivor Social Security rules, tax changes, healthcare costs, and estate planning issues can help protect the surviving spouse financially and emotionally. At Greenbush Financial Group, we often find that the best survivor planning happens before a crisis occurs.

Most Couples Plan for Retirement Together—But Not for Retirement Alone

Many retired couples assume that if one spouse dies, household expenses simply get cut in half.

In reality, that rarely happens.

When one spouse passes away:

One Social Security check may disappear

Taxes may increase

Healthcare costs may remain high

Housing costs often stay similar

One person may suddenly manage all financial decisions alone

At the same time, the surviving spouse may also be dealing with grief, paperwork, legal decisions, and emotional stress.

This is why survivor planning is one of the most important and overlooked parts of retirement planning.

The goal is not to think pessimistically.

The goal is making sure either spouse could continue forward financially with clarity and confidence.

What Financially Changes When One Spouse Dies?

Several important financial changes can happen almost immediately after a spouse passes away.

Social Security Income Often Drops

This is one of the biggest surprises for many couples.

When both spouses are receiving Social Security, one benefit usually disappears after the first death.

The surviving spouse generally keeps:

Their own benefit

Or the higher of the two benefits

But not both full checks.

Example

John receives:

$3,200/month from Social Security

Susan receives:

$2,100/month

Combined household income:

$5,300/month

After John dies, Susan may keep the larger $3,200 benefit, but the smaller benefit disappears.

Household Social Security income drops by:

$2,100/month

Or more than $25,000 annually

Meanwhile, many expenses continue.

Expenses Often Do NOT Drop by 50%

This is one of the most important retirement realities couples should understand.

Certain expenses may decrease modestly:

Food

Travel

Clothing

Some healthcare expenses

But many major costs remain similar:

Property taxes

Utilities

Insurance

Home maintenance

Car expenses

Healthcare premiums

In many cases, household expenses may only decline by 20%–30% while income drops significantly more.

That gap can create financial pressure for surviving spouses.

Why Surviving Spouses Often Pay Higher Taxes

This surprises many retirees.

After one spouse dies, the surviving spouse usually transitions from:

Married Filing Jointly

to:Single tax filing status

That change can happen quickly.

The problem is that single tax brackets are less favorable at lower income levels.

This means surviving spouses may pay higher taxes even if household income decreases.

The Survivor Tax Trap

A surviving spouse may face:

Similar IRA balances

Similar investment income

Similar Required Minimum Distributions (RMDs)

But now with:

Less favorable tax brackets

One standard deduction instead of two

Potentially higher Medicare premiums

Example

A married couple may comfortably remain in the 22% bracket while filing jointly.

After one spouse dies, the survivor could move into higher effective tax exposure as a single filer with nearly the same retirement account balances.

This is one reason Roth conversion planning during joint lifetimes can become extremely valuable.

Why Roth Conversions Can Matter More Than Couples Realize

Many couples focus only on their current taxes.

But survivor planning often changes the equation.

Converting portions of traditional IRAs to Roth IRAs while both spouses are alive may help:

Reduce future RMDs

Lower future survivor tax exposure

Create tax-free withdrawal flexibility

Improve long-term tax diversification

Example

A retired couple in their mid-60s delays Social Security and intentionally converts moderate IRA amounts annually while remaining within a manageable tax bracket.

Years later, if one spouse dies, the surviving spouse may have:

Smaller RMDs

More Roth flexibility

Lower taxable income

Better control over Medicare premium exposure

The key is evaluating these opportunities before tax brackets potentially tighten later.

Pension Survivor Decisions Matter More Than Many Couples Realize

Some pensions offer choices such as:

Single-life payout

Joint-and-survivor payout

Reduced survivor benefits

Many retirees choose larger monthly income initially without fully understanding how survivor income changes later.

Important Question

If one spouse dies:

Will pension income continue?

Reduce?

Or disappear entirely?

These decisions are often permanent once retirement begins.

