Secure Act 2.0: RMD Start Age Pushed Back to 73 Starting in 2023

On December 23, 2022, Congress passed the Secure Act 2.0, which moved the required minimum distribution (RMD) age from the current age of 72 out to age 73 starting in 2023. They also went one step further and included in the new law bill an automatic increase in the RMD beginning in 2033, extending the RMD start age to 75.

On December 23, 2022, Congress passed the Secure Act 2.0, which moved the required minimum distribution (RMD) age from the current age of 72 out to age 73 starting in 2023. They also went one step further and included in the new law bill an automatic increase in the RMD beginning in 2033, extending the RMD start age to 75.

This is the second time within the past 3 years that Congress has changed the start date for required minimum distributions from IRAs and employer-sponsored retirement plans. Here is the history and the future timeline of the RMD start dates:

1986 – 2019: Age 70½

2020 – 2022: Age 72

2023 – 2032: Age 73

2033+: Age 75

You can also determine your RMD start age based on your birth year:

1950 or Earlier: RMD starts at age 72

1951 – 1959: RMD starts at age 73

1960 or later: RMD starts at age 75

What Is An RMD?

An RMD is a required minimum distribution. Once you hit a certain age, the IRS requires you to start taking a distribution each year from your various retirement accounts (IRA, 401(K), 403(b), Simple IRA, etc.) because they want you to begin paying tax on a portion of your tax-deferred assets whether you need them or not.

What If You Turned Age 72 In 2022?

If you turned age 72 anytime in 2022, the new Secure Act 2.0 does not change the fact that you would have been required to take an RMD for 2022. This is true even if you decided to delay your first RMD until April 1, 2023, for the 2022 tax year.

If you are turning 72 in 2023, under the old rules, you would have been required to take an RMD for 2023; under the new rules, you will not have to take your first RMD until 2024, when you turn age 73.

Planning Opportunities

By pushing the RMD start date from age 72 out to 73, and eventually to 75 in 2033, it creates more tax planning opportunities for individuals that do need to take distributions out of their IRAs to supplement this income. Since these distributions from your retirement account represent taxable income, by delaying that mandatory income could allow individuals the opportunity to process larger Roth conversions during the retirement years, which can be an excellent tax and wealth-building strategy.

Delaying your RMD can also provide you with the following benefits:

Reduce the amount of your Medicare premiums

Reduce the percentage of your social security benefit that is taxed

Make you eligible for tax credits or deductions that you would have phased out of

Potentially allow you to realize a 0% tax rate on long-term capital gains

Continue to keep your pre-tax retirement dollars invested and growing

Additional Secure Act 2.0 Articles

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is the new RMD age under the Secure Act 2.0?

Starting in 2023, the required minimum distribution (RMD) age increased from 72 to 73. Beginning in 2033, the RMD age will rise again to 75.

How does the new RMD timeline compare to previous rules?

Before 2020, RMDs began at age 70½. The Secure Act of 2019 moved it to age 72, and Secure Act 2.0 now increases it to age 73 in 2023 and age 75 starting in 2033.

How do you determine your RMD start age based on birth year?

If you were born in 1950 or earlier, your RMD started at 72. Those born between 1951 and 1959 begin at 73, and anyone born in 1960 or later will start at 75.

What if I turned 72 in 2022?

If you reached age 72 in 2022, you are still required to take your first RMD for that tax year, even if you delayed it until April 1, 2023. The new rule applies only to individuals turning 72 in 2023 or later.

What are the benefits of delaying RMDs?

Delaying RMDs can create valuable tax planning opportunities, including the ability to complete larger Roth conversions, reduce taxable income, lower Medicare premiums, and minimize taxes on Social Security benefits.

Can delaying RMDs impact long-term investment growth?

Yes. By postponing mandatory withdrawals, your tax-deferred savings can remain invested and continue to grow, potentially increasing your retirement assets over time.

Removing Excess Contributions From A Roth IRA

If you made the mistake of contributing too much to your Roth IRA, you have to go through the process of pulling the excess contributions back out of the Roth IRA. The could be IRS taxes and penalties involved but it’s important to understand your options.

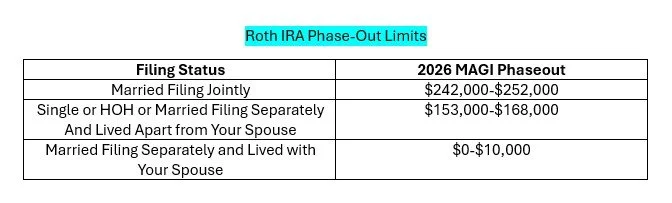

You discovered that you contributed too much to your Roth IRA, now it’s time to fix it. This most commonly happens when individuals make more than they expected which causes them to phaseout of their ability to make a contribution to their Roth IRA for a particular tax year. In 2026, the phase out ranges for Roth IRA contributions are:

· Single Filer: $153,000 - $167,999

· Married Filing Joint: $242,000 - $251,999

The good news is there are a few options available to you to fix the problem but it’s important to act quickly because as time passes, certain options for removing those excess IRA contributions will be eliminated.

You Discover The Error Before You File Your Taxes

If you discover the contribution error prior to filing your tax return, the most common fix is to withdraw the excess contribution amount plus EARNINGS by your tax filing deadline, April 18th. Custodians typically have a special form for removing excess contributions from your Roth IRA that you will need to complete.

If you withdraw the excess contribution before the tax deadline, you will avoid having to pay the IRS 6% excise penalty on the contribution, but you will still have to pay income tax on the earnings generated by the excess contribution. In addition, if you are under the age of 59½, you will also have to pay the 10% early withdrawal penalty on just the earnings portion of the excess contribution.

Example, you contribute $6,000 to your Roth IRA in September 2025 but you find out in March 2026 that your income level only allows you to make a $2,000 contribution to your Roth IRA for 2025 so you have a $4,000 excess contribution. You will have to withdraw not just the $4,000 but also the earnings produced by the $4,000 while it was in the account, for purposes of this example let’s assume that’s $400. The $4,000 is returned to you tax and penalty free but when the $400 in earnings is distributed from the account, you will have to pay tax on the earnings, and if under age 59½, a 10% withdrawal penalty on the $400.

