How Do Single(k) Plans Work?

A Single(k) plan is an employer sponsored retirement plan for owner only entities, meaning you have no full-time employees. These owner only entities get the benefits of having a full fledge 401(k) plan without the large administrative costs associated with traditional 401(k) plans.

What is a Single(k) Plan?

A Single(k) plan is an employer-sponsored retirement plan for owner-only entities, meaning you have no full-time employees. These owner-only entities get the benefits of having a full-fledged 401(k) plan without the large administrative costs associated with traditional 401(k) plans.

What is the definition of a “full-time” employee?

Oftentimes, a small company will have some part-time staff. It does not matter whether you consider them “part-time”, the definition of full-time employee is defined by the IRS as working 1000 hours in a 12-month period. If you have a “full-time” employee, you would not be eligible to sponsor a Single(k) plan.

Types of Contributions

There are two types of contributions to these plans: Employee deferral contributions and employer profit-sharing contributions. The employee deferral piece works like a 401(k) plan. If you are under the age of 50 you can contribute $24,500 in 2026 in employee deferrals. If you are 50-59 or 64 or older, you get the $8,000 catch-up contribution so you can contribute $32,500 in employee deferrals. Beginning in 2026, if you are age 60-63, instead of the $8,000 catch-up, you can contribute an additional $11,250 for a total of $35,750 in employee deferrals.

The reason why these plans are a little different than other employer-sponsored plans is the employee deferral piece allows you to put 100% of your compensation into these plans up to those dollar thresholds.

In addition to the employee deferrals, you can also contribute 20% of your net earned income in the form of a profit-sharing contribution. For example, if you make $100,000 in net earned income from self-employment and you are age 53, you could contribute $32,500 in employee deferrals and then you could contribute an additional $20,000 in the form of a profit-sharing contribution. Making your total pre-tax contribution $52,500.

Establishment Deadline

The deadline for establishing a Solo(k) plan varies based on how the business is incorporated. If the business is an S-Corp or multi-member partnership, the business owner(s) must have the Solo(k) plan setup by December 31st. If the business is a sole proprietor or single member LLC, the Solo(k) plan can be setup by the tax filing deadline plus extension.

Loans & Roth Deferrals

Single(k) plans provide all of the benefits to the owner of a full 401(k) plan at a fraction of the cost. You can set up the plan to allow 401(k) loan and Roth deferral contributions.

SEP IRA vs Single(k) Plans

A lot of small business owners find themselves in a position where they are trying to decide between setting up a SEP IRA or a Single(k) plan. One of the big factors, that is often times the deciding factor, is how much the owner intends to contribute to the plan. The SEP IRA limits the business owner to just the 20% of net earned income. Whereas the Single(k) plan allows the 20% of net earned income plus the employee deferral contribution amount. However, if 20% of your net earned income would satisfy your target amount then the SEP IRA may be the right choice.

Advanced Strategy Using A Single(k) Plan

Here is a great tax strategy if you have one spouse that is the primary breadwinner bringing in most of the income and the other has self-employment income for a side business. If the spouse with the self-employment income is over the age of 50 and makes $20,000 in net earned income, they could set up a Single(k) Plan and defer the full $20,000 into their Single(k) plan as employee deferrals. If they had a SEP IRA, the max contribution would have been $4,000.

A huge tax savings for a married couple that is looking to lower their tax liability.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Last updated June, 2026

Strategies to Save for Retirement with No Company Retirement Plan

The question, “How much do I need to retire?” has become a concern across generations rather than something that only those approaching retirement focus on. We wrote the article, How Much Money Do I Need To Save To Retire?, to help individuals answer this question. This article is meant to help create a strategy to reach that number. More

The question, “How much do I need to retire?” has become a concern across generations rather than something that only those approaching retirement focus on. But what if you, or in the case of married couples, your spouse, are not covered by an employer-sponsored retirement plan? In this article we are going to cover retirement savings strategies for individuals that may not be covered by an employer-sponsored retirement plan.