Healthcare and Long-Term Care Planning Become More Important

Healthcare planning can become more difficult for surviving spouses because:

One spouse may eventually need care alone

Adult children may live far away

Financial management responsibilities may suddenly shift

Couples should discuss:

Long-term care preferences

Healthcare directives

Emergency contacts

Account access

Caregiving expectations

These conversations are uncomfortable for many families, but avoiding them often creates more stress later.

One of the Biggest Risks: Only One Spouse Understands the Finances

In many households, one spouse handles:

Investments

Taxes

Bills

Insurance

Account logins

Estate planning

That may work fine until something unexpected happens.

Then the surviving spouse may suddenly feel overwhelmed managing decisions they were never involved in previously.

Important Step

Both spouses should understand:

Where accounts are located

How income is generated

Who to contact for help

How bills are paid

What the retirement income plan looks like

Financial organization itself can become a form of protection.

Beneficiary Mistakes Can Create Major Problems

Many retirement accounts pass through beneficiary designations rather than wills.

Outdated beneficiaries can create unintended outcomes.

Common issues include:

Ex-spouses still listed

Missing contingent beneficiaries

Unequal inheritance structures

Children added improperly to accounts

Retirement transitions are a good time to review:

IRA beneficiaries

Roth IRA beneficiaries

Life insurance

Transfer-on-death accounts

Trust coordination

A Real-World Survivor Planning Example

David and Karen retire at age 66.

They have:

$1.5 million invested

Two Social Security benefits totaling $5,800/month

Moderate IRA balances

A paid-off home

Initially, they focus mostly on investment growth and travel spending.

But after reviewing survivor planning, they realize several risks:

One Social Security check would disappear

Karen would likely face higher taxes as a single filer

Future RMDs could become problematic

Karen was unfamiliar with many financial accounts

They decide to:

Complete partial Roth conversions annually

Organize account records and passwords

Review estate documents

Stress-test survivor income needs

Ensure both spouses understand the retirement plan

None of these changes were dramatic.

But together, they significantly improved financial clarity and flexibility for the surviving spouse.

Questions Every Retired Couple Should Ask

If one spouse died tomorrow:

Would the surviving spouse know where everything is?

Would income still cover expenses?

Which Social Security benefit would remain?

Would taxes increase?

Would healthcare costs still be manageable?

Are beneficiaries updated?

Are estate documents current?

Does each spouse understand the financial plan?

These are difficult questions.

But they are often easier to address proactively than during a crisis.

Common Survivor Planning Mistakes

1. Ignoring Survivor Income Changes

Many couples underestimate how much income could disappear after the first death.

2. Delaying Estate Organization

Missing documents and unclear account structures create unnecessary stress.

3. Claiming Social Security Without Survivor Planning

Social Security timing decisions can significantly affect long-term survivor income.

4. Ignoring Future Survivor Tax Rates

Surviving spouses often face higher taxes with less favorable filing brackets.

5. Letting One Spouse Handle Everything Alone

Retirement planning works best when both spouses understand the overall strategy.

What Good Survivor Planning Really Looks Like

Good survivor planning is not about predicting the future perfectly.

It is about creating flexibility and reducing unnecessary uncertainty.

That may include:

Reviewing Social Security timing

Evaluating Roth conversions

Stress-testing survivor income

Organizing estate documents

Updating beneficiaries

Maintaining adequate liquidity

Ensuring both spouses understand the plan

The goal is not fear.

The goal is preparedness.

Final Thoughts

Most married couples spend years planning for retirement together.

Far fewer spend time planning for the financial realities one spouse may eventually face alone.

At Greenbush Financial Group, we often find that the strongest retirement plans are not just designed for ideal scenarios. They are also built to protect the surviving spouse from unnecessary financial stress, tax surprises, and confusion during difficult transitions.

These conversations are not always easy.

But they are some of the most valuable retirement planning discussions couples can have.

Good retirement planning is not just about helping both spouses retire comfortably.

It is about helping either spouse continue confidently if life changes unexpectedly.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

What happens to Social Security when one spouse dies?The surviving spouse generally keeps the larger of the two Social Security benefits, while the smaller benefit stops.

