The House Passed The Tax Bill. What's The Next Step?

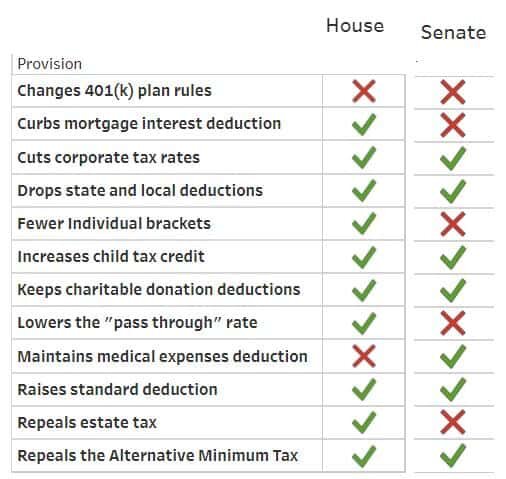

Last night the house passed the Tax Cut & Jobs Act Bill with ease. Next up is the Senate vote. It’s important to understand the House and the Senate are voting on two different tax reform bills. Below is a chart illustrating the main differences between the House version and the Senate version of the tax reform bill.

Last night the house passed the Tax Cut & Jobs Act Bill with ease. Next up is the Senate vote. It’s important to understand the House and the Senate are voting on two different tax reform bills. Below is a chart illustrating the main differences between the House version and the Senate version of the tax reform bill.

As you can see, there are a number of dramatic differences between the two bills. The easy part was getting the House to approve their version because the Republican Party own 239 of the 435 seats. In other words, they own 55% of the votes.

The Senate Vote

Next, the Senate will put their tax reform bill to a vote. The vote is expected to take place during the week of Thanksgiving. However, in the Senate , which the Republican have the majority, they only have 52 of the 100 seats. In this case, they would need at least 50 “Yes” votes to get the bill approved in the senate. It’s 50, not 51 votes, because in the event of a “tie”, the Vice President gets a vote to break the tie and he is likely to vote “Yes” to keep tax reform moving along.

Reconciliation Process

Once the House and Senate have approved their own separate tax bills, they will then have to begin the reconciliation process of blending the two bills together. This will be the difficult part. The two tax bills are dramatically different so there will be a fair amount of grappling between the House and the Senate committees as to which features stay and which features get tossed out or adjusted as part of the final tax bill. In the end, the final tax reform bill cannot add more than $1.5 Trillion to the national debt over the next 10 years. Otherwise, the bill would need to return to the Senate and would require “60” votes to approve the bill. There is a slim too no chance of that happening.

Tax Reform by Christmas

President Trump wants the bill on his desk to sign into law before Christmas. While it seems likely that the Senate will pass their tax bill next week, the battle will take place in the reconciliation process that will begin immediately after that vote. It’s a tall order to fill given that there are only six weeks left in the year and how different the two bills are in their current form. However, don’t underestimate how badly the Republican party wants to put a run on the scoreboard before the end of the year. If they get tax reform through in the last week of the year, it’s an understatement to say that it will be an intense final week of December for year-end tax planning. Stay tuned for more………

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Reform: Your Company May Voluntarily Terminate Your Retirement Plan

Make no mistake, your company retirement plan is at risk if the proposed tax reform is passed. But wait…..didn’t Trump tweet on October 23, 2017 that “there will be NO change to your 401(k)”? He did tweet that, however, while the tax reform might not directly alter the contribution limits to employer sponsored retirement plans, the new tax rates

Make no mistake, your company retirement plan is at risk if the proposed tax reform is passed. But wait…..didn’t Trump tweet on October 23, 2017 that “there will be NO change to your 401(k)”? He did tweet that, however, while the tax reform might not directly alter the contribution limits to employer sponsored retirement plans, the new tax rates will produce a “disincentive” for companies to sponsor and make employer contributions to their plans.

What Are Pre-Tax Contributions Worth?

Remember, the main incentive of making contributions to employer sponsored retirement plans is moving income that would have been taxed now at a higher tax rate into the retirement years, when for most individuals, their income will be lower and that income will be taxed at a lower rate. If you have a business owner or executive that is paying 45% in taxes on the upper end of the income, there is a large incentive for that business owner to sponsor a retirement plan. They can take that income off of the table now and then realize that income in retirement at a lower rate.

