Should You Make Pre-tax or Roth 401(k) Contributions?

When you become eligible to participate in your employer’s 401(k), 403(b), or 457 plan, you will have to decide what type of contributions that you want to make to the plan.

When you become eligible to participate in your employer’s 401(k), 403(b), or 457 plan, you will have to decide what type of contributions you want to make to the plan. Most employer-sponsored retirement plans now offer employees the option to make either Pre-tax or Roth contributions. A number of factors come into play when deciding what source is the right one for you, including:

Age

Income level

Marital status

Income needed in retirement

Withdrawal plan in retirement

Abnormal income years

You must consider all of these factors before making the decision to contribute either pre-tax or Roth to your retirement plan.

Pre-tax vs Roth Contributions

First, let’s start off by identifying the differences between pre-tax and Roth contributions. It’s pretty simple and straightforward. With pre-tax contributions, the strategy is “don’t tax me on it now, tax me on it later”. The contributions are deducted from your gross pay; they deduct FICA tax, but they do not withhold federal or state tax, which, in doing so, you are essentially lowering the amount of your income that is subject to federal and state income tax in that calendar year. The full amount is deposited into your 401K, the balance accumulates tax deferred, and then, when you retire and pull money out, that is when you pay tax on it. The tax strategy here is taking income off the table when you are working and in a higher tax bracket, and then paying tax on that money after you are retired, your paychecks have stopped, and you are hopefully in a lower tax bracket.

With Roth contributions, the strategy is “pay tax on it now, don’t pay tax on it later”. When your contributions are deducted from your pay, they withhold FICA, as well as Federal and State income tax, but when you withdraw the money in retirement, you don’t have to pay tax on any of it INCLUDING all of the earnings.

Age

Your age and your time horizon to retirement are a big factor to consider when trying to decide between pre-tax or Roth contributions. In general, the younger you are and the longer your time horizon to retirement, the more it tends to favor Roth contributions because you have more years to build the earning in the account which will eventually be withdrawn tax-free. In contrast, if you’re within 10 years to retirement, you have a relatively short period of time before withdrawals will begin from the account, making pre-tax contributions may make the most sense.

When you end up in one of those mid time horizon ranges like 10 to 20 years to retirement, the other factors that we’re going to discuss have a greater weight in arriving at your decision to do pre-tax or Roth.

Income level

Your level of income also has a big impact on whether pre-tax or Roth makes sense. In general, the higher your level of income, the more it tends to favor pre-tax contributions. In contrast, lower to medium levels of income, can favor Roth contributions. Remember pre-tax is “don’t tax me on it now, tax me on it later”, and the strategy is you are assuming that you are in a higher tax bracket now during your earning years then you will be in retirement when you don’t have a paycheck. By contrast, a 22 year old, that has accepted their first job, will most likely be at the lowest level of income over their working career, and have the expectation that their earnings will grow overtime. This situation would favor making Roth contributions because you are paying tax on the contributions while you are still in a low tax bracket and then later on when your income rises, you can switch over to pre-tax.

Marital status

Your marital status matters because if you’re married and you file a joint tax return, you have to consider not just your income but your spouse’s income. If you make $30,000 a year, that might lead you to think that Roth is a good option, but if your spouse makes $200,000 a year, your combined income on your joint tax return is $230,000 which puts you in a higher tax bracket. Assuming you’re not going to need $230,000 per year to live off of in retirement, pre-tax contributions may be more appropriate because you want the tax deduction now.

A change in your marital status can also influence the type of contributions that you’re making to the plan. If you are a single filer making $50,000 a year, you may have been making Roth contributions but then you get married and your spouse makes $100,000 a year, since your income will now be combined for tax filing purposes, it may make sense for you to change your elections to pre-tax contributions.

These changes can also take place when one spouse retires and the other is still working. Prior to the one spouse retiring, both were earning income, and both were making pre-tax contributions. Once one of the spouses retires the income level drops, the spouse that is still working may want to switch to Roth contributions given their much lower tax rate.

Withdrawal plan in retirement

You also have to look ahead to your retirement years and estimate what your income picture might look like. If you anticipate that you will need the same level in retirement that you have now, even though you might have a shorter time horizon to retirement, it may favor making Roth contributions because your tax rate is not anticipated to drop in the retirement years. So why not pay tax on the contributions now and then receive the earnings on the account tax-free, as opposed to making pre-tax contributions and having to pay tax on all of it. The benefit associated with pre-tax contributions assumes that you’re in a higher tax rate now and when you withdraw the money you will be in a lower tax bracket.

Some individuals accumulate balances in their 401(k) accounts but they also have pensions. As they get closer to retirement, they realize between their pension and Social Security, they will not need to make withdrawals from their 401(k) account to supplement their income. In many of those cases, we can assume a much longer time horizon for those accounts which may begin to favor Roth contributions. Also, if those accounts are going to continue to accumulate and eventually be inherited by their children, from a tax standpoint, it’s more beneficial for children to inherit a Roth account versus a pre-tax retirement account because they have to pay tax on all of the money in a pre-tax retirement account as some point.

Abnormal income years

It’s not uncommon during your working years to have some abnormal income years where your income ends up being either significantly higher or significantly lower than it normally is. In these abnormal years it often makes sense to change your pre-tax or Roth approach. If you are a business owner, you typically make $300,000 per year, but the business has a bad year, and you’re only going to make $50,000 this year, instead of making your usual pre-tax contributions, it may make sense to contribute Roth that year. If you are a W-2 employee, and the company that you work for is having a really good year, and you expect to receive a big bonus at the end of the year, if you’re contributing Roth it may make sense to switch to pre-tax anticipating that your income will be much higher for the tax year.

Another exception can happen in the year that you retire. Some companies will issue bonuses or paid out built up sick time or vacation time which can count as taxable income. In those years it may make sense to make larger pre-tax contributions because the income in that final year may be much higher than normal.

Frequently Asked Questions About Roth Contributions

When we are educating 401K plan participants on this topic, there are a few frequently asked questions that we receive:

Do all retirement plans allow Roth contributions?

ANSWER: No, Roth contributions are a voluntary contribution source that a company has to elect to offer to its employees. We are seeing a lot more plans that offer this benefit but not all plans do.

Can you contribute both Pre-Tax and Roth at the same time to the plan?