-

Do taxes increase for surviving spouses?Often, yes. Surviving spouses usually transition from married filing jointly to single filing status, which can create higher tax exposure at lower income levels.

-

Do household expenses get cut in half after one spouse dies?Usually not. Many fixed expenses remain similar even though household income may decline significantly.

-

Why are Roth conversions important for married retirees?Roth conversions during joint lifetimes may help reduce future taxes, lower survivor RMDs, and improve tax flexibility for the surviving spouse.

-

Should both spouses understand the retirement plan?Absolutely. Both spouses should know where accounts are held, how income is generated, and who to contact for financial guidance.

-

What estate planning documents should retirees review?Retirees should review wills, trusts, powers of attorney, healthcare directives, and beneficiary designations regularly.

-

Can Medicare premiums increase for surviving spouses?Yes. Higher taxable income combined with single filing status may increase Medicare IRMAA exposure.

-

What is the biggest survivor planning mistake couples make?One of the biggest mistakes is assuming the surviving spouse will automatically be financially secure without reviewing income reductions, taxes, and account organization ahead of time.

The Inflation Problem Conservative Retirees Often Underestimate

Many retirees prioritize safety after leaving work, but being too conservative can create risks of its own. Learn how inflation, longevity, and portfolio growth affect long-term retirement income.

Many retirees become more conservative after leaving work, and that instinct is understandable. But avoiding too much market risk can create other risks that are easier to overlook, including inflation erosion, reduced long-term income growth, and the possibility of running out of money later in retirement. A retirement portfolio should not only protect against market declines but also support spending needs over decades. At Greenbush Financial Group, we often help retirees balance safety, growth, and income without taking unnecessary risk.

Many Retirees Focus on One Risk While Overlooking Another

Most retirees worry about losing money in the market.

That concern is completely reasonable.

Once paychecks stop, market declines often feel more emotional because withdrawals may now be coming directly from investment accounts.

As a result, many retirees react by moving heavily into:

Cash

CDs

Savings accounts

Short-term bonds

Extremely conservative portfolios

At first, this can feel safer.

Balances may fluctuate less. Monthly statements may feel calmer. Market headlines may feel less threatening.

But there is another risk retirees sometimes underestimate:

The risk of becoming too conservative for too long.

Because retirement is not usually a 5-year plan.

For many households, retirement may need to last:

20 years

30 years

Or longer

And over long periods of time, inflation can quietly become one of the biggest financial pressures retirees face.

The Hidden Risk: Losing Purchasing Power Over Time

One of the biggest challenges in retirement is that expenses rarely stay flat forever.

Even moderate inflation can slowly increase the cost of:

Healthcare

Insurance

Property taxes

Utilities

Food

Travel

Long-term care

Example

Suppose a retiree needs:

$80,000 per year today

If inflation averages 3% annually, that same lifestyle could require roughly:

$145,000 annually in 20 years

That does not mean spending suddenly doubles overnight.

It means purchasing power slowly erodes over time.

And portfolios that are too conservative may struggle to keep pace.

Why Too Much Cash Can Become a Retirement Problem

Cash plays an important role in retirement.

But many retirees unintentionally turn short-term safety into a long-term strategy.

That can create problems.

The Challenge With Excess Cash

Cash and low-yield investments may provide stability, but they often generate returns that struggle to outpace inflation over longer periods.

Over time, retirees may face:

Reduced purchasing power

Greater withdrawal pressure

Lower portfolio growth

Increased longevity risk

This becomes especially important later in retirement when:

Healthcare costs rise

Inflation compounds

One spouse may eventually live alone

Required withdrawals increase

The Difference Between Volatility Risk and Purchasing-Power Risk

Most retirees understand volatility risk.

That is the risk of market declines.

But retirement planning also involves purchasing-power risk.

That is the risk that your money loses real spending power over time because growth fails to keep up with inflation.

Both Risks Matter

An overly aggressive portfolio can create uncomfortable volatility.