Married Filing Jointly - One Spouse Covered by Employer Sponsored Plan and is Not Maxing Out

A common strategy we use for clients when a covered spouse is not maxing out their deferrals is to increase the deferrals in the retirement plan and supplement income with the non-covered spouse’s salary. The limits for 401(k) deferrals in 2026 is $24,500 for individuals under 50, $32,500 for individuals 50-59 and 64+ and $35,750 for individuals 60-63. For example, if I am covered and only contribute $8,000 per year to my account and my spouse is not covered but has additional money to save for retirement, I could increase my deferrals up to the plan limits using the amount of additional money we have to save. This strategy is helpful as it allows for easier tracking of retirement accounts and the money is automatically deducted from payroll. Also, if you are contributing pre-tax dollars, this will decrease your tax liability.

Note: Payroll deferrals must be withheld from payroll by 12/31. If you owe money when you file your taxes in April, you would not be able to go back and increase your deferrals in your company plan for that tax year.

Married Filing Jointly - One Spouse Covered by Employer Sponsored Plan and is Maxing Out

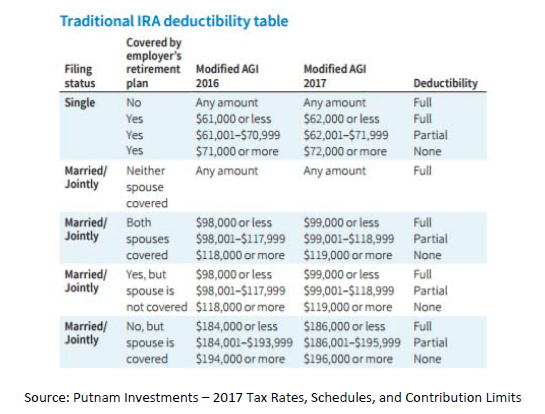

If the covered spouse is maxing out at the high limits already, you may be able to save additional pre-tax dollars depending on your Adjusted Gross Income (AGI).

Below is the Traditional IRA Deductibility Table for 2026. This table shows how much individuals or married couples can earn and still deduct IRA contributions from their taxable income.

As shown in the chart, if you are married filing jointly and one spouse is covered, the couple can fully deduct IRA contributions to an account in the covered spouses name if AGI is less than $126,000 and can fully deduct IRA contributions to an account in the non-covered spouses name if AGI is less than $236,000. The Traditional IRA limits for 2026 are $7,500 if under 50 and $8,600 if 50+. These lower limits and income thresholds make contributing to company sponsor plans more attractive in most cases.

Single or Married Filing Jointly and Neither Spouse is Covered

If you (and your spouse if married filing joint) are not covered by an employer sponsored plan, you do not have an income threshold for contributing pre-tax dollars to a Traditional IRA. The only limitations you have relate to the amount you can contribute. These contribution limits for both Traditional and Roth IRA’s are $7,500 if under 50 and $8,600 if 50+. If married filing joint, each spouse can contribute up to these limits.

Unlike employer sponsored plans, your contributions to IRA’s can be made after 12/31 of that tax year as long as the contributions are in before you file your tax return.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Last updated June, 2026

How Much Money Do I Need To Save To Retire?

This is by far the most popular question that we come across as financial planners. You may have heard some of the "rules of thumb" like “80% of your current take-home pay” or “1 million dollars”. In reality, the answer varies greatly on an individual by individual basis. This article will outline the procedures that we follow as financial planners to help

poc

This is by far the most popular question that we come across as financial planners. You may have heard some of the "rules of thumb" like “80% of your current take-home pay” or “1 million dollars”. In reality, the answer varies greatly on an individual by individual basis. This article will outline the procedures that we follow as financial planners to help individuals answer this very important question.

Step 1: Estimate Your Annual Expenses In Retirement

The first step is to get a ballpark idea of what your annual expenses might look like in retirement. The best place to start is to list your current monthly and annual expenses. Then create a separate column labeled “expenses in retirement”. Whether you are 2 years, 10 years, or 20 years away from retirement the idea is to pretend as if you were retiring tomorrow and determining what your annual expenses might look like. Some of your expenses in retirement will be lower, others may be higher, but most people find that a lot of their current expenses will carry over at the same level into the retirement years. This is because most people have become accustom to a certain standards of living and they intend to maintain that standard of living in retirement. Here are a few important questions that you should ask yourself when forecasting your retirement expenses:

How much should I budget for health insurance?

Will I have a mortgage or debt when I retire?