ANSWER: Yes, if your plan allows Roth contributions you are normally able to contribute both pre-tax and Roth to the plan simultaneously. However, the annual deferral limits are aggregated for purposes of all employee elective deferrals. For example, in 2025, the maximum employee deferral limits are as follows:

Under the age of 50: $23,500

Age 50-59 and 64 and over: $31,000

Age 60-63: $34,750

You can contribute all pre-tax, all Roth, or any combination of the two but those amounts are aggregated together for purposes of assessing the annual dollar limits.

Do you have to set up a separate account for your Roth contributions to the 401K?

ANSWER: No. The Roth contributions that you make out of your paycheck to the plan are just tracked as a separate source within the 401K plan. They have to do this because when it comes to withdrawing the money, they have to know how much of your account balance is pre-tax and what amount is Roth. Typically, on your statements, you will see your total balance, and then it breaks it down by money type within your account.

What happens when I retire and I have Roth money in my 401K account?

ANSWER: For those that contribute Roth to their accounts, it's common for them to have both pre-tax and Roth money in their account when they retire. The pre-tax money could be from employee deferrals that you made or from the employer contributions. When you retire, you can set up both a rollover IRA and a Roth IRA to receive the rollover balance from each source.

SPECIAL NOTE: The Roth source has a special 5 year holding rule. To be able to withdraw the earnings from the Roth source tax free, you have to be over the age of 59 ½ AND the Roth source has to have been in existence for at least 5 years. Here is the problem, that five-year holding clock does not transfer over from a Roth 401(k) to a Roth IRA. If you did not have a Roth IRA a prior to the rollover, you would have to re satisfy the five-year holding period within the Roth IRA before making withdraws. We normally advise clients in this situation that they should set up a Roth IRA with $1 five years prior to retirement to start that five-year clock within the Roth IRA so by the time they rollover the Roth 401(k) balance they are free and clear of the 5 year holding period requirement. (Assuming their income allows them to make a Roth IRA contribution during that $1 year)

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What’s the difference between pre-tax and Roth contributions in a 401(k), 403(b), or 457 plan?

Pre-tax contributions reduce your taxable income now—you defer paying taxes until retirement when you withdraw the money. Roth contributions are made after taxes, meaning you pay taxes upfront, but qualified withdrawals in retirement (including earnings) are tax-free.

How does age influence whether you should contribute pre-tax or Roth?

Generally, younger workers with longer time horizons benefit more from Roth contributions because their investments can grow tax-free for decades. Those closer to retirement often prefer pre-tax contributions to reduce taxes while earning income and defer taxation until retirement.

Does income level affect whether to choose pre-tax or Roth contributions?

Yes. Higher earners often benefit more from pre-tax contributions because they receive a larger tax deduction now and may be in a lower tax bracket later. Workers in lower or moderate tax brackets may prefer Roth contributions since they’re paying tax at relatively low rates today.

How does marital status impact pre-tax vs Roth decisions?

Married couples filing jointly must consider combined income. If one spouse earns significantly more, the higher joint tax bracket may favor pre-tax contributions. However, when a spouse retires or income drops, switching to Roth contributions may make sense to take advantage of lower tax rates.

What if I expect to have the same income in retirement?

If you expect to maintain similar income levels in retirement—due to pensions, Social Security, or investment withdrawals—Roth contributions may be advantageous. Paying taxes now locks in today’s rates and provides tax-free withdrawals later.

Should I adjust my contribution type during abnormal income years?

Yes. In unusually high-income years, pre-tax contributions can help reduce taxable income. In lower-income years—such as a slow business year or partial-year retirement—it may make sense to switch to Roth contributions and pay taxes at a lower rate.

Can I contribute to both pre-tax and Roth sources at the same time?

Yes, most plans allow you to split your contributions between pre-tax and Roth. However, the combined total can’t exceed the annual IRS deferral limits ($23,500 for those under 50; up to $34,750 for those aged 60–63 in 2025).

Do I need a separate account for Roth 401(k) contributions?

No. Both pre-tax and Roth balances are held within the same plan but tracked separately. Your statements will show how much of your balance is Roth versus pre-tax for proper tax treatment at withdrawal.

What happens to my Roth 401(k) when I retire?

At retirement, you can roll your pre-tax funds to a traditional IRA and your Roth funds to a Roth IRA. Keep in mind that Roth IRAs have a five-year rule—you must have held a Roth IRA for at least five years before earnings can be withdrawn tax-free.

Cash Balance Plans: $100K to $300K in Pre-tax Contributions

DB/DC combo plans can allow business owners to contribute $100,000 to $300,000 pre-tax EACH YEAR which can save them tens of thousands of dollars in taxes.

A Cash Balance Plan for small business owners can be one the best ways to shelter large amounts of income from taxation each year. Most small business owners are familiar with 401(K) plans, SEP IRA’s, Solo(k) Plans, and Simple IRA’s, but these “DB/DC Combo” plans bring the tax savings for business owners to a whole new level. DB/DC combo plans can allow business owners to contribute $100,000 to $300,000 pre-tax EACH YEAR which can save them tens of thousands of dollars in taxes. In this article I’m going to walk you through:

How cash balance plans and DB/DC combo plans work

Which companies are the best fit for these plans

How the contribution amount is calculated each year

Why an actuary is involved

How long should these plans be in place for?

The cost of maintaining these plans

How they differ from 401(k) plans, SEP IRA, Solo(k), and Simple IRA plans

The Right Type of Company

When we put one of these DB/DC combo plans in place for a client, most of the time, the company has the following characteristics:

Less than 20 full time employees

The business is producing consistent cash flow

Business owners are making $300K or more per year

Business owner is looking for a way to dramatically reduce their tax liability

Company already sponsors either a 401(k), Solo(k), Simple IRA, or SEP IRA

What Is A Cash Balance Plan?

This special plan design involves running a 401(k) plan and Cash Balance Plan side by side. 401(K) plans, SEP IRAs, and Simple IRAs are considered a “defined contribution plans”. As the name suggests, a defined contribution plan defines the maximum hard dollar amount that you can contribute to the plan each year. The calculation is based on the current, here and now benefit. For 2025, the maximum annual contribution limits for a 401(k) plan is either $70,000 or $77,500 depending on your age.