But an overly conservative portfolio may quietly lose ground for years.

Retirement planning is often about balancing these risks rather than eliminating one entirely.

Why Retirees Still Need Some Growth

One of the biggest retirement misconceptions is:

“Once I retire, I should stop investing for growth.”

In reality, many retirees still need a portion of their portfolio invested for long-term growth because retirement may last decades.

Growth investments may help:

Offset inflation

Support future withdrawals

Reduce longevity risk

Maintain purchasing power

Improve portfolio sustainability

This does not mean retirees should become aggressive investors.

It means retirement portfolios usually need balance.

A Real-World Example: Conservative vs Balanced Retirement Strategies

Let’s compare two retirees.

Both retire at age 65 with:

$1.5 million invested

Spending needs of $75,000 annually

No pension

Moderate Social Security income

Retiree #1: Extremely Conservative

This retiree keeps:

80% in cash and CDs

20% in short-term bonds

The portfolio experiences very little volatility.

But over time:

Inflation reduces purchasing power

Withdrawals slowly increase

Portfolio growth struggles to keep pace

Future flexibility declines

Initially, this strategy feels emotionally comfortable.

But the long-term pressure builds quietly.

Retiree #2: Balanced Retirement Allocation

This retiree keeps:

Cash reserves for near-term spending

Bonds for stability

A diversified stock allocation for long-term growth

The portfolio experiences more short-term fluctuations.

But it also maintains greater long-term growth potential to help offset:

Inflation

Rising healthcare costs

Longer retirement timelines

The goal is not maximizing returns.

The goal is balancing stability and sustainability.

Why Fear Often Drives Overly Conservative Decisions

Many retirees become more conservative after:

Major market declines

Retirement timing stress

Watching account balances fluctuate

Financial news headlines

Economic uncertainty

These reactions are understandable.

Retirement changes how risk feels emotionally.

But investment decisions driven entirely by fear can sometimes create new risks that are less obvious initially.

Important Note

The answer is not ignoring risk.

The answer is understanding that retirement includes multiple risks:

Market risk

Inflation risk

Longevity risk

Tax risk

Healthcare cost risk

Strong retirement planning considers all of them together.

Sequence Risk Still Matters

Some retirees hear that they should maintain growth investments and assume they should remain heavily invested aggressively.

That can also create problems.

This is where sequence-of-returns risk becomes important.

What Is Sequence Risk?

Sequence risk occurs when poor market returns happen early in retirement while withdrawals are occurring simultaneously.

This can permanently damage long-term portfolio sustainability.

That is why retirement portfolios should balance:

Growth potential

Stability

Cash reserves

Withdrawal flexibility

Not simply maximize stock exposure.

The Role of Cash Reserves in a Balanced Retirement Plan

Cash is still important.

The issue is not holding cash.

The issue is relying too heavily on cash for too long.

Many retirees benefit from maintaining:

12–24 months of planned withdrawals in cash or short-term reserves

This may help cover spending needs during market declines without forcing investment sales at poor times.

Key Insight

Cash works best as a stability tool, not a complete long-term retirement strategy.

What About CDs and Bonds?

CDs and bonds can absolutely play an important role in retirement income planning.

But relying exclusively on conservative fixed-income investments can become more difficult when:

Inflation rises

Interest rates change

Spending needs increase

Retirement lasts longer than expected

The challenge is that many retirees need portfolios to do two things simultaneously:

Provide stability

Maintain long-term purchasing power

That often requires diversification across multiple asset types.

How Conservative Portfolios Can Increase Withdrawal Pressure

This is one of the least understood retirement risks.

If portfolio growth remains too low for too long:

Withdrawals may consume a larger percentage of assets

Future income flexibility may shrink

Spending adjustments may become necessary later

Ironically, some retirees become more conservative specifically because they fear running out of money.

But insufficient growth can sometimes increase that risk over longer periods.

The Goal Is Not Aggressive Investing

This is important.

A balanced retirement strategy should not feel like speculation.

The goal is not chasing returns.

