Do I Have To Pay Taxes On My Inheritance?

Whenever people come into large sums of money, such as inheritance, the first question is “how much will I be taxed on this money”? Believe it or not, money you receive from an inheritance is likely not taxable income to you.

Whenever people come into large sums of money, such as inheritance, the first question is “how much will I be taxed on this money”? Believe it or not, money you receive from an inheritance is likely not taxable income to you.

Of course there are some caveats to this. If the inherited money is from an estate, there is a chance the money received was already taxed at the estate level. The current federal estate exclusion is $5,430,000 (estate taxes and the exclusion amount varies for states). Therefore, if the estate was large enough, a portion of the inheritance may have been subject to estate tax which is 40% in most cases. That being said, whether the money was or was not taxed at the estate level, you as an individual do not have to pay income taxes on the money.

Although the inheritance itself is not taxable, you may end up paying taxes if there is appreciation after the money is inherited. The type of account and distribution will dictate how the income will be taxed.

Basis Of Inherited Property

Typically, the basis of inherited property is the fair market value of the property on the date of the decedent’s death or the fair market value of the property on the alternate valuation date if the estate uses the alternate valuation date for valuing assets. An estate will choose to value assets on an alternate date subsequent to the date of death if certain assets, such as stocks, have depreciated since the date of death and the estate would pay less tax using the alternate date.

What the fair market value basis means is that if you inherit stock that was originally purchased for $500 and at the date of death has appreciated to $10,000, you will have a “step-up” basis of $10,000. If you turn around and sell the stock for $11,000, you will have a $1,000 gain and if you sell the stock for $9,000, you will have a $1,000 loss.

Inheriting a personal residence also provides for a step-up in basis but the gain or loss may be treated differently. If no one lives in the inherited home after the date of death, it will be treated similar to the stock example above. If you move into the home after death, any subsequent sale at a loss will not be deductible as it will be treated as your personal asset but a gain would have to be recognized and possibly taxed. If you rent the property subsequent to inheritance, it could be treated as a trade or business which would be treated differently for tax purposes.

Inheriting An IRA or Retirement Plan Account

Please read our article “Inherited IRA’s: How Do They Work” for a more detailed explanation of the three different types of distribution options.

When you inherit a retirement account, and you are not the spouse of the decedent, in most cases you will only have one option, fully distribute the account balance 10 years following the year of the decedents death. The SECURE Act that was passed in December 2019 dramatically change the distribution options available to non-spouse beneficiaries. See the article below:

If you are the spouse of the of the decedent, you are able to treat the retirement account as if it was yours and not be forced to take one of the options above. You will have to pay taxes on distributions but you do not have to start withdrawing funds immediately unless there are required minimum distributions needed.

Note: If the inherited account was an after tax account (i.e. Roth), the inheritor must choose one of the options presented above but no tax will be paid on distributions.

Non-Qualified Annuities

Non-qualified annuities are an exception to the step-up in basis rule. The non-spousal inheritor of a non-qualified annuity will have to take either a lump sum or receive payments over a specified time period. If the inheritor chooses a lump sum, the portion that represents the gain (lump sum balance minus decedent’s contributions) will be taxed as ordinary income. If the inheritor chooses a series of payments, distributions will be treated as last in, first out. Last in, first out means that the appreciation will be distributed first and fully taxable until there is only basis left.

If the spouse inherits the annuity, they most likely have the option to treat the annuity contract as if they were the original owner.

This article concentrated on inheritance at a federal level. There is no inheritance tax at a federal level but some states do have an inheritance tax and therefore meeting with a professional is recommended. New York currently does not have an inheritance tax.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Year End Tax Strategies

The end of the year is always a hectic time but taking the time to sit with a tax professional and determine what tax strategies will work best for you may save thousands on your tax bill due April 15th. As the deadline for your taxes starts to get closer, you may be in such a rush to file them on time that you make some mistakes in the process, but

year end tax strategies

The end of the year is always a hectic time but taking the time to sit with a tax professional and determine what tax strategies will work best for you may save thousands on your tax bill due April 15th. As the deadline for your taxes starts to get closer, you may be in such a rush to file them on time that you make some mistakes in the process, but don't worry, you won't be the only one. If you don't have the relevant tax strategy in place, you are more prone to mistakes. So, the purpose of this article is to discuss some of the most common tax strategies that may apply to you. It may be worth contacting a company that specializes in tax services if you're unsure of how to go about these strategies though. Some of the deadlines for these strategies aren't until tax filing but the majority include an action item that must be done by December 31st to qualify and therefore taking the time before year end is crucial.