A Cash Balance Plan is considered a “defined benefit plan”; think a pension plan. Defined benefit plans define the benefit that will be available to you at some future date and the contribution that is required today is a calculation based on the dollar amount needed to meet that future benefit. They have caps but the caps are much higher than defined contribution plans and they vary based on the age and compensation of the business owner. Also, even though they are pension plans, they typically payout the benefit as a lump sum pre-tax amount that can be rolled over to either an IRA or other type of qualified plan.

As mentioned earlier, these Combo plans can provide annual pre-tax contribution in excess of $300,000 per year for some business owners. Now that is the maximum but you do not have to design your plan to be based on the maximum contribution. Some small business owners would prefer to just contribute $100,000 - $150,000 pre-tax per year if that was available, and these combo plans can be designed to meet those contribution levels.

Employee Demographic

Employee demographic play a huge role as to whether or not these plans work for a given company. Similar to 401(K) plans, cash balance plans are subject to nondiscrimination testing year which requires the company to make an employer contribution to eligible employees based on amounts that are contributed to the owner’s accounts. But it’s not as big of a jump in contribution level to the employees that many business owners expect. It's not uncommon a company to already be sponsoring a company retirement plan which is providing the employees with an employer contribution equal to 3% to 5% of the employees annual compensation. Many of these DB/DC combo plans only require a 7.5% total contribution to pass testing. Thus, making an additional 2.5% of compensation contributions to the employees can open up $100,000 - $250,000 in additional pre-tax contributions for the business owner. In many cases, the tax savings for the business owner more than pays for the additional contribution to the employee so everyone wins. The employee get more and the business owner gets a boat load of tax savings.

The age and annual compensation of the owner versus the employees also has a large impact. In general, this plan design works the best for businesses where the average age of the employees is much lower than the age of the business owner, and the business owner’s compensation is much higher than that of the average employee. These plans are very common for dentists, doctors, lawyers, consultants, and any other small business that fits this owner vs employee demographic.

If you have no employees or it’s an owner only entity, even better. You just graduated to the higher contribution level without additional contributions to employees.

Reminder: You only have to count full time employees. ERISA defines full time employees as being employed for at least 1 year and working over 1,000 hours during that one year period. If you have employees working less than 1,000 hours a year, they may never become eligible for the plan.

The 3 Year Rule

When you adopt a Cash Balance Plan, you typically have to keep the plan in place for at least 3 years. The IRS does not want you to have one great year, contribute $300,000 pre-tax, and then terminate the plan the next year. Unlike 401(k) plans, cash balance plans have minimum funding requirements each year which is why businesses have to have more predictable revenue streams for this plan design to makes sense.

However, you can build in fail safe into the plan design to help protect against bad years in the business. Since no business owner knows what is going to happen over the next three years, we can build into the plan design a “lesser of” statement which calculates the contribution for the business owner based on the “lesser of the ERISA max comp limit for the year or the owners comp for that tax year.” If the business owner makes $500,000, they would use the ERISA comp limit of $350,000 for 2025. If it’s a horrible year and the business owner only makes $50,000 that year, the required contribution would be based on that lower compensation level, reducing the required contribution for that year.

After 3 years, the company has the option to voluntarily terminate the cash balance plan, and the business owner can rollover his or her balance into the 401(k) plan or rollover IRA.

Contributions Are Due Tax Filing Deadline Plus Extension

The company is not required to fund these plans until tax filing deadline plus extension. If the business is a 12/31 fiscal year end and you adopt the plan in November, you would not be required to fund the contribution until either September 15th or October 15th of the following year depend on how your business is incorporated.

Assumed Rates of Return

Unlike a 401(k) plan where each employee has their own account that they have control over, Cash Balance Plans are pooled investment account, because the company is responsible for producing the rate of return in the account that meets or beats the actuarial assumptions. The annual rate of return target for the cash balance plan can sometimes be tied to a treasury bond yield, flat rate, or other metric used by the actuary within the ERISA guidelines. If the plan assets underperform the assumed rate of return, it could increase the required contribution for that year. Vice versa, if the plan assets outperform the assumed rate, it can decrease the required contribution for the year. The additional risk taken on by the company has to be considered when selecting the appropriate asset allocation for the cash balance account.

Annual Plan Fees

Since cash balance plans are defined benefit plans, you will need an actuary to calculate the required minimum contribution each year. Since most of these plans are DC/DB combo plans, the 401(K) plan and the Cash Balance Plan need to be tested together for purposes of passing year end testing. A full 401(k) may carry $1,000 - $3,000 in annual administration cost each year depending on your platform, whereas running both a 401(K) and Cash Balance Plan may increase those administration costs to $4,000 - $7,000 depending again on the platform and the number of employees.

While these plans can carry a higher cost, you have to weigh it against the tax savings that the business owner is realizing by having the DC/DB combo plan in place. If they are able to contribute an additional $200,000 over just their 401(K), that could save them $80,000 in taxes. Many business owners in the top tax bracket are willing to pay an additional $3,000 in admin fees to save $80,000 in taxes.

Run Projections

As a business owner, you have to weigh the additional costs of sponsoring the plan against the amount of your tax savings. For the right company, these combo plans can be fantastic but it’s not a set it and forget it type plan design. As the employee demographics within the company change over the years it can impact this cost benefit analysis. We have seen cases where hiring just one employee has thrown off the whole plan design a year later.

If you would like to learn more about this plan design or would like us to run a projection for your company, feel free to reach out to us for a complementary consult.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What is a Cash Balance Plan and how does it work?

A Cash Balance Plan is a type of defined benefit plan that allows higher pre-tax contributions than traditional retirement plans. When combined with a 401(k) in a DB/DC combo structure, business owners can contribute $100,000–$300,000 annually, significantly reducing taxable income while building retirement assets.

Which businesses are best suited for a Cash Balance or DB/DC combo plan?

These plans work best for small businesses with fewer than 20 employees, strong and consistent cash flow, and owners earning $300,000 or more annually. They are especially common among professionals such as doctors, dentists, attorneys, and consultants seeking larger tax deductions.

How are contribution amounts determined in a Cash Balance Plan?

Contributions are calculated by an actuary and depend on the business owner’s age, compensation, and desired future benefit. Older owners typically qualify for higher contribution limits because they have fewer years to fund their target benefit.

Why does a Cash Balance Plan require an actuary?