Do I plan to move when I retire?

Since I will not be working, should I budget additional expenses for vacations and hobbies?

Will I need to keep my life insurance policies after I retire?

Step 2: Adjust Your Retirement Expenses For Inflation

Now that you have a ballpark number of your annual expenses in retirement, you will need to adjust those expenses for inflation. Inflation is just a fancy word for “the price of everything that we buy today will gradually go up in price over time”. If the price of a gallon of milk today is $2 then most likely 20 years from now that same gallon of milk will cost $3.51. A 75% increase!! Historically inflation has grown at a rate of about 3% per year. There are periods of time when the rate of inflation grows faster or slower but on average it grows at 3% per year.

Another way to look at inflation is $20,000 in today’s dollars will not buy the same amount of goods and services 10 years from now because inflation erodes the purchasing power of your $20,000. If I did my annual expense planner and it tells me that I need $50,000 per year in retirement to meet all of my estimated expenses, let’s look at what adjusting that $50,000 for inflation does over different periods of time assuming a 3% rate of inflation:

Today’s Dollars 5 Years From Now 10 Years From Now 20 Years From Now

$50,000 $56,275 $65,238 $87,675

In the above example, if I am retiring in 10 years, and my estimated annual expenses in retirement will be $50,000 in today’s dollars, by the time I retire 10 years from now my annual expenses will increase to $65,238 per year just to stay in the same place that I am in today. Also, inflation does not stop when you retire, it continues into the retirement years. If I am 50 today and plan to live until 90, I have to apply this inflation adjustment for 40 years. It’s clear to see how inflation can have a significant impact on the amount that you may need to withdrawal for your account to meet you estimated expenses at a future date.

Step 3: Gather The Information On Your Current Assets

Once you know your expenses, you now need to gather all of the information on your retirement accounts and pension plans. You should collect the most recent statement for all of your investment accounts (401K, 403B, IRA’s, brokerage accounts, stocks, etc.), pension statements (if applicable), obtain your most recent social security statement, and gather information on the other sources of income and/or assets that may be available when you retire. Such as:

Sale of a business

Downsizing the primary residence

Rental income

Part-time employment

Step 4: Project The Growth Of Your Retirement Assets

There are three main categories to consider when calculating the growth rate of your retirement assets:

Annual contributions

Withdrawals

Investment rate of return

For annual contributions, it’s determining which accounts you plan on making deposits too each year and how much? For most individuals, their employer sponsored retirement plan is the main source of new contributions to their retirement nest egg. If your employer makes regular employer contributions to your retirement plan, you should factor those in as well. For example, if I am contributing 8% of my pay into the plan and my employer is providing me with a 4% matching contributions, I would reasonably assume that I’m adding 12% of my pay to my 401(k) plan each year.

The most popular question that we get in this category is “how much should I be contributing each year to my retirement account with my employer?” We advise employees that they should have a goal of contributing 10% of their pay each year to their retirement accounts. This is an aggregate total between your personal contributions and the employer contributions. Even if you cannot reach that level right now, 10%+ is the target.

Let’s move onto the next category…….withdrawals. Pre-retirement withdrawals from retirement accounts have become much more common in recent years due largely to the rising cost of college education. Parents will take loans from their 401K/403B plans or take early withdrawals from IRA accounts to fulfill the need for additional income during the years that their children are in college. If part of your overall financial plan is to use your retirement accounts to pay for one-time expenses such as college, you will need to factor that into your projections.

The third variable to consider when determining the growth of your assets is the assumed annual rate of return on your investments. There are many items to consider when determining a reasonable annual rate of return for your accounts. Some of those considerations include:

Time horizon to retirement

Allocation of your portfolio (stocks vs bonds)

Concentrated holdings (10%+ of your portfolio allocated to a single investment)

Accumulation phase versus distribution phase

The answer to the question: “what rate of return should I expect from my retirement accounts?”, can really only be determine on a case by case basis. Using an unreasonable rate of return assumption can create a significant disconnect between your retirement projections versus what is likely to actually occur within your investment accounts. Be careful with this step.