The goal is building a portfolio designed for:

Reliable income

Long-term sustainability

Inflation protection

Emotional comfort

Flexibility during downturns

The right allocation depends on factors such as:

Age

Spending needs

Guaranteed income

Health

Risk tolerance

Legacy goals

Withdrawal rates

There is no universal retirement portfolio.

Questions Retirees Should Ask

Important retirement planning questions include:

How much cash is appropriate for my situation?

Could inflation pressure my spending later?

Am I too conservative for a 25–30 year retirement?

What happens if healthcare costs rise significantly?

How would my spouse manage if I died first?

Is my withdrawal strategy sustainable?

Do I have enough growth potential built into the plan?

These questions are often more valuable than trying to predict short-term market movements.

Common Mistakes Conservative Retirees Make

1. Moving Entirely to Cash After Retirement

This may feel safer emotionally but can increase long-term purchasing-power risk.

2. Ignoring Inflation

Even moderate inflation compounds significantly over decades.

3. Assuming Conservative Means “Risk-Free”

Every retirement strategy involves tradeoffs.

Low volatility does not eliminate long-term retirement risk.

4. Separating Safety and Growth Incorrectly

Many retirees benefit from separating:

Short-term spending reserves from:

Long-term growth assets

This creates flexibility during volatility.

5. Reacting Emotionally After Market Declines

Emotional investment decisions can permanently alter long-term retirement outcomes.

Final Thoughts

Wanting safety in retirement is completely understandable.

Most retirees are not trying to maximize returns. They are trying to protect the life they worked decades to build.

But retirement planning is not just about avoiding market declines.

It is also about protecting future purchasing power, maintaining flexibility, and creating income that can last through decades of changing expenses and inflation.

At Greenbush Financial Group, we often help retirees balance multiple retirement risks at once rather than focusing on only one type of fear or uncertainty.

The goal is not taking unnecessary risk.

The goal is making sure your retirement plan protects you from both short-term volatility and long-term erosion.

Rob Mangold

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

FAQ

-

Can being too conservative in retirement be risky?Yes. Holding too much cash or low-growth investments for long periods may increase inflation risk and reduce long-term purchasing power.

-

Why do retirees still need growth investments?Many retirements last 20-30 years or longer. Growth investments may help offset inflation and support long-term income sustainability.

-

How much cash should retirees keep?Many retirees benefit from holding 12-24 months of planned withdrawals in cash or short-term reserves, depending on risk tolerance and spending needs.

-

Is cash bad in retirement?No. Cash plays an important role for stability and near-term spending. Problems usually arise when retirees rely too heavily on cash long-term.

-

What is purchasing-power risk?Purchasing-power risk is the risk that inflation gradually reduces the real value of your money over time.

-

What is sequence-of-returns risk?Sequence risk occurs when poor market returns happen early in retirement while withdrawals are occurring simultaneously.

-

Should retirees avoid the stock market completely?Not necessarily. Many retirees benefit from maintaining some diversified growth exposure while balancing stability and income needs.

-

What is the biggest mistake overly conservative retirees make?One of the biggest mistakes is focusing only on avoiding short-term market volatility while underestimating long-term inflation and longevity risks.

Should You Retire at 62, 65, or 67? The Tradeoffs Most People Overlook

Should you retire at 62, 65, or 67? The answer involves much more than Social Security. Learn how healthcare costs, taxes, Roth conversions, and portfolio withdrawals can influence the best retirement age for your situation.

Deciding whether to retire at 62, 65, or 67 involves much more than simply choosing when to claim Social Security. Your retirement age can impact healthcare costs, taxes, portfolio withdrawals, Roth conversion opportunities, and long-term financial security. In this article, Greenbush Financial Group breaks down the real tradeoffs retirees should consider, including situations where retiring earlier may make sense and when waiting could provide better long-term outcomes.

Should You Retire at 62, 65, or 67? The Tradeoffs Most People Overlook

For many Americans, retirement planning often centers around one question:

“When should I retire?”