An actuary certifies the plan’s annual minimum funding requirement and ensures compliance with IRS and ERISA rules. Because the employer guarantees a specific benefit, actuarial calculations are needed each year to maintain funding accuracy.

How long must a Cash Balance Plan remain in place?

The IRS generally requires that the plan stay in place for at least three years. After that period, it can be voluntarily terminated, and funds are typically rolled into a 401(k) or IRA without tax penalties.

When are contributions due for a Cash Balance Plan?

Contributions are due by the company’s tax filing deadline, including extensions. For most calendar-year businesses, that means the funding deadline falls between September and October of the following year.

What are the typical costs of maintaining a Cash Balance Plan?

Annual administrative and actuarial fees often range from $4,000 to $7,000 for companies running both a 401(k) and Cash Balance Plan. Despite higher costs, the potential tax savings—often $30,000 or more per year—can far outweigh the administrative expenses.

How do Cash Balance Plans differ from 401(k), SEP, and SIMPLE IRA plans?

Unlike defined contribution plans with fixed annual limits, Cash Balance Plans are defined benefit plans with much higher potential contribution amounts. They also require actuarial oversight, minimum funding each year, and pooled investments managed by the employer rather than individual accounts.

What Caused The Market To Sell Off In September?

What Caused The Market To Sell Off In September?

The stock market experienced a fairly significant drop in the month of September. In September, the S&P 500 Index dropped 4.8% which represents the sharpest monthly decline since March 2020. I wanted to take some time today to evaluate:

· What caused the market drop?

· Do we think this sell off is going to continue?

· Have the recent market events caused us to change our investment strategy?

September Is Historically A Bad Month

Looking back at history, September is historically the worse performing month for the stock market. Since 1928, the S&P 500 Index has averaged a 1% loss in September (WTOP News). Most investors have probably forgotten that in September 2020, the market experienced a 10% correction, but rallied significantly in the 4th quarter.

The good news is the 4th quarter is historically the strongest quarter for the S&P 500. Since 1945, the stock market has averaged a 3.8% return in the final three months of the year (S&P Global).

The earned income penalty ONLY applies to taxpayers that turn on their Social Security prior to their normal retirement age. Once you have reached your normal retirement age, this penalty does not apply.

Delta Variant

The emergence of the Delta Variant slowed economic activity in September. People cancelled travel plans, some individuals avoided restaurants and public events, employees were out sick or quarantined, and it delayed some companies from returning 100% to an office setting. However, we view this as a temporary risk as vaccination rates continue to increase, booster shots are distributed, and the death rates associated with the virus continue to stay at well below 2020 levels.

China Real Estate Risk

Unexpected risks surfaced in the Chinese real estate market during September. China's second largest property developer Evergrande Group had accumulated $300 billion in debt and was beginning to miss payments on its outstanding bonds. This spread fears that a default could cause issues other places around the globe. Those risks subsided as the month progressed and the company began to liquidate assets to meet its debt payments.

Rising Inflation

In September we received the CPI index report for August that showed a 5.3% increase in year over year inflation which was consistent with the higher inflation trend that we had seen earlier in the year. In our opinion, inflation has persisted at these higher levels due to:

· Big increase in the money supply

· Shortage of supply of good and services

· Rising wages as companies try to bring employees back into the workforce

The risk here is if the rate of inflation continues to increase then the Fed may be forced to respond by raising interest rates which could slow down the economy. While we acknowledge this as a risk, the Fed does not seem to be in a hurry to raise rates and recently announced plans to pare back their bond purchases before they begin raising the Fed Funds Rate. Fed Chairman Powell has called the recent inflation trend “transitory” due to a bottleneck in the supply chain as company rush to produce more computer chips, construction materials, and fill labor shortages to meet consumer demand. Once people return to work and the supply chain gets back on line, the higher levels of inflation that we are seeing could subside.

Rising Rates Hit Tech Stocks

Interest rates rose throughout the month of September which caused mortgage rates to move higher, but more recently there has been an inverse relationship between interest rates and tech stocks. As interest rates rise, tech stocks tend to fall. We attribute this largely to the higher valuations that these tech stocks trade at. As interest rates rise, it becomes more difficult to justify the multiples that these tech stocks are trading at. It is also important to acknowledge that these tech companies have become so large that the tech sector now represents about 30% of the S&P 500 Index (JP Morgan Guide to the Markets).

Risk of a Government Shutdown

Toward the end of the month, the news headlines were filled with the risk of the government shutdown which has been a reoccurring issue for the U.S. government for the past 20 years. This was nothing new, but it just added more uncertainty to the pile of negative headlines that plagued the markets in September. It was announced on September 30th that Congress had approved a temporary funding bill to extend the deadline to December 3rd.

Expectation Going Forward

Even though the Stock Market faced a pile of bad news in September, our internal investment thesis at our firm has not changed. Our expectation is that:

· The economy will continue to gain strength in coming quarters

· There is a tremendous amount of liquidity still in the system from the stimulus packages that has yet to be spent

· People will begin to return to work to produce more goods and services

· Those additional goods and services will then ease the current supply chain bottleneck

· Interest rates will move higher but they still remain at historically low levels

· The risk of the delta variant will diminish increasing the demand for travel

We will continue to monitor the economy, financial markets, and will release more articles in the future as the economic conditions continue to evolve in the coming months.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Do You Have To Pay Tax On Your Social Security Benefits?

I have some unfortunate news. If you look at your most recent paycheck, you are going to see a guy by the name of “FICA” subtracting money from your take-home pay. Part of that FICA tax is sent to the Social Security system, which entitles you to receive Social Security payments when you retire. The unfortunate news is that, even though it was a tax that you paid while you were working, when you go to receive your payments from Social Security, most retirees will have to pay some form of Income Tax on it. So, it’s a tax you pay on a tax? Pretty much!