October 15th Deadline

If you have already filed your taxes and you discover that you have an excess contribution to a Roth IRA, but it’s still before October 15th, you can avoid having to pay the 6% penalty by filing an amended tax return. You still have pay taxes and possibly the 10% early withdrawal penalty on the earnings but you avoid the 6% penalty on the excess contribution amount. This is only available until October 15th following the tax year that the excess contribution was made.

You Discover The Mistake After The October 15th Extension Deadline

If you already filed your taxes and you did not file an amended tax return by October 15th, the IRS 6% excess contribution penalty applies. If you contributed $6,000 to Roth IRA but your income precluded you from contributing anything to a Roth IRA in that tax year, it would result in a $360 (6%) penalty. But it’s important to understand that this is not a one-time 6% penalty but rather a 6% PER YEAR penalty on the excess amount UNTIL the excess amount is withdrawn from the Roth IRA. If you discovered that 5 years ago you made a $5,000 excess contribution to your Roth IRA but you never removed the excess contributions, it would result in a $1,500 penalty.

6% x 5 Years = 30% Total Penalty x $5,000 Excess Contribution = $1,500 IRS Penalty

A 6% Penalty But No Earnings Refund

Here’s a little known fact about the IRS excess contribution rules, if you are subject to the 6% penalty because you did not withdraw the excess contributions out of your Roth IRA prior to the tax deadline, when you go to remove the excess contribution, you are no longer required to remove the earnings generated by the excess contribution.

Reminder: If you remove the excess contribution prior to the initial tax deadline, you AVOID the 6% penalty on the excess contribution amount but you have to pay taxes and possibly the 10% early withdrawal penalty on just the earnings portion of the excess contribution.

If you remove the excess contribution AFTER the tax deadline, you do not have to pay taxes or penalties on the EARNINGS portion because you are not required to distribute the earnings, but you pay a flat 6% penalty per year based on the actual excess contribution amount.

Example: You contributed $6,000 to your Roth IRA in 2025, your income ended up being too high to allow any Roth IRA contributions in 2025, you discover this error in November 2026. You will have to withdraw the $6,000 excess contribution, pay the 6% penalty of $360, but you do not have to distribute any of the earnings associated with the excess contribution.

Why does it work this way? This is only a guess but since most taxpayers probably try to remove the excess contributions as soon as possible, maybe the 6% IRS penalty represents an assumed wipeout of a modest rate of return generated by those excess contributions while they were in the IRA.

Advanced Tax Strategy

There is an advanced tax strategy that involves evaluating the difference between the flat 6% penalty on the excess contribution amount and paying tax and possibly the 10% penalty on the earnings. Before I explain the strategy, I strongly advise that you consult with your tax advisor before executing this strategy.

I’ll show you how this works in an example. You make a $6,000 contribution to your Roth IRA in 2025 but then find out in March 2026 that based on your income, you are not allowed to make a Roth contribution for 2025. Your Roth IRA experienced a 50% investment return between the time you made the $6,000 contribution and now. You are 35 years old. So now you have a choice:

Option A: Prior to your 2025 tax filing, withdraw the $6,000 tax and penalty free, and also withdraw the $3,000 in earnings which will be subject to ordinary income tax and a 10% penalty. Assuming you are in a 32% Fed bracket, 6% State Bracket, that would cost you 48% in taxes and penalties on the $3,000 in earnings.

Total Taxes and Penalties = $1,440

Option B: Waiting until November 2026, pull out the $6,000 excess contribution, and pay the 6% penalty, but you get to leave the $3,000 in earnings in your Roth IRA. $6,000 x 6% = $360

Total Taxes and Penalties = $360

PLUS you have an additional $3,000 that gets to stay in your Roth IRA, compound returns, and then be withdrawn tax and penalty free after age 59½.

FINANCIAL NERD NOTE: If the only balance in your Roth IRA is from earnings that originated from excess contributions, it’s does not start the 5-year holding period required to receive the Roth IRA earnings tax free after age 59½ because they are considered ineligible contributions retained within the Roth IRA.

Losses Within The Roth IRA

Since I’m writing this in March 2026 and most of the equity indexes are down year-to-date, I’ll explain how losses within a Roth IRA impact the excess contribution calculation. If your Roth IRA has lost value between the time you made the excess contribution and the withdrawal date, it does reduce the amount that you have to withdraw from the IRA. If your excess contribution amount is $3,000 but the Roth IRA dropped 20% in value, you would only have to withdraw $2,400 from the Roth IRA to satisfy the removal of the excess contributions. If withdrawn prior to your tax filing deadline, no taxes or penalties would be due because there were no earnings.

Other Options Besides Cash Withdrawals

Up until now we have just talked about withdrawing the excess contribution from your IRA by taking the cash back but there are a few other options that are available to satisfy the excess contribution rules.

The first is “recharacterizing” your excess Roth contribution as a traditional IRA contribution. If your income allows, you may be able to transfer the excess Roth contribution amount and earnings from your Roth IRA to your Traditional IRA but this must be done in the same tax year to avoid the 6% penalty.

Second option, if you are eligible to make a Roth IRA contribution the following year, the excess contribution can be used to offset the Roth contribution amount for the following tax year. Example, if you had an excess Roth IRA contribution of $1,000 in 2025 and your income will allow you to make a $6,000 Roth IRA contribution in 2026, you can reduce the Roth contribution limit by $1,000 in 2026, leave the excess in the account, and just deposit the remaining $5,000. You would still have to pay the 6% penalty on the $1,000 because you never withdrew it from the Roth IRA but it’s $60 penalty versus having to take the time to go through the excess withdrawal process.

Which Contributions Get Pulled Out First

It’s not uncommon for investors to make monthly contributions to their Roth IRA accounts but when it comes to an excess contribution scenario, you don’t get to choose which contributions are entered into the earning calculation. The IRS follows the LIFO (last-in-first-out) method for determining which contributions should be removed to satisfy the excess refund.

You Have Multiple IRA’s

If you have multiple Roth IRA’s and there is an excess contribution, you have to remove the excess contribution from the same Roth IRA that the contribution was made to, you can’t take it from a different Roth IRA to satisfy the removal of the excess.

If you have both a Traditional IRA and a Roth IRA and you exceed the aggregate contribution limit for the year, by default, the IRS assumes the excess contribution was made to the Roth IRA, so you have to begin taking corrective withdrawals from your Roth IRA first.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What happens if I contribute too much to my Roth IRA?