Step 5: Factor In Taxes

Don’t forget about the lovely IRS. All assets are not treated equally from a tax standpoint. For most individuals, the majority of their retirement savings will be in pre-tax retirement vehicles such as 401(k), 403(b), and Traditional IRA’s. That means when you take distributions from those accounts, you will realize earned income, and have to pay tax. For example, if you have $400,000 in your 401K account and you are in the 25% tax bracket, $100,000 of that $400,000 will be lost to taxes as withdrawals are made from the account.

If you have after tax investment accounts, it’s possible that you may owe little to no taxes on withdrawals. However, if there are unrealized investment gains built up in your after tax investment accounts then you may owe capital gains tax when liquidating positons.

Also note, you may have to pay taxes on a portion of your social security benefit. The amount of your social security benefit that is taxable varies based on your level of income.

Step 6: Spend Down Your Assets

In the final step, you should run long term projections to illustrate the spend down of your assets in retirement. Here are the steps:Example

Start with your annual after tax expense number $60,000

Subtract social security less taxes: ($20,000)

Subtract pension payments less taxes (if applicable): ($10,000)

Annual Expenses Net SS and Pensions: $30,000

In the example above, this individual would need an additional $30,000 after-tax to meet their anticipated annual expenses in Year 1 of retirement. I stress “after-tax” because if all of the retirement assets are in a pre-tax retirement account then they would need to gross up their distributions for taxes to get to the $30,000 after tax. If it is assumed that $40,000 has to be withdrawn from an IRA each year, the 3% inflation rate is applied to the annual expenses, and the life expectancy of this individual is 20 years from the date that they retire, this individual would need to withdrawal $1,074,814 out of their retirement accounts over the next 20 years to meet their income needs.

Step 7: Identify Multiple Solutions

There are often times multiple roads to reach a destination and the same is true when planning for retirement. If you find that you assets are falling short of the amount that is needed to sustain your expenses in retirement, you should work with a knowledgeable financial planner to identify alternative solutions. It may help you to answer questions like:

If I decided to work part-time in retirement how much would I have to earn?

If I downsize my primary residence in retirement how does this impact the overall picture?

If I can’t retire at age 63, what age can I comfortably retire at?

What are the pros and cons of taking social security benefits prior to normal retirement age

I also encourage clients to spend time looking at their annual expenses. If you find that your are cutting it close on income versus expenses in retirement, it's usually easier to cut expenses than it is to create more income in the retirement year.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Sample Business Plan

The business plan for a startup business provides entrepreneurs with a guide in creating a business plan and items to consider when starting a new business.

Sample Business Plan

The business plan for a startup business provides entrepreneurs with a guide in creating a business plan and items to consider when starting a new business.

Click on the PDF link in the green box below.

Should I Establish an Employer Sponsored Retirement Plan?

Employer sponsored retirement plans are typically the single most valuable tool for business owners when attempting to:

Reduce their current tax liability

Attract and retain employees

Accumulate wealth for retirement

establishing an employer sponsored retirement plan

Employer-sponsored retirement plans are typically the single most valuable tool for business owners when attempting to:

Reduce their current tax liability

Attract and retain employees

Accumulate wealth for retirement

But with all of the different types of plans to choose from, which one is the right one for your business? Most business owners are familiar with how 401(k) plans work, but that might not be the right fit given variables such as:

# of Employees

Cash flows of the business

Goals of the business owner

There are four main stream employer-sponsored retirement plans that business owners have to choose from:

SEP IRA

Single(k) Plan

Simple IRA

401(k) Plan

Since there are a lot of differences between these four types of plans, we have included a comparison chart at the conclusion of this newsletter, but we will touch on the highlights of each type of plan.

SEP IRA PLAN

This is the only employer-sponsored retirement plan that can be set up after 12/31 for the previous tax year. So, when you are sitting with your accountant in the spring and they deliver the bad news that you are going to have a big tax liability for the previous tax year, you can establish a SEP IRA up until your tax filing deadline plus extension, fund it, and take a deduction for that year.

However, if the company has employees who meet the plan's eligibility requirement, these plans become very expensive very quickly if the owner(s) want to make contributions to their own accounts. The reason is that these plans are 100% employer-funded, which means there are no employee contributions allowed, and the employer contribution is uniform for all plan participants. For example, if the owner contributes 15% of their income to the SEP IRA, they have to make an employer contribution equal to 15% of compensation for each employee who has met the plan's eligibility requirement. If the 5305-SEP Form, which serves as the plan document, is set up correctly, a company can keep new employees out of the plan for up to 3 years, but often it is either not set up correctly or the employer cannot find the document.