In this article, I will be covering:

· The percent of your Social Security benefit that will be taxable

· The tax rate that you pay on your Social Security benefits

· The Social Security earned income penalty

· State income tax exceptions

· Withholding taxes from your Social Security payments

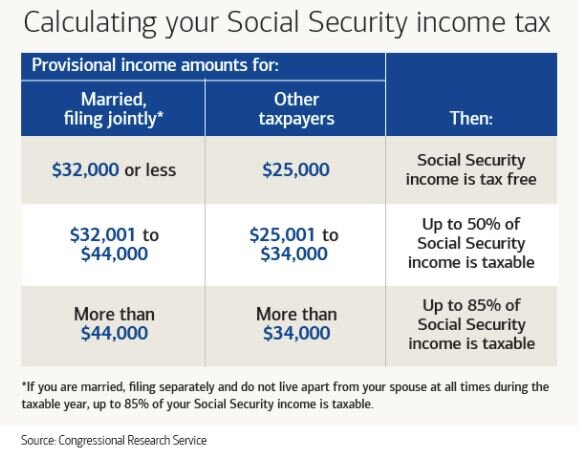

What percent of your Social Security benefit is taxable?

First, let’s start off with how much of your Social Security will be considered taxable income. It ranges from 0% to 85% of the amount received. Where you fall in that range will depend on the amount of income that you have each year. Here is the table for 2025:

But, here’s the kicker. 50% of your Social Security benefit that you receive counts towards the income numbers that are listed in the table above to arrive at your “combined Income” amount. Here is the formula:

Adjusted Gross Income (AGI) + nontaxable interest + 50% of your SS Benefit = Combined Income

If you are a single tax filer, and you are receiving $30,000 in Social Security benefits, you are already starting at a combined income level of $15,000 before you add in any of your other income from employment, pensions, pre-tax distributions from retirement accounts, investment income, or rental income.

As you will see in the table, if your combined income for a single filer is below $25,000, or a joint filer below $32,000, you will not have to pay any tax on your Social Security benefit. Taxpayers above those thresholds will have to pay some form of tax on their Social Security benefits. But, I have a small amount of good news: no one has to pay tax on 100% of their benefit, because the highest percentage is 85%. Therefore, everyone at a minimum receives 15% of their benefit tax free.

NOTE: The IRS does not index the combined income amounts in the table above for inflation, meaning that even though an individual’s Social Security and wages tends to increase over time, the dollar amounts listed in the table stay the same from year to year. This has caused more and more taxpayers to have to pay tax on a larger portion of their Social Security benefit over time.

Tax Rate on Social Security Benefits

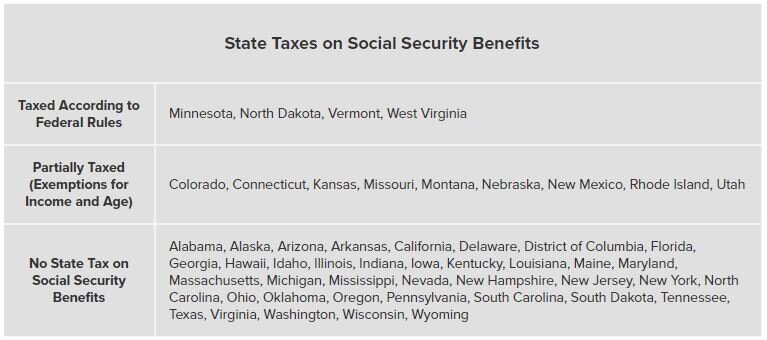

Your Social Security benefits are taxed as ordinary income. There are no special tax rates for Social Security like capital gains rates for investment income. Social Security is taxed at the federal level but may or may not be taxed at the state level. Currently there are 37 states in the U.S. that do not tax Social Security benefits. There are 4 states that tax it at the same level as the federal government and there are 13 states that partially tax the benefit. Here is table:

Withholding Taxes From Your Social Security Benefit

For taxpayers that know that will have to pay tax on their Social Security benefit, it is usually a good idea to have Social Security withholding taxes taken directly from your Social Security payments. Otherwise, you will have to issue checks for estimated tax payments throughout the year which can be a headache. They only provide you with four federal tax withholding options:

7%

0%

12%

22%

These percentages are applied to the full amount of your Social Security benefit, not to just the 50% or 85% that is taxable. Just something to consider when selecting your withholding elections.

To make a withholding election, you have to complete Form W-4V (Voluntary Withholding Request). Once you have completed the form, which only has 7 lines, you can mail it or drop it off at the closest Social Security Administration office.

Social Security Earned Income Penalty

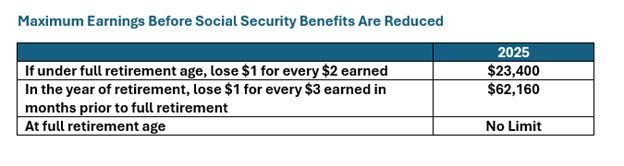

If you elect to turn on your Social Security benefit prior to your Normal Retirement Age (NRA) AND you plan to keep working, you have to be aware of the Social Security earned income penalty. Your Normal Retirement Age is the age that you are entitled to receive your full Social Security benefit, and it’s based on your date of birth.

The earned income penalty ONLY applies to taxpayers that turn on their Social Security prior to their normal retirement age. Once you have reached your normal retirement age, this penalty does not apply.

Basically, the IRS limits how much you are allowed to make each year if you elect to turn on your Social Security early. If you earn over those amounts, you may have to pay all or a portion of the Social Security benefit back to the government. Note that for married couples, the earned income numbers below apply to your personal earnings, and do not take into consideration your spouse’s income.

INCOME UNDER $23,400: If you earned income is below $23,400, no penalty, you get to keep your full social security benefit

INCOME OVER $23,400: You lose $1 of your social security benefit for every $2 you earn over the threshold. Example:

You turn on your social security at age 63

Your social security benefit is $20,000 per year

You make $40,000 per year in wages

Since you made $40,000 in wages, you are $16,600 over the $23,400 limit:

$16,600 x 50% ($1 reduction for every $2 earned) = $8,300 penalty.

The following year, your $20,000 Social Security benefit would be reduced by $8,300 for the assessment of the earned income penalty. Ouch!!

As a general rule of thumb, if you plan on working prior to your Social Security normal retirement age, and your wages will be in excess of the $23,400 limit, it usually makes sense to wait to turn on your Social Security benefit until your wages are below the threshold or you reach normal retirement age.

NOTE: You will see in the second row of the table “In the year of retirement”. In the year that you reach your full retirement age for social security the wage threshold is higher and the penalty is lower (a $1 penalty for every $3 over the threshold).