If your income is too high or you accidentally contribute more than the annual Roth IRA limit, the excess amount is considered an “excess contribution.” The IRS assesses a 6% penalty each year that the excess remains in the account until it’s corrected.

How can I fix a Roth IRA excess contribution before filing my taxes?

If you catch the mistake before your tax filing deadline (typically April 15), you can withdraw the excess contribution and any earnings. You’ll avoid the 6% penalty, but the earnings portion is taxable—and may be subject to a 10% early withdrawal penalty if you’re under age 59½.

What if I already filed my tax return but it’s before October 15?

You can file an amended return and withdraw the excess contribution plus earnings before October 15 to avoid the 6% excise tax. However, you’ll still owe income taxes and possibly the 10% early withdrawal penalty on the earnings portion.

What happens if I discover the excess contribution after October 15?

Once the October 15 deadline passes, you can no longer avoid the 6% annual penalty. The penalty continues each year until the excess amount is removed from your Roth IRA, but you no longer have to withdraw the earnings associated with that excess contribution.

Can I recharacterize or apply the excess contribution to a future year?

Yes. You can recharacterize the excess Roth contribution as a traditional IRA contribution, if eligible, by transferring it and any earnings. Alternatively, you can apply the excess toward next year’s contribution limit, but you’ll owe a 6% penalty for the current year.

What if my Roth IRA lost money after I made the excess contribution?

If the value of your Roth IRA declines, you only need to withdraw the reduced value of the excess contribution. For example, if your $3,000 excess contribution dropped 20% in value, you would only withdraw $2,400, and no taxes or penalties would apply if withdrawn before the filing deadline.

How does the IRS determine which contributions to remove?

The IRS uses a last-in, first-out (LIFO) method, meaning the most recent contributions are treated as the ones being withdrawn first. Excess withdrawals must come from the same Roth IRA where the contribution was made.

Last updated June, 2026

Can You Contribute To An IRA & 401(k) In The Same Year?

There are income limits that can prevent you from taking a tax deduction for contributions to a Traditional IRA if you or your spouse are covered by a 401(k) but even if you can’t deduct the contribution to the IRA, there are tax strategies that you should consider

The answer to this question depends on the following items:

Do you want to contribute to a Roth IRA or Traditional IRA?

What is your income level?

Will the contribution qualify for a tax deduction?

Are you currently eligible to participate in a 401(k) plan?

Is your spouse covered by a 401(k) plan?

If you have the choice, should you contribute to the 401(k) or IRA?

Advanced tax strategy: Maxing out both and spousal IRA contributions

Traditional IRA

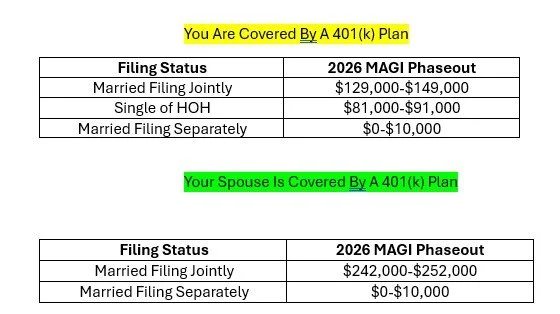

Traditional IRA’s are known for their pre-tax benefits. For those that qualify, when you make contributions to the account you receive a tax deduction, the balance accumulates tax deferred, and then you pay tax on the withdrawals in retirement. The IRA contribution limits for 2025 are:

Under Age 50: $7,500

Age 50+: $8,600

However, if you or your spouse are covered by an employer sponsored plan, depending on your level of income, you may or may not be able to take a deduction for the contributions to the Traditional IRA. Here are the phaseout thresholds for 2025:

Note: If both you and your spouse are covered by a 401(k) plan, then use the “You Are Covered” thresholds above.

BELOW THE BOTTOM THRESHOLD: If you are below the thresholds listed above, you will be eligible to fully deduct your Traditional IRA contribution

WITHIN THE PHASEOUT RANGE: If you are within the phaseout range, only a portion of your Traditional IRA contribution will be deductible

ABOVE THE TOP THRESHOLD: If your MAGI (modified adjusted gross income) is above the top of the phaseout threshold, you would not be eligible to take a deduction for your contribution to the Traditional IRA

After-Tax Traditional IRA

If you find that your income prevents you from taking a deduction for all or a portion of your Traditional IRA contribution, you can still make the contribution, but it will be considered an “after-tax” contribution. There are two reasons why we see investors make after-tax contributions to traditional IRA’s. The first is to complete a “Backdoor Roth IRA Contribution”. The second is to leverage the tax deferral accumulation component of a traditional IRA even though a deduction cannot be taken. By holding the investments in an IRA versus in a taxable brokerage account, any dividends or capital gains produced by the activity are sheltered from taxes. The downside is when you withdraw the money from the traditional IRA, all of the gains will be subject to ordinary income tax rates which may be less favorable than long term capital gains rates.

Roth IRA

If you are covered by a 401(K) plan and you want to make a contribution to a Roth IRA, the rules are more straight forward. For Roth IRAs, you make contributions with after-tax dollars but all the accumulation is received tax free as long as the IRA has been in existence for 5 years, and you are over the age of 59½. Unlike the Traditional IRA rules, where there are different income thresholds based on whether you are covered or your spouse is covered by a 401(k), Roth IRA contributions have universal income thresholds.

The contribution limits are the same as Traditional IRA’s but you have to aggregate your IRA contributions meaning you can’t make a $7,500 contribution to a Traditional IRA and then make a $7,500 contribution to a Roth IRA for the same tax year. The IRA annual limits apply to all IRA contributions made in a given tax year.

Should You Contribute To A 401(k) or an IRA?

If you have the option to either contribute to a 401(k) plan or an IRA, which one should you choose? Here are some of the deciding factors:

Employer Match: If the company that you work for offers an employer matching contribution, at a minimum, you should contribute the amount required to receive the full matching contribution, otherwise you are leaving free money on the table.

Roth Contributions: Does your 401(k) plan allow Roth contributions? Depending on your age and tax bracket, it may be advantageous for you to make Roth contributions over pre-tax contributions. If your plan does not allow a Roth option, then it may make sense to contribute pre-tax up the max employer match, and then contribute the rest to a Roth IRA.