Single(k) Plan or "Solo(k)"

These plans are for owner-only entities. As soon as you have an employee who works more than 1000 hours in a 12-month period, you cannot sponsor a Single(k) plan.

The plans are often the most advantageous for self-employed individuals who have no employees and want to have access to higher pre-tax contribution levels. For all intents and purposes, it is a 401(k) plan, with the same contribution limits, ERISA protected, they allow loans and Roth contributions, etc. However, they can be sponsored at a much lower cost than traditional 401(k) plans because there are no non-owner employees. So there is no year-end testing, it's typically a boilerplate plan document, and the administration costs to establish and maintain these plans are typically under $400 per year compared to traditional 401(k) plans, which may cost $1,500+ per year to administer.

The beauty of these plans is the "employee contribution" of the plan, which gives it an advantage over SEP IRA plans. With SEP IRA plans, you are limited to contributions up to 25% of your income. So if you make $24,000 in self-employment income, you are limited to a $6,000 pre-tax contribution.

With a Single(k) plan, for 2026, I can contribute $24,500 per year (another $8,000 if I'm age 50-59 or 64 or over or $11,250 if I’m age 60-63) up to 100% of my self-employment income and in addition to that amount I can make an employer contribution up to 25% of my income. In the previous example, if you make $24,000 in self-employment income, you would be able to make a salary deferral contribution of $24,500 and an employer contribution of $500, effectively wiping out all of your taxable income for that tax year.

Simple IRA

Simple IRA's are the JV version of 401(k) plans. Smaller companies that have 1 – 50 employees that are looking to start are retirement plan will often times start with implementing a Simple IRA plan and eventually graduate to a 401(k) plan as the company grows. The primary advantage of Simple IRA Plans over 401(k) Plans is the cost. Simple IRA's do not require a TPA firm since they are self-administered by the employer and they do not require annual 5500 filings so the cost to setup and maintain the plan is usually much less than a 401(k) plan.

What causes companies to choose a 401(k) plan over a Simple IRA plan?

Owners want access to higher pre-tax contribution limits

They want to limit to the plan to just full time employees

The company wants flexibility with regard to the employer contribution

The company wants a vesting schedule tied to the employer contributions

The company wants to expand investment menu beyond just a single fund family

401(k) Plans

These are probably the most well-recognized employer-sponsored plans since, at one time or another, each of us has worked for a company that has sponsored this type of plan. So we will not spend a lot of time going over the ins and outs of these types of plan. These plans offer a lot of flexibility with regard to the plan features and the plan design.

We will issue a special note about the 401(k) market. For small business with 1 -50 employees, you have a lot of options regarding which type of plan you should sponsor but it's our personal experience that most investment advisors only have a strong understanding of 401(k) plans so they push 401(k) plans as the answer for everyone because it's what they know and it's what they are comfortable talking about. When establishing a retirement plan for your company, make sure you consult with an advisor who has a working knowledge of all these different types of retirement plans and can clearly articulate the pros and cons of each type of plan. This will assist you in establishing the right type of plan for your company.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Last updated June, 2026

Paying Down Debt: What is the Best Strategy?

Living with debt is not easy. It can be a constant burden and easily disrupt day-to-day life. Having debt will also ruin your credit score too. The worse your credit score gets, the less likely you will be accepted for any type of loan. One of the fastest ways to get rid of your debt is to pay your debt off in the correct order.

strategies for paying off debt

Living with debt is not easy. It can be a constant burden and easily disrupt day-to-day life. Having debt will also ruin your credit score too. The worse your credit score gets, the less likely you will be accepted for any type of loan. One of the fastest ways to get rid of your debt is to pay your debt off in the correct order.

STEP 1: Create a list of all your current debts

The first step is understanding what you owe. To start, make a master list of all your monthly credit card and loan statements. For each bill, include:

The creditor's name

The total amount you owe on that bill

The minimum required monthly payment

The interest rate (also known as APR)

The payment due date

STEP 2: List all of your monthly expenses

Add up all your monthly expenses: rent, car, food, utilities, health insurance and the minimum payments on your debts; as well as regular spending on things such as entertainment and clothing. Subtract that figure from your monthly after-tax income. The remaining amount is what you could put toward debt repayment each month-though it may make sense for you to save some.