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

College Savings Account Options

To make it easy to compare and contrast each option, I will have a grading table at the beginning of each section that will provide you with some general information on each type of account, as well as my overall grade on the effectiveness of each college saving option.

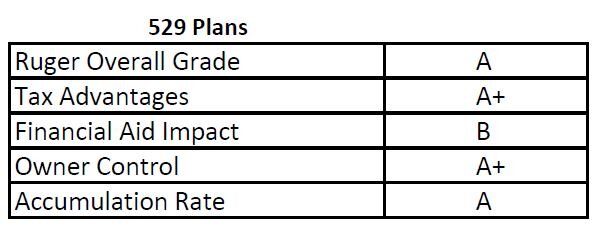

529 Plans

I’ll start with my favorite which are 529 College Savings Plan accounts. As a Financial Planner, I tend to favor 529 accounts as primary college savings vehicles due to the tax advantages associated with them. Many states offer state income tax deductions for contributions up to specific dollar amounts, so there is an immediate tax benefit. For example, New York provides a state tax deduction for up to $5,000 for single filers, and $10,000 for joint filers for contributions to NYS 529 accounts year. There is no income limitation for contributing to these accounts.

NOTE: Every now and then I come across individuals that have 529 accounts outside of their home state and they could be missing out on state tax deductions.

However, the bigger tax benefit is that fact that all of the investment returns generated by these accounts can be withdrawn tax free, as long as they are used for a qualified college expense. For example, if you deposit $5K into a 529 account when your child is 2 years old, and it grows to $15,000 by the time they go to college, and you use the account to pay qualified expenses, you do not pay tax on any of the $15,000 that is withdrawn. That is huge!! With many of the other college savings options like UTMA or brokerage accounts, you have to pay tax on the gains.

There is also a control advantage, in that the parent, grandparent, or whoever establishes the accounts has full control as to when and how much is distributed from the account. This is unlike UTMA / UGMA accounts, where once the child reaches a certain age, the child can do whatever they want with the account without the account owner’s consent.

A 529 account does count against the financial aid calculation, but it is a minimal impact in most cases. Since these accounts are typically owned by the parents, in the FAFSA formula, 5.6% of the balance would count against the financial aid reward. So, if you have a $50,000 balance in a 529 account, it would only set you back $2,800 per year in financial aid.

I gave these account an “A” for an accumulation rating because they have a lot of investment option available, and account owners can be as aggressive or conservative as they would like with these accounts. Many states also offer “age based portfolios” where the account is allocated based on the age of the child, and when the will turn 18. These portfolios automatically become more conservative as they get closer to the college start date.

The contributions limits to these accounts are also very high. Lifetime contributions can total $400,000 or more (depending on your state) per beneficiary.

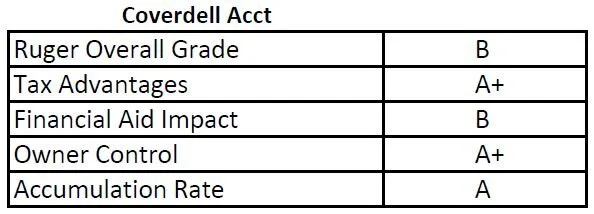

Coverdell Accounts (Education Savings Accounts)

Coverdell accounts have some of the benefits associated with 529 accounts, but there are contribution and income restrictions associated with these types of accounts. First, as of 2025, only taxpayers with adjusted gross income below $110,000 for single filers and $220,000 for joint filers are eligible to contribute to Coverdell accounts.

The other main limiting factor is the contribution limits. You are limited to a $2,000 maximum contribution each year until the beneficiary’s 18th birthday. Given the rising cost of college, it is difficult to accumulate enough in these accounts to reach the college savings goals for many families. Similar to 529 accounts, these accounts are counted as an asset of the parents for purposes of financial aid.

The one advantage these accounts have over 529 accounts is that the balance can be used without limitations for qualified expenses to an elementary or secondary public, private, or religious school. The federal rules recently changed for 529 accounts allowing these types of qualified withdrawal, but they are limited to $10,000 and depending on the state you live in, the state may not recognize these as qualified withdrawals from a 529 account.

If there is money left over in these Coverdell account, they also have to be liquidated by the time the beneficiary of the account turns age 30. 529 accounts do not have this restriction.

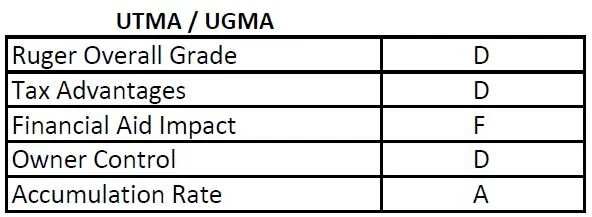

UTMA & UGMA Accounts

UGMA & UTMA accounts get the lowest overall grade from me. With these accounts, the child is technically the owner of the account. While the child is a minor, the parent is often assigned as the custodian of the account. But once the child reaches legal age, which can be 18, 19, or 21, depending on the state you live in, the child is then awarded full control over the account. This can be a problem when your child decides at age 18 that buying a Porsche is a better idea than spending that money on college tuition.

Also, because these accounts are technically owned by the child, they are a wrecking ball for the financial aid calculation. As I mentioned before, when it is an asset of the parent, 5.6% of the balance counts against financial aid, but when it is an asset of the child, 20% of the account balance counts against financial aid.

There are no special tax benefits associated with UTMA and UGMA accounts. No tax deductions for contributions and the child pays taxes on the gains.

Unlike 529 and Coverdell accounts, where you can change the beneficiary list on the account, with UTMA and UGMA accounts, the beneficiary named on the account cannot be changed.

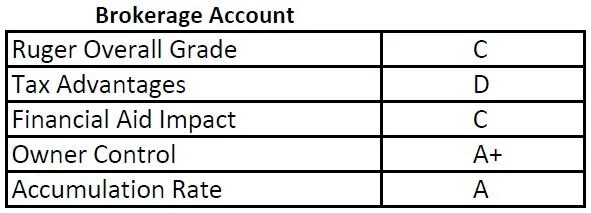

Brokerage Accounts

Parents can use brokerage accounts to accumulate money for college instead of the cash sitting in their checking account earning 0.25% per year. The disadvantage is the parents have to pay tax on all of the investment gains in the account once they liquidate them to pay for college. If the parents are in a higher tax bracket, they could lose up to 40%+ of those gains to taxes versus the 529 accounts where no taxes are paid on the appreciation. But, it also has the double whammy that if the parents realize capital gains from the liquidation, their income will be higher in the FAFSA calculation two years from now.