This situation also benefits the employees of these companies. Due to non-discrimination rules, if the owner or executives are receiving contributions from the company to their retirement accounts, the company is required to make employer contributions to the rest of the employees to pass testing. This is why safe harbor plans have become so popular in the 401(k) market.

But what happens if the tax reform is passed and the business owners tax rate drops from 45% to 25%? You would have to make the case that when the business owner retires 5+ years from now that their tax rate will be below 25%. That is a very difficult case to make.

An Incentive NOT To Contribute To Retirement Plans

This creates an incentive for business owners NOT to contribution to employer sponsored retirement plans. Just doing the simple math, it would make sense for the business owner to stop contributing to their company sponsored retirement plan, pay tax on the income at a lower rate, and then accumulate those assets in a taxable account. When they withdraw the money from that taxable account in retirement, they will realize most of that income as long term capital gains which are more favorable than ordinary income tax rates.

If the owner is not contributing to the plan, here are the questions they are going to ask themselves:

Why am I paying to sponsor this plan for the company if I’m not using it?

Why make an employer contribution to the plan if I don’t have to?

This does not just impact 401(k) plans. This impacts all employer sponsored retirement plans: Simple IRA’s, SEP IRA’s, Solo(k) Plans, Pension Plans, 457 Plans, etc.

Where Does That Leave Employees?

For these reasons, as soon as tax reform is passed, in a very short time period, you will most likely see companies terminate their retirement plans or at a minimum, lower or stop the employer contributions to the plan. That leaves the employees in a boat, in the middle of the ocean, without a paddle. Without a 401(k) plan, how are employees expected to save enough to retire? They would be forced to use IRA’s which have much lower contribution limits and IRA’s don’t have employer contributions.

Employees all over the United States will become the unintended victim of tax reform. While the tax reform may not specifically place limitations on 401(k) plans, I’m sure they are aware that just by lowering the corporate tax rate from 35% to 20% and allowing all pass through business income to be taxes at a flat 25% tax rate, the pre-tax contributions to retirement plans will automatically go down dramatically by creating an environment that deters high income earners from deferring income into retirement plans. This is a complete bomb in the making for the middle class.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Reform: At What Cost?

The Republicans are in a tough situation. There is a tremendous amount of pressure on them to get tax reform done by the end of the year. This type of pressure can have ugly side effects. It’s similar to the Hail Mary play at the end of a football game. Everyone, including the quarterback, has their eyes fixed on the end zone but nobody realizes that no

The Republicans are in a tough situation. There is a tremendous amount of pressure on them to get tax reform done by the end of the year. This type of pressure can have ugly side effects. It’s similar to the Hail Mary play at the end of a football game. Everyone, including the quarterback, has their eyes fixed on the end zone but nobody realizes that no one is covering one of the defensive lineman and he’s just waiting for the ball to be hiked. The game ends without the ball leaving the quarterback’s hands.

The Big Play

Tax reform is the big play. If it works, it could lead to an extension of the current economic rally and more. I’m a supporter of tax reform for the purpose of accelerating job growth both now and in the future. It’s not just about U.S. companies keeping jobs in the U.S. That has been the game for the past two decades. The new game is about attracting foreign companies to set up shop in the U.S. and then hire U.S. workers to run their plants, companies, subsidiaries, etc. Right now we have the highest corporate tax rate in the world which has not only prevented foreign companies from coming here but it has also caused U.S. companies to move jobs outside of the United States. If everyone wants more pie, you have to focus on making the pie bigger, otherwise we are all just going to sit around and fight over who’s piece is bigger.

Easier Said Than Done

How do we make the pie bigger? We have to lower the corporate tax rate which will entice foreign companies to come here to produce the goods and services that they are already selling in the U.S. Which is easy to do if the government has a big piggy bank of money to help offset the tax revenue that will be lost in the short term from these tax cuts. But we don’t.