Fees: Is there a big difference in fees when comparing your 401(k) account versus an IRA? With 401(k) plans, typically the fees are assessed based on the total assets in the plan. If you have a $20,000 balance in a 401(K) plan that has $10M in plan assets, you may have access to lower cost mutual fund share classes, or lower all-in fees, that may not be available within a IRA.

Investment Options: Most 401(k) plans have a set menu of mutual funds to choose from. If your plan does not provide you with access to a self-directed brokerage window within the 401(k) plan, going the IRA route may offer you more investment flexibility.

Easier Is Better: If after weighing all of these options, it’s a close decision, I usually advise clients that “easier is better”. If you are going to be contributing to your employer’s 401(k) plan, it may be easier to just keep everything in one spot versus trying to successfully manage both a 401(k) and IRA separately.

Maxing Out A 401(k) and IRA

As long as you are eligible from an income standpoint, you are allowed to max out both your employee deferrals in a 401(k) plan and the contributions to your IRA in the same tax year. If you are age 51, married, and your modified AGI is $180,000, you would be able to max your 401(k) employee deferrals at $32,500, you are over the income limit for deducting a contribution to a Traditional IRA, but you would have the option to contribute $8,600 to a Roth IRA.

Advanced Tax Strategy: In the example above, you are above the income threshold to deduct a Traditional IRA but your spouse may not be. If your spouse is not covered by a 401(k) plan, you can make a spousal contribution to a Traditional IRA because the $180,000 is below the income threshold for the spouse that is NOT COVERED by the employer-sponsored retirement plan.

Last updated June, 2026

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

Can you contribute to both a 401(k) and an IRA in the same year?

Yes, as long as you meet the income requirements for IRA eligibility. For example, in 2025 you could contribute the full employee deferral limit to your 401(k) ($23,000 plus $7,500 catch-up if age 50+) and still contribute up to $7,000 or $8,000 to an IRA.

What is a spousal IRA contribution?

If one spouse does not work or isn’t covered by an employer retirement plan, the working spouse can make an IRA contribution on their behalf. This strategy allows a couple to potentially double their retirement savings and may preserve tax deductibility for the non-covered spouse.

Roth Conversions In Retirement

Roth conversions in retirement are becoming a very popular tax strategy. It can help you to realize income at a lower tax rate, reduce your RMD’s, accumulate assets tax free, and pass Roth money onto your beneficiaries. However, there are pros and cons that you need to be aware of, because processing a Roth conversion involves showing more taxable income in a given year. Without proper tax planning, it could lead to unintended financial consequences such as:

· Social Security taxed at a higher rate

· Higher Medicare premiums

· Assets lost to a long term care event

· Higher taxes on long term capital gains

· Losing tax deductions and credits

· Higher property taxes

· Unexpected big tax liability

In this video, Michael Ruger will walk you through some of the strategies that he uses with his clients when implementing Roth Conversions. This can be a very effective wealth building strategy when used correctly.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Retirement Account Withdrawal Strategies

The order in which you take distributions from your retirement accounts absolutely matters in retirement. If you don’t have a formal withdraw strategy it could end up costing you in more ways than one. Click to read more on how this can effect you.

The order in which you take distributions from your retirement accounts absolutely matters in retirement. If you don’t have a formal withdraw strategy it could end up costing you more in taxes long-term, causing you to deplete your retirement assets faster, pay higher Medicare premiums, and reduce the amount of inheritance that your heirs would have received. Retirees will frequently have some combination of the following income and assets in retirement:

· Pretax 401(k) and IRA’s

· Roth IRA IRA’s

· After tax brokerage accounts

· Social Security

· Pensions

· Annuities

As Certified Financial Planner’s®, we look at an individual’s income needs, long-term goals, and map out the optimal withdraw strategy. In this article, I will be sharing with you some of the considerations that we use with our clients when determining the optimal withdrawal strategy.

Layer One : Pension Income

When you develop a withdrawal strategy for your retirement assets it’s similar to building a house. You have to start with a foundation which is taxable income that you expect to receive before you begin taking withdrawals from your retirement accounts. For retirees that have pensions, this is the first layer. Income from pensions are typically taxable income at the federal level but may or may not be taxable at the state level depending on which state you live in and who the sponsor of the pension plan is. While pensions are great, retirees that have pension income have to be very careful about how they make withdrawals from their retirement accounts because any withdraws from pre-tax accounts will stack up on top of their pension income making those withdrawal potentially subject to higher tax rates or cause you to lose tax deductions and credits that were previously received.

Layer Two: Social Security

Social Security income is also something that has to be factored into the mix. Most retirees will have to pay federal income tax on a large portion of their Social Security benefit. When we are counseling clients on their Social Security filing strategy, one of the largest influencers in that decision is what type of retirement accounts that have and how much is in each account. Delaying Social Security each year, increases the amount that an individual receives in the range of 6% to 8% per year forever. As financial planners, we view this as a “guaranteed rate of return” which is tough to replicate in other asset classes. Not turning your Social Security benefit prior to your normal retirement age can:

· Increase 50% spousal benefit

· Increase the survivor benefit

· Increase the value of SS cost of living adjustments

· Reduce the amount required to be withdrawn for other sources

For purposes of this article, we will just look at Social Security as another layer of income but know that depending on your financial situation your Social Security filing strategy does factor into your asset withdrawal strategy.

Roth Accounts: Last To Touch

In most situations, Roth assets are typically the last asset that you touch in retirement. Since Roth assets accumulate and are withdrawn tax free, they are by far the most valuable vehicle to accumulate wealth long-term. The longer they accumulate, the more valuable they are.

The other wonderful feature about Roth IRAs is that there is no required minimum distributions (RMD’s) at age 72. Meaning the government does not force you to take distributions once you have reached a certain age so you can continue to accumulate wealth within that asset class.

Roth’s are also one of the most valuable assets to pass onto beneficiaries because they can continue to accumulate tax free and are withdrawn tax free. For spousal beneficiaries, they can roll over the balance into their own Roth IRA and continue to accumulate wealth tax free. For non-spouse beneficiaries, under the new 10 year rule, they can continue to accumulate wealth for a period of up to 10 years after inheriting the Roth before they are required to distribute the full balance but they don’t pay tax on any of it.