STEP 3: Call your lenders

Call your lenders and explain your situation. They may be willing to lower your interest rate temporarily or waive late fees. You may also be able to lower your interest rate by transferring some high-interest credit card debt onto a new credit card with a lower rate (though that's not a long-term solution).

STEP 4: Payoff high interest rate or small balances first

You can start with the bill carrying the highest interest, or the one with the smallest balance. Prioritizing the highest-rate debt can save you more money: You pay off your most expensive debt sooner. Paying off the smallest debt can eliminate a bill faster, providing a motivating boost. Whichever you choose, make sure to pay at least the minimum on all your debts.

credit card debt

Pay the monthly minimum on each debt. The exception: your target bill. Put more money toward this one to pay it down faster. Once you pay off that bill, choose another to pay down aggressively. Your monthly debt repayment total shouldn't change, even when you eliminate bills. This way you gain momentum as you go, putting more and more money toward each remaining bill.

STEP 5: Get creative

You can use your annual tax refund or holiday bonus to pay down debt. Look for small ways to save money every day, such as riding your bike to work, or eating in instead of dining out. Another way to make a dent quickly is to sell unused or unnecessary belongings-maybe downgrading your car to a more affordable model with lower monthly payments.

STEP 6: Break the cycle

As you start to escape debt, it can be tempting to reward yourself by splurging on a new smartphone or an expensive dinner but just a few purchases can erase all your hard work. Instead, buy things with cash or your debit card, and think long and hard before taking on any new debt.

Read this book

If you want to live a debt free life, I strongly recommend you read the book "Total Money Makeover" by Dave Ramsey. Ramsey's book really paves the way to get out of debt and stay out of debt.

dave ramsey book

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Simple IRA vs. 401(k) - Which one is right for your company?

There are a lot of options available to small companies when establishing an employer sponsored retirement plan. For companies that have employees in addition to the owners of the company, the question is do they establish a 401(k) plan or a Simple IRA?The right fit for your company depends on:

compare simple ira and 401k

There are a lot of options available to small companies when establishing an employer sponsored retirement plan. For companies that have employees in addition to the owners of the company, the question is do they establish a 401(k) plan or a Simple IRA?The right fit for your company depends on:

What are the company's primary goals for establishing the plan?

How much the owner(s) plan to contribute to the plan?

How many employees does the company have?

Do you want to restrict the plan to only full time employees?

The cost of maintaining each plan?

Does the company intend to make an employer contribution to the plan?

Diversity of the investment menu

Below is a chart that contains a quick comparison of some of the main features of each type of plan:

simple ira vs 401K comparison chart

For many small companies it often makes sense to start with a Simple IRA plan and then transition to a 401K plan as the company grows or when the owner intends to start accessing the upper deferral limits offered by the 401(k) plan.

Simple IRA's are relatively easy to setup and the administrative fees to maintain these plans are typically lower in comparison to 401(k) plans. Most Simple IRA providers will only charge $10 - $30 to custody the accounts.

By comparison, 401(k) plans are ERISA covered plans which require a TPA Firm (third party administrator) to maintain the plan documents, conduct year end plan testing, and file the 5500 each year. The TPA fees vary based on the provider and the number of employees eligible to participate in the plan. A ballpark range is $1,500 - $2,500 for companies with under 50 employees.

However, the additional TPA fees associated with establishing a 401(k) plan may be justified if:

The owners intend to max out their employee deferrals

The owners are approaching retirement and need to make big contributions

The company wants to maintain flexibility with the employer contribution

The company would like to make Roth contributions, loans, or rollovers available

WARNING: Most investment providers are "one trick ponies". They will talk about 401(k) plans and not present other options because they either do not have a thorough understand of how Simple IRA plans work or they are only able to offer 401(k) plans. Before establishing a retirement plan it is important to work with a firm that presents both options, helps you to understand the difference between the two types of plans, and assist you in evaluating which plan would best meet your company's goals and objectives.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How to Create a Business Plan