Sometimes, a brokerage account can complement a 529 account as part of a comprehensive college savings strategy. Many parents do not want to risk “over funding” a 529 account, so once the 529 accounts have hit a comfortable level, they will begin contributing the rest of the college savings to a brokerage account to maintain flexibility.

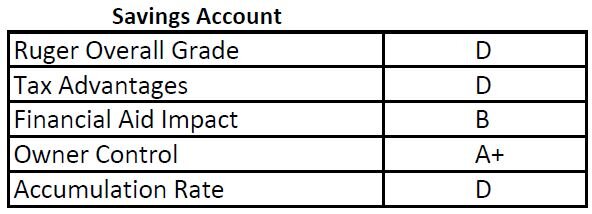

Savings Accounts

The pros and cons of a savings account owned by the parent or guardian of the child will have similar pros and cons of a brokerage account with one big drawback. Last I checked, most savings accounts were earning under 1% in interest. The cost of college since 1982 has increased by 6% per year (JP Morgan College Planning Essentials 2021). If the cost of college is going up by 6% per year, and your savings is only earning 1% per year, even though the balance in your savings account did not drop, you are losing ground to the tune of 5% PER YEAR. By having your college savings accounts invested in a 529, Coverdell, or brokerage account, it will at least provide you with the opportunity to keep pace with or exceed the inflation rate of college costs.

Can The Cost of College Keep Rising?

Let’s say the cost of attending college keeps rising at 6% per year, and you have a 2-year-old child that you want to send to state school which may cost $25,000 per year today. By the time they turn 18, it would cost $67,000 PER YEAR, times 4 years of college, which is $268,000 for a bachelor’s degree! The response I usually get when people hear these number is “there is no way that they can allow that to happen!!”. People were saying that 10 years ago, and guess what? It happened. This is what makes having a solid college savings strategy so important for your overall financial plan.

NOTE: As Financial Planners, we are seeing a lot more retirees carry mortgages and HELOC’s into retirement and the reason is usually “I helped the kids pay for college”.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Beware of Annuities

I’ll come right out and say “I’m not a fan of annuities”. They tend to carry:

1) Higher internal fees

2) Surrender charges that prevent investors from getting out of them

3) “Guarantees” that are inferior to alternative investment solutions

Unfortunately, annuities pay Financial Professionals a lot of money, which is why it is not uncommon for Investment Advisors to present them as a primary solution. For example, some annuities pay Investment Professionals 5% - 8% of the amount invested, so if you invest $200,000 in the annuity, the advisor gets paid $10,000 to $16,000 as soon as you deposit the money to the annuity. Compared to an Investment Advisor that may be charging you 1% per year to manage your portfolio, it will take them 5 to 8 years to earn that same amount.

To be fair, there are a few situations where I think annuities make sense, and I will share those with you in this article. In general, however, I think investors should be very cautious when they are presented with an annuity as a primary investment solution, and I will explain why.

Fixed Annuities & Variable Annuities

There are two different types of annuities. Fixed annuities and variable annuities. Within those categories, there are a lot of different flavors, such as indexed annuities, guaranteed income benefits, non-qualified, qualified, etc. Annuities are often issued by banks, investment firms, insurance companies, employer sponsored plan providers, or directly to the consumer. It is important to understand that not all annuities are the same and they can vary greatly from provider to provider. The points that I will be making in this article are my personal option based on my 20 years of experience in the investment industry.

Annuities Have High Fees

My biggest issue with annuities in general is the higher internal costs associated with them. When you read the fine print, annuities can carry:

· Commissions

· Contract fees

· Mortality expenses

· Surrender fees

· Rider fees

· Mutual fund expense ratios

· Penalties for surrender prior to age 59½

When you total all of those annual fees, it can sometimes be between 2% - 4% PER YEAR. The obvious questions is, “How is your money supposed to grow if the insurance company is assessing fees of 2% - 4% per year?”

Sub-Par Guarantees

The counter argument to this is that the insurance company is offering you “guarantees” in exchange for these higher fees. During the annuity presentation, the broker might say “if you invest in this annuity, you are guaranteed not to lose any money. It can only make money”. Who wouldn’t want that? But the gains in these annuities are often either capped each year, or get chipped away by the large internal fees associated with the annuity contract. So, even though you may not “lose money”, you may not be making as much as you could in a different investment solution.

Be The Insurance Company

At a high level, this is how insurance companies work. They sell you an annuity, then the insurance company turns around and invests your money, and hands you back a lower rate of return, often in the form of “guarantees”. That is how they stay in business. So, my question is “Why wouldn’t you just keep your money, invest it like the insurance would have, and you keep all of the gains”?

The answer: Fear. Most investments involve some level of risk, meaning you could lose money. Annuity presentations prey on this fear. They will usually show financial illustrations from recessions, such as when the market went down 30%, but the annuity lost no value. For retirees, this can be very appealing, because the working years are over and now they just have their life savings to last them for the rest of their lives.

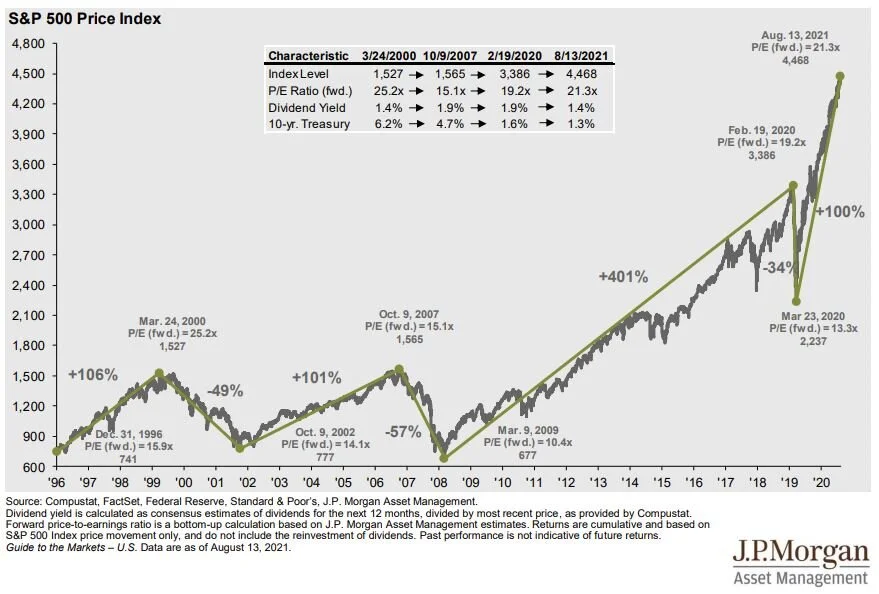

But like other successful investors, insurance companies rely on the historical returns of the stock market, which suggest that over longer periods of time (10+ year) the stock market tends to appreciate in value. See the charge of the S&P 500 Index below. Even with the pull backs and recessions, the value of the stock market has historically moved higher.