Financial Nerd Note: While Roth are great accumulation vehicles, it’s impossible to protect them from a long term care event spend down situation. They cannot be transferred into a Medicaid trust and they are subject to full spend down for purposes of qualifying for Medicaid in New York since there is no RMD requirements. It’s just a risk that I want you to be aware of.

Pre-tax Assets

Pre-taxed retirement assets often include:

· Traditional & Rollover IRAs

· 401k / 403b / 457 plans

· Deferred compensation plans

· Qualified Annuities

When you withdraw money from these pre-tax sources you have to pay federal income tax on the amount withdrawn but you may also have to pay state income tax as well. If you live in a state that has state income tax, it’s very important to understand the taxation rules for retirement accounts within your state.

For example, New York has a unique rule that each person over the age of 59½ is allowed to withdraw $20,000 from a pre-tax retirement account without having to pay state income tax. Any amounts withdrawn over that threshold in a given tax year are subject to state income tax.

Pretax retirement accounts are usually subject to something called a required minimum distribution (RMD). The IRS requires you to start taking small distributions out of your pre-tax retirement accounts at 72. Without proper guidance, retirees often make the mistake of withdrawing from their after tax assets first, and then waiting until they are required to take the RMD’s from their pre-tax retirement accounts at age 72 and beyond. But this creates a problem for many retirees because it causes:

· The distribution to be subject to higher tax rates

· Loss of tax deductions and credits

· Increase the tax ability of Social Security Increase Medicare premiums Loss of certain property tax credits for

seniors

· Other adverse consequences……

Instead as planners, we proactively plan ahead and ask questions like:

“instead of waiting until age 72 and taking larger RMD’s from the pre-tax account, does it make sense to start making annual distribution from the pre-tax retirement accounts leading up to age 72, thus spreading those distribution in lower amounts, across more tax year resulting in:

· Lower tax liability

· Lower Medicare premiums

· Maintaining tax deductions and credits

· The assets last longer due to a lower aggregate tax liability

· More inheritance for their family members

Since everyone’s tax situation and retirement income situation is different, we have to work closely with their tax professional to determine what the right amount is to withdraw out of the pre-tax retirement accounts each year to optimize their net worth long-term.

After Tax Accounts

After tax assets can include:

· Savings accounts

· Brokerage accounts

· Non-qualified annuities

· Life Insurance with cash value

Just because I’m listing them as “after tax assets” does not mean the whole account value is free and clear of taxes. What I’m referring to is the accounts listed above typically have some “cost basis” meaning a portion of the account it what was originally contributed to the account and can be withdrawal tax fee. The appreciation within the account would be taxes at either ordinary income or capital gains rates depending on the type of the account and how long the assets have been held in the account.

Having after tax assets often provides retirees with a tax advantage because they may be able to “choose their tax rate” when they retire. Meaning they can choose to withdrawal “X” amount from an after tax source and pay little know taxes and show very little taxable income in any given year which opens the door for more long term advanced tax planning.

Withdrawal Strategies

Now that have covered all of the different types of retirement assets and how they are taxed, let move into some of the common withdrawal strategies that we use with our clients:

Retirees With All Three: Pre-tax, Roth, and After-tax Assets

When retirees have all three types of retirement account sources, the strategy usually involves leaving the Roth assets for last, and then meeting with their accountant to determine the amount that should be withdrawn out of their pre-tax and after tax accounts year to minimize the amount of aggregate taxes that they pay long term.

Example: Jim and Carol are both age 67 and just retired and they financial picture consists of the following:

Joint brokerage account: $200,000

401(k)’s: $500,000

Roth IRA‘s: $50,000

Combined Social Security: $40,000

Annual Expenses $100,000

Residents of New York State

An optimal withdrawal strategy may include the following:

Assuming we recommend that they turn on Social Security at their normal retirement age, it will provide them with $40,000 pre-tax Income, 85% of their Social Security benefit will be taxed at the federal level but there will be no state tax deal, resulting in an estimated $35,000 after tax.

That means we need an additional $65,000 after-tax per year from another source to meet their $100,000 per year in expenses. Instead of taking all the money from their joint brokerage account, we could have them rollover their 401(k) balances into Traditional IRAs and then take $20,000 distributions each from their accounts which they not have to pay state income tax on because it’s below the $20K threshold. That would result in another $40,000 in pre-tax income, translating to $35,000 after-tax.

The final $30,000 that is needed to meet their annual expenses would most likely come from their after tax brokerage account unless their accountant advises differently.

This strategy accomplishes a number of goals:

1) We are withdrawing pre-tax retirement assets in smaller increments and taking advantage of the New York

State tax free portion every year. This should result in lower total taxes paid over their lifetime as opposed to waiting until RMD’s start at age 72 and then being required to take larger distributions which could push them over the $20,000 annual limit making them subject in your state tax income tax and higher federal tax rates.

2) We are preserving the after-tax brokerage account for a longer period of time as opposed to using it all to supplement their expenses which would only last for about two years and then they would be forced to take all of their distributions from their pre-tax retirement account making them subject to a higher tax liability

3) For the Roth accounts, we are law allowing them to continue to accumulate as much as possible resulting in more tax free dollars to be withdrawn in the future, or if they pass onto their children, they are inheriting a larger assets that can be withdrawn tax free.

All Pre-Tax Retirement Savings

It’s not uncommon for retirees to have 100% of their retirement savings all within a pre-tax sources like 401(k)s, 403(b)s, traditional IRA‘s, and other types of pre-tax retirement account. This makes the withdrawal strategy slightly more tricky because if there are any big one-time expenses that are incurred during retirement, it forces the retiree to take a large withdrawal from a pre-tax source which also increases the tax liability associate the distribution.

A common situation that we often have to maneuver around is retirees that have plans to purchase a second house in retirement but in order to do that they need to have the cash to come up with a down payment. If they don’t have any after-tax retirement savings, those amounts will most likely have to come from a pre-tax account. Withdrawing $60,000 or more for a down payment can lead to a higher tax liability, higher Medicare premiums the following year, and make a larger portion of your Social Security taxable. For clients in the situation, we often have to plan a few year ahead, and will begin taking pre-text Distributions over multiple tax years leading up to the purchase of the retirement house in an effort to spread the tax liability over multiple years and avoiding the adverse tax and financial consequences of taking one large distribution.