Starting your own business can be an exciting and rewarding experience. It can offer numerous advantages such as being your own boss, setting your own schedule and making a living doing something you enjoy. But, becoming a successful entrepreneur requires thorough planning, creativity, and hard work. After making the decision to start your

How to Create a Business Plan

Starting your own business can be an exciting and rewarding experience. It can offer numerous advantages such as being your own boss, setting your own schedule and making a living doing something you enjoy. But, becoming a successful entrepreneur requires thorough planning, creativity, and hard work. After making the decision to start your own business, you'll need to be realistic about the sort of goals and targets you want to achieve at first. Businesses need targets though, so be sure to set some. Meeting targets does usually indicate business growth and success, so that's why they are so important. As with any business though, it all starts with a solid plan...

Learn from those before you

Before you make the leap to start your own business, make sure you talk or work for the person that you want to be 5 years from now. Working in the industry before taking your leap of faith will most likely increase your success rate. On the surface some businesses seem simple and straight forward. No business ever is. You have to figure out how the successful companies in that industry currently make money, what are their margins, who are the customers, who are the competitors, and more importantly what are the missteps that you should avoid when building you own business.

You must be able to answer these questions

Why am I starting a business?

What kind of business do I want?

Who is my ideal customer?

What products or services will my business provide?

Am I prepared to spend the time and money needed to get my business started?

What differentiates my business idea and the products or services I will provide from others in the market?

Where will my business be located?

How many employees will I need?

What types of suppliers do I need?

How much money do I need to get started?

Will I need to get a loan?

How soon will it take before my products or services are available?

How long do I have until I start making a profit?

Who is my competition?

How will I price my product compared to my competition?

How will I set up the legal structure of my business?

What taxes do I need to pay?

What kind of insurance do I need?

How will I manage my business?

How will I advertise my business?

Do not spend a dime until you can clearly answer all of these questions otherwise you are leaving your fate to chance.

Write your business plan

Your business plan is your roadmap to success. Business plans typically forecast out 3 to 5 years. Any shorter than that and you will have no idea where you are going with the business. Any longer than that is irrelevant because you may need to make material adjustments to your plan within the first 3 years as obstacles present themselves and as the competitive landscape changes along the way. Here are the key elements that you will want include in your business plan:

Executive Summary: Your executive summary is a snapshot of your business plan as a whole and touches on your company profile and goals. Read these tips about what to include.

Company Description: Your company description provides information on what you do, what differentiates your business from others, and the markets your business serves.

Market Analysis: Before launching your business, it is essential for you to research your business industry, market and competitors.

Organization & Management: Every business is structured differently. Find out the best organization and management structure for your business.

Service or Product Line: What do you sell? How does it benefit your customers? What is the product lifecycle? Get tips on how to tell the story about your product or service.

Marketing & Sales: How do you plan to market your business? What is your sales strategy? Read more about how to include this information in your plan.Funding Request: If you are seeking funding for your business, find out about the necessary information you should include in your plan.

Financial Projections: If you need funding, providing financial projections to back up your request is critical. Find out what information you need to include in your financial projections for your small business.

Your Competitive Advantage: What makes your business unique? Determining this could help you stand out from the crowd and give you advantages over your competitors.

Appendix: An appendix is optional, but a useful place to include information such as resumes, permits and leases. Find additional information you should include in your appendix.

Surround yourself with a great team of advisors.

Most business should have an accountant to ensure your books are correct and that all of the money your business is involved with is accounted for. You will collaborate with an attorney. You will also need a financial advisor. they will provide you with advice on where you can spend more money, what do you need to keep back or whether you need to reduce the money your spending on marketing for example. These professionals will help you to get your business established and help you with the key decisions that need to be made when you are establishing a business for the first time.

How should I incorporate?

What business expenses can I deduct?

How much cash do I need to sustain my business on a monthly basis?

It is likely that many of these professionals will be working with a client in your industry so they can provide you with real world guidance on the pros and cons of the decisions that you have to make.

Rule #1: Make sure you trust and like who you are working with. Do not just select a firm because they have a big name or because your friend uses them. You are going to be busy building your business so you will rely heavily on your team of professional advisors to make sure from a legal, tax, and financial standpoint that you are maximizing your resources.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.