$1.5 Trillion In Debt Approved

Tax reform made some headway in mid-October when the Senate passed the budget. Within that budget was a provision that would allow the national debt to increase by approximately $1.5 trillion dollars to help offset the short-term revenue loss cause by tax reform. While $1.5 trillion sounds like a lot of money, and don’t get me wrong, it is, let’s put that number in context with some of the proposals that are baked into the proposed tax reform.

Pass-Through Entities

One of the provisions in the proposed tax reform is that income from “pass-through” businesses would be taxed at a flat rate of 25%.

A little background on pass-through business income: sole proprietorships, S corporations, limited liability companies (LLCs), and partnerships are known as pass-through businesses. These entities are called pass-throughs, because the profits of these firms are passed directly through the business to the owners and are taxed on the owners’ individual income tax returns.

How many businesses in the U.S. are pass-through entities? The Tax Foundation states on its website that pass-through entities “make up the vast majority of businesses and more than 60 percent of net business income in America. In addition, pass-through businesses account for more than half of the private sector workforce and 37 percent of total private sector payroll.”

At a conference in D.C., the American Society of Pension Professionals and Actuaries (ASPPA), estimated that the “pass through 25% flat tax rate” will cost the government $6 trillion - $7 trillion in tax revenue. That is a far cry from the $1.5 trillion that was approved in the budget and remember that is just one of the many proposed tax cuts in the tax reform package.

Are Democrats Needed To Pass Tax Reform?

Since $1.5 trillion was approved in the budget by the senate, if the proposed tax reform is able to prove that it will add $1.5 trillion or less to the national debt, the Republicans can get tax reform passed through a “reconciliation package” which does not require any Democrats to step across the aisle. If the tax reform forecasts exceed that $1.5 trillion threshold, then they would need support from a handful of Democrats to get the tax reformed passed which is unlikely.

Revenue Hunting

To stay below that $1.5 trillion threshold, the Republicans are “revenue hunting”. For example, if the proposed tax reform package is expected to cost $5 trillion, they would need to find $3.5 trillion in new sources of tax revenue to get the net cost below the $1.5 trillion debt limit.

State & Local Tax Deductions – Gone?

One for those new revenue sources that is included in the tax reform is taking away the ability to deduct state and local income taxes. This provision has created a divide among Republicans. Since many southern states do not have state income tax, many Republicans representing southern states support this provision. Visa versa, Republicans representing states from the northeast are generally opposed to this provision since many of their states have high state and local incomes taxes. There are other provisions within the proposed tax reform that create the same “it depends on where you live” battle ground within the Republican party.

Obamacare

One of the main reasons why the Trump administration pushed so hard for the Repeal and Replace of Obamacare was “revenue hunting”. They needed the tax savings from the repeal and replace of Obamacare to carrry over to fill the hole that will be created by the proposed tax reform. Since that did not happen, they are now looking high and low for other revenue sources.

Retirement Accounts At Risk?

If the Republicans fail to get tax reform through they run the risk of losing face with their supporters since they have yet to get any of the major reforms through that they campaigned on. Tax reform was supposed to be a layup, not a Hail Mary and this is where the hazard lies. Republicans, out of the desperation to get tax reform through, may start making cuts where they shouldn’t. There are rumors that the Republican Party may consider making cuts to the 401(k) contribution limits and employers sponsored retirement plan. Even though Trump tweeted on October 23, 2017 that he would not touch 401(k)’s as part of tax reform, they are running out of the options for other places that they can find new sources of tax revenue. If it comes down to the 1 yard line and they have the make the decision between making deep cuts to 401(k) plans or passing the tax reform, retirement plans may end up being the sacrificial lamb. There are other consequences that retirement plans may face if the proposed tax reform is passed but it’s too broad to get into in this article. We will write a separate article on that topic.

Tax Reform May Be Delayed

Given all the variables in the mix, passing tax reform before December 31st is starting to look like a tall order to fill. If the Republicans are looking for new sources of revenue, they should probably look for sources that are uniform across state lines otherwise they risk splintering the Republican Party like we saw during the attempt to Repeal and Replace Obamacare. We are encouraging everyone to pay attention to the details buried in the tax reform. While I support tax reform to secure the country’s place in the world both now and in the future, if provisions that make up the tax reform are rushed just to get something done, we run the risk of repeating the short lived glory that tax reform saw during the Reagan Era. They passed sweeping tax cuts, the deficits spiked, and they were forced to raise tax rates a few years later.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Who Pays The Tax On A Cash Gift?