Since many retirees are afraid of taking on debt in retirement, we often get the question in these second house situations is “Should I just take a big distribution from my retirement, pay for the house in full, and not have a mortgage?” If all of the retirement assets are tied up in pre-tax sources, it typically makes the most sense to take a mortgage which allows you to then take smaller distributions from your IRA accounts over multiple tax years to make the mortgage payments compared to taking an enormous tax hit by withdrawing $200,000+ out of a pre-tax return account in a single year.

Pensions With No Need For Retirement Accounts

For retirees that have pensions, it’s not uncommon for their pension and Social Security to provide enough income to meet all of their expenses. But these individual may also have pre-tax retirement accounts and the question becomes “what do we do with them if we don’t need them, and we expect the kids to inherit them?”

This situation often involves a Roth conversion strategy where each year we convert money from the pre-tax IRA’s over to Roth IRA’s. This allows those retirement accounts to accumulate tax free and ultimately withdrawn tax free by the beneficiaries. Versus if they continue to accumulate in pre-tax retirement accounts, the beneficiaries will have to distribute those accounts within 10 years and pay tax on the full balance.

Also when those retirees turn age 72 they have to start taking required minimum distributions which they don’t necessarily need. Since they are receiving pension and Social Security income, those distributions from the retirement accounts could be subject to higher tax rates. By proactively moving assets from a pre-tax source to a Roth source we are essentially reducing the amount of retirement assets that will be subject to RMD’s at age 72 because Roth assets are not subject to RMD‘s.

Using this Roth conversion strategy, it’s also not uncommon for us to have these retirees delay their Social Security. Since Social Security is taxable at the federal level, if we delay Social Security, it gives us more room to process larger Roth conversions because it free up those lower tax brackets. At the same time, it also allows Social Security to accumulate at a guaranteed rate of 6% - 8%.

Nerd Note: When you process these Roth conversions, make sure you’re taking into account the tax liability that’s being generated. You have to have a way to pay the taxes on the amounts converted because the money goes directly from your traditional IRA to your Roth IRA. Retirees that implement this strategy typically have large cash holdings, after tax retirement holdings, or we convert some of the money, and take pre-tax IRA distribution to cover the taxes.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Coronavirus RMD Relief: Ability To Waive Mandatory IRA Distributions In 2020

Congress passed the CARES Act in March 2020 which provides individuals with IRA, 401(k), and other employer sponsored retirement accounts, the option to waive their required minimum distribution (RMD) for the 2020 tax year.

Congress passed the CARES Act in March 2020 which provides individuals with IRA, 401(k), and other employer sponsored retirement accounts, the option to waive their required minimum distribution (RMD) for the 2020 tax year. This option is available to both individual over the age of 70½ and non-spouse beneficiaries of inherited IRA’s. In this article we will review:

The new RMD waiver rules

RMD’s for individuals age 70.5

RMD’s for beneficiaries of Inherited IRA’s

What happens if you already took your distribution for 2020?

Options for putting the RMD back into your IRA

Who Qualifies For The RMD Waiver?

Unlike other provisions in the CARES Act that require an individual to demonstrate that they have been impacted by the Coronavirus to gain access, the waiver of 2020 required minimum distributions is available to everyone. If you were age 70½ prior to December 31, 2019 or are the non-spouse beneficiary of an IRA, you are typically required to take a small distribution from your IRA each year, called an “RMD”, and pay tax on those distributions. However, for 2020, if you want to keep that money in your IRA in 2020 and avoid the tax hit associated with taking the distribution, you have the option to do so.

What If You Already Took Your RMD for 2020?

If you already received the RMD amount from your IRA for 2020, you may be able to return it to your IRA, and avoid the tax hit.

If the distribution came from your own personal IRA, not an inherited IRA, you will have two options:

OPTION 1: If the distribution happened within the last 60 days, you can simply return the money to your IRA. For this option, you are utilizing the 60-day rollover rule which allows you to take money out of an IRA, return it within 60 days, and avoid the tax liability. You are only allowed one 60-day rollover every 12 months.

OPTION 2: If the distribution took place more than 60 days ago, you will only be allowed to return it to your IRA if you qualify based on one of the four Coronavirus-Related Distribution criteria:

You, your spouse, or a dependent was diagnosed with the COVID-19

You are unable to work due to lack of childcare resulting from COVID-19

You own a business that has closed or is operating under reduced hours due to COVID-19

You have experienced adverse financial consequences as a result of being quarantined, furloughed, laid off, or having work hours reduced because of COVID-19

If you qualify under one of these items, then you will have 3-years from the date of the distribution to return the money back to your IRA and avoid the tax hit. However, while you have 3-years to return it to the IRA, if you don’t return the money to your IRA prior to December 31, 2020, you will have a tax liability in 2020 for all or a portion of that IRA distribution. It’s only when you actually return the money to your IRA that the tax liability is nullified. If you return it in a future tax year, you would have to go back and amend your 2020 tax return to recapture the taxes that were paid.

Inherited IRA – Non-spouse Beneficiary

However, if you are a non-spouse beneficiary of an IRA, the rules for returning the money to your IRA are different. If you are a non-spouse beneficiary of an IRA and you already received your RMD for 2020, you cannot return that money to your IRA to avoid the tax liability. Why is this? Beneficiaries are not eligible to make rollovers, so that disqualifies them from return the money to the IRA under the rollover rules in the CARES Act.

A Note To Our Greenbush Financial Clients

If you wish to waiver your RMD to 2020 or if have already received your RMD, and wish to process a rollover back into your IRA, 401(k), or employer sponsored plan, please contact us.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

IRA RMD Start Date Changed From Age 70 ½ to Age 72 Starting In 2020

The SECURE Act was passed into law on December 19, 2019 and with it came some big changes to the required minimum distribution (“RMD”) requirements from IRA’s and retirement plans. Prior to December 31, 2019, individuals

The SECURE Act was passed into law on December 19, 2019 and with it came some big changes to the required minimum distribution (“RMD”) requirements from IRA’s and retirement plans. Prior to December 31, 2019, individuals were required to begin taking mandatory distributions from their IRA’s, 401(k), 403(b), and other pre-tax retirement accounts starting in the year that they turned age 70 ½. The SECURE Act delayed the start date of the RMD’s to age 72. But like most new laws, it’s not just a simple and straightforward change. In this article we will review:

Old Rules vs New Rules surrounding RMD’s

New rules surrounding Qualified Charitable Distributions from IRA’s

Who is still subject to the 70 ½ RMD requirement?