Annuity Surrender Fees Lock You In

The insurance company knows they are going to have your money for a long period of time because most annuities carry “surrender fees”. Most surrender schedules last 5 – 10 YEARS!! This means if you change your mind and want out of the annuity before the surrender period is up, the annuity company hits you with big fees. So, before you write the check to fund the annuity, make sure it’s 100% the right decision.

Do Not Invest an IRA In An Annuity

This situation always baffles me. We will come across investors that have an IRA invested in an annuity. Annuities by themselves have the advantage of being “tax deferred vehicles” meaning you do not pay taxes on the gains accumulated in the annuity until you make a withdrawal. You pay money to the insurance company to have that benefit since annuities are insurance products.

An IRA by itself is also a tax deferred account. You can choose to invest your IRA in whatever you want – cash, stocks, bonds, mutual funds, or an annuity. So, here is my question: since an IRA is already tax deferred vehicle, why would you pay extra fees to an annuity company to invest it in a tax deferred annuity? It makes no sense to me.

The answer, again, is usually fear. An individual retires, they meet with an investment advisor that recommends that they rollover their 401(k) into an IRA, and uses the fear of losing money in the market to convince them to move their full 401(k) into an annuity product. I completely understand the fear of losing money in retirement, and for some individuals it may make sense to put a portion of their retirement assets into something like an annuity that offers some guarantees. But in my experience, it rarely makes sense to invest the majority of your retirement assets in an annuity.

Guaranteed Minimum Income Benefits

Another sparkling gem associated with annuities that is often appealing to retirees are annuities that carry a GMIB, or “Guaranteed Minimum Income Benefit”. These annuities are usually designed to go up by a “guaranteed” 5% - 8% per year, and then at a set age will pay you a set monthly amount for the rest of your life. Now that sounds wonderful, but here is the catch that I want you to be aware of. For most annuity companies, the value of your annuity associated with the “guaranteed increases” only matters if you annuitize the contract with that insurance company. After 10 years, if instead you decided to surrender the annuity, you typically do not receive those big, guaranteed increases, but instead get the actual value of the underlying investments less the big fees. This is why there is often more than one “balance” illustrated on your annuity statement.

Here is the catch of the GMIB – when you go to turn it on, the annuity company decides what that fictitious GMIB balance will equal in the form of a monthly benefit for the rest of your life. Also, with some annuities, they cap the guaranteed increase after a set number of years. In general, what I have found is annuities that were issued with GMIB prior to 2008 tend to be fairly generous, because that was before the 2008/2009 recession. After 2008, the guarantees associated with these GMIB’s became less advantageous.

When Do Annuities Make Sense

I have given you the long list of reason why I am not a fan of annuities but there are a few situations where I think annuities can make sense:

1) Overspending protection

2) CD’s vs Fixed Annuity

Overspending Protection

When people retire, for the first time in their lives, they often have access to their 401(K), 403(b), or other retirement account. Having a large dollar amount sitting in accounts that you have full access to can sometimes be a temptation to overspend, make renovation to your house, go on big vacations, etc. But when you retire, when the money is gone, it is gone. For individuals that do not trust themselves to not spend through the money, turning that lump sum of money into a guaranteed money payment for the rest of their lives may be beneficial. In these cases, it may make sense for an individual to purchase an annuity with their retirement dollars, because it lowers the risk of them running out of money in retirement.

CD’s vs Fixed Annuities

For individuals that have a large cash reserve, and do not want to take any risk, sometimes annuity companies will offer attractive fixed annuity rates. For example, your bank may offer a 2 year CD at a 2%, but there may be an insurance company that will offer you a fixed annuity at a rate of 3.5% per year for 7 years. The obvious benefit is a higher interest rate each year. The downside is usually that the annuity carries surrender fees if you break the annuity before the maturity date. But if you don’t see any need to access the cash before the end of the surrender period, it may be worth collecting the higher interest rate.

Final Advice

Selecting the right investment vehicle is a very important decision. Before selecting an investment solution, it often makes sense to meet with a few different firms to listen to the approach of each advisor to determine which is the most appropriate for your financial situation. If you go into one of these meetings and an annuity is the only solution that is present, I would be very cautious about moving forward with that solution before you have vetted other options.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Paying Tax On Inheritance?

Not all assets are treated the same tax wise when you inherit them. It’s important to know what the tax rules are and the distribution options that are available to you as a beneficiary of an estate. In this video we will cover the tax treatment on inheriting a:

· House

· Retirements Accounts

· Stock & Mutual Funds

· Life Insurance

· Annuities

· Trust Assets

We will also cover the:

· Distribution options available to spouse and non-spouse beneficiaries of retirement accounts

· Federal Estate Tax Limits

· Biden’s Proposed Changes To The Estate Tax Rules

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

The Impact of Inflation on Stocks, Bonds, and Cash

The inflation fears are rising in the market and we are releasing this video to help you to better understand how inflation works and the impact that is has on stock, bonds, and cash.

The inflation fears are rising in the market and we are releasing this video to help you to better understand how inflation works and the impact that is has on stock, bonds, and cash. In this video we will go over:

· How inflation works

· Recent inflation trends that are spooking the markets

· Do we have to worry about hyperinflation like in the 80’s

· How stocks perform in inflationary environments

· The risk to bonds in inflationary environments

· How cash melts due to inflation

· The Feds reaction to inflation

· Inflation conspiracy theories that are building momentum

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.