This question comes up a lot when a parent makes a cash gift to a child or when a grandparent gifts to a grandchild. When you make a cash gift to someone else, who pays the tax on that gift? The short answer is “typically no one does”. Each individual has a federal “lifetime gift tax exclusion” of $5,400,000 which means that I would have to give

This question comes up a lot when a parent makes a cash gift to a child or when a grandparent gifts to a grandchild. When you make a cash gift to someone else, who pays the tax on that gift? The short answer is “typically no one does”. Each individual has a federal “lifetime gift tax exclusion” of $13,990,000 which means that I would have to give away $13.99 million dollars before I would owe “gift tax” on a gift. For married couples, they each have a $13.99 million dollar exclusion so they would have to gift away $27.98M before they would owe any gift tax. When a gift is made, the person making the gift does not pay tax and the person receiving the gift does not pay tax below those lifetime thresholds.

“But I thought you could only gift $19,000 per year per person?” The $19,000 per year amount is the IRS “gift exclusion amount” not the “limit”. You can gift $19,000 per year to any number of people and it will not count toward your $13.99M lifetime exclusion amount. A married couple can gift $38,000 per year to any one person and it will not count toward their $27.98 million lifetime exclusion. If you do not plan on making gifts above your lifetime threshold amount you do not have to worry about anyone paying taxes on your cash gifts.

Let’s look at an example. I’m married and I decide to gift $20,000 to each of my three children. When I make that gift of $60,000 ($20K x 3) I do not owe tax on that gift and my kids do not owe tax on the gift. Also, that $60,000 does not count toward my lifetime exclusion amount because it’s under the $38,000 annual exclusion for a married couple to each child.

In the next example, I’m single and I gift $1,000,000 my neighbor. I do not owe tax on that gift and my neighbor does not owe any tax on the gift because it is below my $13.99M threshold. However, since I made a gift to one person in excess of my $19,000 annual exclusion, I do have to file a gift tax return when I file my taxes that year acknowledging that I made a gift $981,000 in excess of my annual exclusion. This is how the IRS tracks the gift amounts that count against my $13.99M lifetime exclusion.

Important note: This article speaks to the federal tax liability on gifts. If you live in a state that has state income tax, your state’s gift tax exclusion limits may vary from the federal limits.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Secret: R&D Tax Credits…You May Qualify

When you think of Research and Development (R&D) many people envision a chemistry lab or a high tech robotics company. It’s because of this thinking that millions of dollars of available tax credits for R&D go unused every year. R&D exists in virtually every industry and business owners need to start thinking about R&D in a different light because

When you think of Research and Development (R&D) many people envision a chemistry lab or a high tech robotics company. It’s because of this thinking that millions of dollars of available tax credits for R&D go unused every year. R&D exists in virtually every industry and business owners need to start thinking about R&D in a different light because there could be huge tax savings waiting for them.

Most companies don't realize that they qualify

Road paving companies, manufactures, a meatball company, software firms, and architecture firms are just a few examples of companies that have met the criteria to qualify for these lucrative tax credits.

Think of R&D as a unique process within your company that you may be using throughout the course of your everyday business that is specific to your competitive advantage. The purpose of these credits is to encourage companies to be innovative with the end goal of keeping more jobs here in the U.S. If you have an engineers on your staff, whether software engineers, design engineers, mechanical engineers there is a very good chance that these tax credits may be available to you. The R&D tax credits also allow you to look back to all open tax years so for companies that discover this for the first time, the upside can be huge. Tax years typically stay open for three years.

Accountants may not be aware of these credits

One of the main questions we get from business owners is “Shouldn’t my accountant have told me about this?” Many accounting firms are unaware of these tax credits and the process for qualifying which is why there are specialty consulting firms that work with companies to determine whether or not they are eligible for the credit. Some of our clients have worked with these firms and the company only pays the consulting firm if you qualify for the tax credits. Kind of a win-win situation.