The April 1st delay rule

Required Minimum Distributions

A quick background on required minimum distributions, also referred to as RMD’s. Prior to the SECURE Act, when you turned age 70 ½ the IRS required you to take small distributions from your pre-tax IRA’s and retirement accounts each year. For individuals that did not need the money, they did not have a choice. They were forced to withdraw the money out of their retirement accounts and pay tax on the distributions. Under the current life expectancy tables, in the year that you turned age 70 ½ you were required to take a distribution equaling 3.6% of the account balance as of the previous year end.

With the passing of the SECURE Act, the start age from these RMD’s is now delayed until the calendar year that an individual turns age 72.

OLD RULE: Age 70 ½ RMD Begin Date

NEW RULE: Age 72 RMD Begin Date

Still Subject To The Old 70 ½ Rule

If you turned age 70 ½ prior to December 31, 2019, you will still be required to take RMD’s from your retirement accounts under the old 70 ½ RMD rule. You are not able to delay the RMD’s until age 72.

Example: Sarah was born May 15, 1949. She turned 70 on May 15, 2019 making her age 70 ½ on November 15, 2019. Even though she technically could have delayed her first RMD to April 1, 2020, she will not be able to avoid taking the RMD’s for 2019 and 2020 even though she will be under that age of 72 during those tax years.

Here is a quick date of birth reference to determine if you will be subject to the old 70 ½ start date or the new age 72 start date:

Date of Birth Prior to July 1, 1949: Subject to Age 70 ½ start date for RMD

Date of Birth On or After July 1, 1949: Subject to Age 72 start date for RMD

April 1 Exception Retained

OLD RULE: In the the year that an individual turned age 70 ½, they had the option to delay their first RMD until April 1st of the following year. This is a tax strategy that individuals engaged in to push that additional taxable income associated with the RMD into the next tax year. However, in year 2, the individual was then required to take two RMD’s in that calendar year: One prior to April 1st for the previous tax year and the second prior to December 31st for the current tax year.

NEW RULE: Unchanged. The April 1st exception for the first RMD year was retained by the SECURE Act as well as the requirement that if the RMD was voluntarily delayed until the following year that two RMD’s would need be taken in the second year.

Qualified Charitable Distributions (QCD)

OLD RULES: Individuals that had reached the RMD age of 70 ½ had the option to distribute all or a portion of their RMD directly to a charitable organization to avoid having to pay tax on the distribution. This option was reserved only for individuals that had reached age 70 ½. In conjunction with tax reform that took place a few years ago, this has become a very popular option for individuals that make charitable contributions because most individual taxpayers are no longer able to deduct their charitable contributions under the new tax laws.

NEW RULES: With the delay of the RMD start date to age 72, do individuals now have to wait until age 72 to be eligible to make qualified charitable distributions? The answer is thankfully no. Even though the RMD start date is delayed until age 72, individuals will still be able to make tax free charitable distributions from their IRA’s in the calendar year that they turn age 70 ½. The limit on QCDs is still $100,000 for each calendar year.

NOTE: If you plan to process a qualified charitable distributions from your IRA after age 70 ½, you have to be well aware of the procedures for completing those special distributions otherwise it could cause those distributions to be taxable to the owner of the IRA. See the article below for more on this topic:

ANOTHER NEW RULE: There is a second new rule associated with the SECURE Act that will impact this Qualified Charitable Distribution strategy. Under the old tax law, individuals were unable to contribute to Traditional IRA’s past the age of 70 ½. The SECURE Act eliminated that rule so individuals that have earned income past age 70 ½ will be eligible to make contributions to Traditional IRAs and take a tax deduction for those contributions.

As an anti-abuse provision, any contributions made to a Traditional IRA past the age of 70 ½ will, in aggregate, dollar for dollar, reduce the amount of your qualified charitable distribution that is tax free.

Example: A 75 year old retiree was working part-time making $20,000 per year for the past 3 years. To reduce her tax bill, she contributed $7,000 per year to a traditional IRA which is allowed under the new tax laws. This year she is required to take a $30,000 required minimum distribution (RMD) from her retirement accounts and she wants to direct that all to charity to avoid having to pay tax on the $30,000. Because she contributed $21,000 to a traditional IRA past the age of 70 ½, $21,000 of the qualified charitable distribution would be taxable income to her, while the remaining $9,000 would be a tax free distribution to the charity.

$30,000 QCD – $21,000 IRA Contribution After Age 70 ½ = $9,000 tax free QCD

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

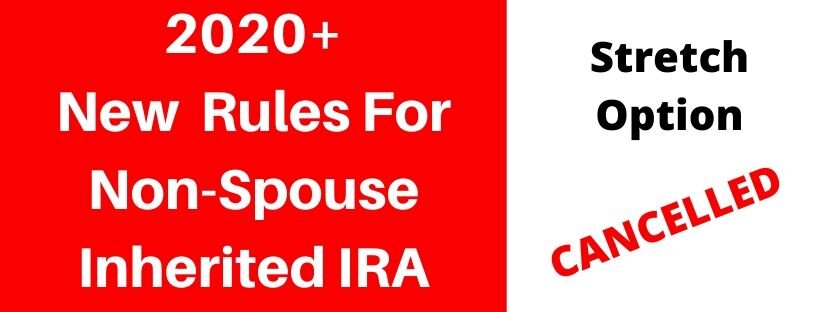

New Rules For Non Spouse Beneficiaries Of Retirement Accounts Starting In 2020

The SECURE Act was signed into law on December 19, 2019 and with it comes some very important changes to the options that are available to non-spouse beneficiaries of IRA’s, 401(k), 403(b), and other types of retirement accounts

The SECURE Act was signed into law on December 19, 2019 and with it comes some very important changes to the options that are available to non-spouse beneficiaries of IRA’s, 401(k), 403(b), and other types of retirement accounts starting in 2020. Unfortunately, with the passing of this law, Congress took away one of the most valuable distribution options available to non-spouse beneficiaries called the “stretch” provision. Non-spouse beneficiaries would utilize this distribution option to avoid the tax hit associated with having to take big distributions from pre-tax retirement accounts in a single tax year. This article will cover:

The old inherited IRA rules vs. the new inherited IRA rules

The new “10 Year Rule”

Who is grandfathered in under the old inherited IRA rules?