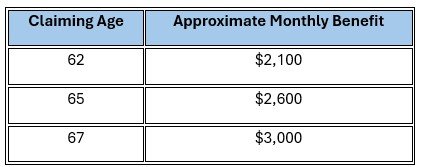

The most common ages people consider are 62, 65, and 67 because each one connects to major financial milestones:

Age 62: Earliest Social Security eligibility

Age 65: Medicare eligibility

Age 67: Full Retirement Age (FRA) for many retirees

But the reality is that retirement timing is rarely just about Social Security.

The age you stop working can affect:

Your healthcare costs

Your tax strategy

Your withdrawal rate

Your investment risk

Your long-term retirement security

Your emotional well-being

And despite what many headlines suggest, there is no universally “perfect” retirement age.

At Greenbush Financial Group, we often find that the best retirement age depends less on rules and more on how all the moving pieces fit together for a household.

The Real Difference in Social Security at 62 vs. 65 vs. 67

One of the biggest factors in retirement timing is Social Security income.

Here’s a simplified example using someone whose Full Retirement Age benefit at 67 is $3,000 per month.

That difference can become substantial over a 25- to 30-year retirement.

For a married couple, coordinated claiming decisions may impact lifetime income by hundreds of thousands of dollars.

However, larger Social Security checks do not automatically mean delaying retirement is always better.

The bigger question is:

What are you giving up by waiting?

The Tradeoff Most People Miss

Many retirement articles focus only on maximizing Social Security benefits.

But retiring later can also mean:

Fewer healthy retirement years

Higher stress or burnout

Less flexibility with family

Missing Roth conversion opportunities

Paying more taxes later

Delaying goals you care about

Meanwhile, retiring earlier may increase:

Portfolio withdrawal pressure

Healthcare costs before Medicare

Sequence of returns risk

Longevity concerns

The goal is not simply maximizing one variable.

The goal is building a retirement plan that balances income, taxes, lifestyle, healthcare, and risk.

How Retiring Early Impacts Medicare and Healthcare Costs

One of the largest financial gaps in early retirement is health insurance before Medicare begins at 65.

If you retire at 62, you may need to bridge three years of healthcare costs before Medicare eligibility.

Depending on your income and coverage needs, that could mean:

ACA marketplace plans

COBRA coverage

Private insurance

Spousal employer coverage

For many couples, healthcare premiums and out-of-pocket costs can easily exceed:

$15,000 to $30,000+ annually before age 65

That expense is often underestimated.

Example: Retiring at 62 Before Medicare

A couple retires at 62 with:

$1.2 million invested

No pension

$70,000 annual spending goal

Because Social Security has not started yet, they may need to withdraw:

$70,000+ annually from investments

Plus healthcare costs

Plus taxes

If markets decline early in retirement, those larger withdrawals can create pressure on the portfolio much sooner than expected.

The Sequence of Returns Risk Most Retirees Ignore

One of the biggest risks in early retirement is something called sequence of returns risk.

This means poor market returns early in retirement can damage a portfolio more severely when withdrawals are happening simultaneously.

For example:

A major market decline at age 63 may hurt far more than the same decline at age 78.

Early losses combined with withdrawals can permanently reduce future recovery potential.

This becomes especially important for retirees stopping work before Social Security and Medicare begin.

Example

Two retirees both average 6% annual returns over retirement.

But:

Retiree A experiences strong returns early

Retiree B experiences a bear market immediately after retiring

Even with identical average returns, Retiree B may run out of money significantly sooner because withdrawals occurred during market declines.

This is why retirement timing and market conditions should be evaluated together.

Break-Even Analysis: How Long Do You Need to Live for Waiting to Pay Off?

One of the most common questions retirees ask is:

“How long do I need to live for delaying Social Security to make sense?”

A simplified break-even analysis often shows:

Delaying from 62 to 67 may break even somewhere in the late 70s or early 80s

But this analysis is incomplete unless you also consider:

Taxes

Investment withdrawals

Survivor benefits

Healthcare costs

Portfolio growth