We recently attended a seminar that was sponsored by Alliantgroup out of New York City and on their website it listed the following description of companies that qualify for these credits:“

Any company that designs, develops, or improves products, processes, techniques, formulas, inventions, or software may be eligible. In fact, if a company has simply invested time, money, and resources toward the advancement and improvement of its products and processes, it may qualify”.

We love helping our clients save taxes and in this case, like many others, we were looking at R&D in a different light.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Avoid These 1099 “Employee” Pitfalls

As financial planners we are seeing more and more individuals, especially in the software development and technology space, hired by companies as “1099 employees”. “1099 employees” is an ironic statement because if a company is paying you via a 1099 technically you are not an “employee” you are a self-employed sub-contractor. It’s like having

As financial planners we are seeing more and more individuals, especially in the software development and technology space, hired by companies as “1099 employees”. “1099 employees” is an ironic statement because if a company is paying you via a 1099 technically you are not an “employee” you are a self-employed sub-contractor. It’s like having your own separate company and the company that you work for is your “client”.

There are advantages to the employer to pay you as a 1099 sub-contractor as opposed to a W2 employee. When you are a W2 employee they may have to provide you with health benefits, the company has to pay payroll taxes on your wages, there may be paid time off, you may qualify for unemployment benefits if you are fired, eligibility for retirement plans, they have to put you on payroll, pay works compensation insurance, and more. Basically companies have a lot of expenses associated with you being a W2 employee that does not show up in your paycheck.

To avoid all of these added expenses the employer may decide to pay you as a 1099 “employee”. Remember, if you are a 1099 employee you are “self-employed”. Here are the most common mistakes that we see new 1099 employees make:

Making estimated tax payments throughout the year

This is the most common error. When you are a W2 employee, it’s the responsibility of the employer to withhold federal and state income tax from your paycheck. When you are a 1099 sub-contractor, you are not an employee, so they do not withhold taxes from your compensation…………that is now YOUR RESPONSIBILITY. Most 1099 individuals have to make what is called “estimated tax payments” four times a year which are based on either your estimated income for the year or 110% of the previous year’s income. Best advice……..if 1099 income is new for you, setup a consultation with an accountant. They will walk you through tax withholding requirements, tax deductions, tax filing forms, etc. It’s very difficult to get everything right using Turbo Tax when you are a self-employed individual.

Tracking mileage and expenses throughout the year

Since you are self-employed you need to keep track of your expenses including mileage which can be used as deductions against your income when you file your tax return. Again, we recommend that you meet with a tax professional to determine what you do and do not need to track throughout the year.

The tax return is prepared incorrectly

No one wants a love letter from the IRS. Those letters usually come with taxes due, penalties, and a “guilty until proven innocent” approach. There may be additional “schedules” that you need to file with your tax return now that you are self-employed. The tax schedules detail your self-employment income, deductions, estimated tax payments, and other material items.

Important rule, do not cut corners by reducing the gross amount of your 1099 income. This is a big red flag that is easy for the IRS to catch. The company that issued the 1099 to you usually reports that 1099 payment to the IRS with your social security number or the Tax ID number of your self-employment entity. The IRS through an automated system can run your social security number or tax ID to cross check the 1099 payment and 1099 income to make sure it was reported.

Legal protection

As a 1099 sub-contractor, you have to consider the liability that could arise from the services that you are providing to your “client” (your employer). As a self-employed individual, the company that you “work for” could sue you for any number of reasons and if you are operating the business under your social security number (which most are) your personal assets could be at risk if a lawsuit arises. Advice, talk to an attorney that is knowledgeable in business law to discuss whether or not setting up a corporate entity makes sense for your self-employment income to better protect yourself.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Secret: Spousal IRAs

Spousal IRA’s are one of the top tax tricks used by financial planners to help married couples reduce their tax bill. Here is how it works:

Spousal IRA’s are one of the top tax tricks used by financial planners to help married couples reduce their tax bill. Here is how it works:

In most cases you need “earned income” to be eligible to make a contribution to an Individual Retirement Account (“IRA”). The contribution limits for 2025 is the lesser of 100% of your AGI or $7,000 for individuals under the age of 50. If you are age 50 or older, you are eligible for the $1,000 catch-up making your limit $8,000.