Impact of the new rules on minor children beneficiaries

Tax traps awaiting non spouse beneficiaries of retirement accounts

The “Stretch” Option Is Gone

The SECURE Act’s elimination of the stretch provision will have a big impact on non-spouse beneficiaries. Prior to January 1, 2020, non-spouse beneficiaries who inherited retirement accounts had the option to either:

Take a full distribution of the retirement account within 5 years

Rollover the balance to an inherited IRA and stretch the distributions from the retirement account over their lifetime. Also known as the “stretch option”.

Since any money distributed from a pre-tax retirement account is taxable income to the beneficiary, many non-spouse beneficiaries would choose the stretch option to avoid the big tax hit associated with taking larger distributions from a retirement account in a single year. Under the old rules, if you did not move the money to an inherited IRA by December 31st of the year following the decedent’s death, you were forced to take out the full account balance within a 5 year period.

On the flip side, the stretch option allowed these beneficiaries to move the retirement account balance from the decedent’s retirement account into their own inherited IRA tax and penalty free. The non-spouse beneficiary was then only required to take small distributions each year from the account called a RMD (“required minimum distribution”) but was allowed to keep the retirement account intact and continuing to accumulate tax deferred over their lifetime. A huge benefit!

The New 10 Year Rule

For non-spouse beneficiaries, the stretch option was replaced with the “10 Year Rule” which states that the balance in the inherited retirement account needs to be fully distributed by the end of the 10th year following the decedent’s date of death. The loss of the stretch option will be problematic for non-spouse beneficiaries that inherit sizable retirement accounts because they will be forced to take larger distributions exposing those pre-tax distributions to higher tax rates.

RMD Requirement Depends on the Age of the Decedent

Whether or not the beneficiary of the inherited retirement account will need to take an RMD during the 10 year period, depends on the decedent age when that passed away. If the decedent was taking RMDs at the time they passed away, the beneficiary must continue to take annual RMD during the 10 year period. If the decedent died prior to the RMD start age, the beneficiary not required to take RMDs during the 10 year period.

Tax Traps For Non-Spouse Beneficiaries

These new inherited IRA distribution rules are going to require proactive tax and financial planning for the beneficiaries of these retirement accounts. I’m lumping financial planning into that mix because taking distributions from pre-tax retirement accounts increases your taxable income which could cause the following things to happen:

Reduce the amount of college financial aid that your child is receiving

Increase the amount of your social security that is considered taxable income

Loss of property tax credits such as the Enhanced STAR Program

Increase your Medicare Part B and Part D premiums the following year

You may phase out of certain tax credits or deductions that you were previously receiving

Eliminate your ability to contribute to a Roth IRA

Loss of Medicaid or Special Needs benefits

Ordinary income and capital gains taxed at a higher rate

You really have to plan out the next 10 years and determine from a tax and financial planning standpoint what is the most advantageous way to distribute the full balance of the inherited IRA to minimize the tax hit and avoid triggering an unexpected financial consequence associated with having additional income during that 10 year period.

Who Is Grandfathered In?

If you are the non-spouse beneficiary of a retirement account and the decedent passed away prior to January 1, 2020, you are grandfathered in under the old inherited IRA rules. Meaning you are still able to utilize the stretch provision. Here are a few examples:

Example 1: If you had a parent pass away in 2018 and in 2019 you rolled over their IRA into your own inherited IRA, you are not subject to the new 10 year rule. You are allowed to stretch the IRA distributions over your lifetime in the form of those RMD’s.

Example 2: On December 15, 2019, your father passed away and you are listed as the beneficiary on his 401(k) account. Since he passed away prior to January 1, 2020, you would still have the option of setting up an Inherited IRA prior to December 31, 2020 and then stretching the distributions over your lifetime.

Example 3: On February 3, 2020, your uncle passes away and you are listed as a beneficiary on his Rollover IRA. Since he passed away after January 1, 2020, you would be required to distribute the full IRA balance prior to December 31, 2030.

You are also grandfathered in under the old rules if:

The beneficiary is the spouse

Disabled beneficiaries

Chronically Ill beneficiaries

Individuals who are NOT more than 10 years younger than the decedent

Certain minor children (see below)

Even beyond 2020, the beneficiaries listed above will still have the option to rollover the balance into their own inherited IRA and then stretch the required minimum distributions over their lifetime.

Minor Children As Beneficiaries

The rules are slightly different if the beneficiary is the child of the decedent AND they are still a minor. I purposely capitalized the word “and”. Within the new law is a “Special Rule for Minor Children” section that states if the beneficiary is a child of the decedent but has not reached the age of majority, then the child will be able to take age-based RMD’s from the inherited IRA but only until they reach the age of majority. Once they are no longer a minor, they are required to distribute the remainder of the retirement account balance within 10 years.

Example: A mother and father pass away in a car accident and the beneficiaries listed on their retirement accounts are their two children, Jacob age 10, and Sarah age 8. Jacob and Sarah would be able to move the balances from their parent’s retirements accounts into an inherited IRA and then just take small required minimum distributions from the account based on their life expectancy until they reach age 18. In their state of New York, age 18 is the age of majority. The entire inherited IRA would then need to be fully distributed to them before the end of the calendar year of their 28th birthday.

This exception only applies if they are a child of the decedent. If a minor child inherits a retirement account from a non-parent, such as a grandparent, then they are immediately subject to the 10 year rule.

Note: the age of majority varies by state.

Advanced Planning

Under the old inherited IRA rules there was less urgency for immediate tax planning because the non-spouse beneficiaries just had to move the money into an inherited IRA the year after the decedent passed away and in most cases the RMD's were relatively small resulting in a minimal tax impact. For non-spouse beneficiaries that inherit a retirement account after January 1, 2020, it will be so important to have a tax plan and financial plan in place as soon as possible otherwise you could lose a lot of your inheritance to higher taxes or other negative consequences associated with having more income during those distribution years.

Please feel free to contact us if you have any questions on the new inherited IRA rules. We would also be more than happy to share with you some of the advanced tax strategies that we will be using with our clients to help them to minimize the tax impact of the new 10 year rule.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.