There is an exception for “Spousal IRAs,” and there are two cases where this strategy works very well.

Case 1: One spouse works and the other spouse does not. The employed spouse is currently maxing out their contributions to their employer-sponsored retirement plan, and they are looking for other ways to reduce their income tax liability.

If the AGI (adjusted gross income) for that couple is below $236,000 in 2025, the employed spouse can make a contribution to a Spousal Traditional IRA up to the $7,000/$8,000 limit even though their spouse had no “earned income”. It should also be noted that a contribution can be made to either a Traditional IRA or Roth IRA but the contributions to the Roth IRA do not reduce the tax liability because they are made with after tax dollars.

Case 2: One spouse is over the age of 70 ½ and still working (part-time or full-time) while the other spouse is retired. IRA rules state that once you are age 70½ or older, you can no longer make contributions to a traditional IRA. However, if you are age 70½ or older BUT your spouse is under the age of 70½, you still can make a pre-tax contribution to a traditional IRA for your spouse.

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Changes to 2016 Tax Filing Deadlines

In 2015, a bill was passed that changed tax filing deadlines for certain IRS forms that will impact a lot of filers. Not only is it important to know the changes so you can prepare and file your return timely but to understand why the changes were made.

In 2015, a bill was passed that changed tax filing deadlines for certain IRS forms that will impact a lot of filers. Not only is it important to know the changes so you can prepare and file your return timely but to understand why the changes were made.

Summary of Changes

IRS Form Business Type Previous Deadline New Deadline

1065 Partnership April 15 March 15

1120C Corporation March 15 April 15

NOTE: The dates in the chart above are for companies with years ending 12/31. If a company has a different fiscal year, Partnerships will now file by the 15th day of the third month following year end and C Corporations will now file by the 15th day of the fourth month following year end.

Why the Changes?

The most practical reason for the change to filing deadlines is that individuals with partnership interests will now have a better opportunity to file their individual returns (Form 1040) without extending. Form K-1 provides information related to the activity of a Partnership at the level of each individual partner. For example, if I own 50% of a Partnership, my K-1 would show 50% of the income (or loss) generated, certain deductions, and any other activity needed for me to file my Form 1040. The issue with the previous Partnership return deadline of April 15th is that it coincided with the individual deadline. This resulted in partners of the company not receiving their K-1’s with sufficient time to file their personal return by April 15th. With Partnerships now having a deadline of March 15th, this will give individuals a month to receive their K-1 and file their personal return without having to extend.

The deadline for Form 1120, which is filed by C Corporations, was also changed with this bill. Where the Form 1065 deadline was cut back by a month, the Form 1120 was extended a month. C Corporations, for tax purposes, are treated similar to individuals whereas they pay taxes directly when they file their return. Partnerships are not taxed directly, rather the income or loss is passed through to each individual partner who recognizes the tax ramifications on their personal return. For this reason, the deadline for Form 1120 being extended a month has little impact, if any, on individuals. The change gives C Corporations more time to file without having to extend the return.

S Corporations are another common business type. The deadlines for S Corporation returns (Form 1120S) were not changed with this bill. S Corporations are similar to Partnerships in that K-1’s are distributed to owners and the income or loss generated is passed through to the individuals return. That being said, Form 1120S already has a due date of March 15th, the same as the new Partnership deadline.

Extension Deadlines

IRS Form Business Type Deadline

1040 Individual October 15

1065 Partnership September 15

1120 C Corporation September 15

1120S S Corporation September 15

Extension deadlines were not immediately changed with the passing of the bill. Although Partnerships previously had the same filing deadline as individuals, the deadline with the filing of an extension was a month before. This was necessary because if a Partnership did not have to file an extended return until October 15th, individuals with partnership interests wouldn’t have a choice but to file delinquent.

The one change to the extension chart above set to take place in 2026 is the C Corporation extension being changed to October 15th.

Summary

Overall, the changes appear to have improved the filing calendar. This may be a big adjustment for Partnerships that are used to the April 15th deadline as they will have one less month to get organized and file. For this reason, you may see an increase in 2016 Partnership extensions.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.