Taxable Investment Accounts

Offset some of the realized gains incurred during the year by selling investments in loss positions. Often times dividends received and sales made in a taxable investment account are reinvested. Although the owner of the account never received cash in the transaction, the gain is still realized and therefore taxable. This may cause an issue when the cash is not available to pay the tax bill. By selling investments in a loss position prior to 12/31, you will offset some, if not all, of the gain realized during the year. If possible, sell enough investments in a loss position to take advantage of the maximum $3,000 loss that can be claimed on your tax return.

Note: The IRS recognized this strategy was being abused and implemented the "wash sale" rule. If you sell an investment in a loss position to diminish gains and then repurchase the same investment within 30 days, the IRS does not allow you to claim the loss therefore negating the strategy.

Convert a Traditional IRA to a Roth IRA

If you are in a low income year and will be taxed at a lower tax bracket than projected in the future, it may make sense to convert part of a traditional IRA to a Roth IRA. The current maximum contribution to a Roth IRA in a single year is $5,500 if under 50 and $6,500 if 50 plus. You will pay taxes on the distributions from the traditional but the benefit of a Roth is that all the contributions and earnings accumulated is tax free when distributed as long as the account has been opened for at least 5 years. Roth accounts are typically the last touched during retirement because you want the tax free accumulation as long as possible. Also, Roth accounts can be passed to a beneficiary who can continue accumulating tax free. Roth money is after tax money and therefore the IRS allows you to withdraw contributions tax and penalty free and let the earnings continue to accumulate tax free. If you don't have the cash come tax time to cover the conversion, you can convert the Roth money back to a traditional IRA by tax filing plus extension and the account will be treated as the Roth conversion never took place.

Donate to Charity if you Itemize

If you itemize deductions on your tax return, go through your closet and donate any clothing or household goods that you no longer use. There are helpful tools online that will allow you to value the items donated but be sure you keep record of what was donated and have the charity give you a receipt.

Max Out Your Employer Sponsored Retirement Plan

If you know you will be hit with a big tax bill and want to defer some of the taxes, max out your retirement plan if you haven't already. Employer sponsored plans, such as 401(k)'s, must be funded through payroll by 12/31 and therefore it is important to make this determination early and request your payroll department start upping your contribution for the remaining payroll periods in the year. The maximum for 401(k)'s in 2015 and 2016 is $18,000 if under 50 and $24,000 if 50 plus.

Business Owners – Cut Checks by 12/31

If your company had a great year and the cash is available, use it to pay for expenses you would normally hold off on. This could mean paying state taxes early, paying invoices you usually wait until the end of the payment term, paying monthly expenses like health or general insurance, or buying new office equipment. This might also mean investing in new office furniture such as chairs and desks, or more storage space for all of your paperwork and electronics. Above all, by getting the checks cut by 12/31, you realize the expense in the current year and will decrease your tax bill.

Business Owners – Set Up a Retirement Plan

For owners with no full time employees, a Single(k) plan being put in place by 12/31 will allow you to fund a retirement account up to the 401(k) limits mentioned early. As long as the plan is established by 12/31, the owner will be able to fund the plan any time before tax filing plus extension. If the plan is not established by 12/31, other options like the SEP IRA are available to take money off the table come tax time.With tax laws continuously changing, it is important to consult with your tax professional as there may be strategies available to you that could save you money. Don't procrastinate as some planning before the end of the year may be necessary to take full advantage.

About Rob.........

Hi, I'm Rob Mangold. I'm the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Understanding Investment Tax Forms

Making a wide variety of investments is a wise move as it means if one market drops, not all of your investments will be affected. If you've only invested in stocks or real estate then it would be a good idea to diversify. Take a look at this review and see if Bitcoin is something you want to invest in. The whole point of investing is to make a profit from your

investment tax forms

Types of Investment Income

Making a wide variety of investments is a wise move as it means if one market drops, not all of your investments will be affected. If you've only invested in stocks or real estate then it would be a good idea to diversify. Take a look at this review and see if Bitcoin is something you want to invest in. The whole point of investing is to make a profit from your investments so you want to give yourself as much of a chance of success as possible. Income from investments can be divided into four main categories;

Interest – Interest income is paid on bonds and other types of fixed-income securities such as fixed annuities. Interest is always taxable as ordinary income unless it is paid inside an IRA or qualified plan or annuity contract. Municipal bond interest is also tax free and interest from treasury securities is exempt from taxation at the state and local levels.

Dividends – These represent a portion of a company's current profits that it passes on to shareholders. Dividends can be taxed as ordinary income, or they may qualify for lower capital gains treatment in some cases if they are coded as "qualified" dividends.

Capital Gains – This represents the amount of profit realized when an investment is sold at a higher price than that for which it was bought. Long-term gains are realized for investments held for at least a year and a day before they were sold, and are taxed at a lower rate than ordinary income. Short-term gains are taxed as ordinary income.

Retirement and Annuity Distributions – Although distributions from retirement plans are not technically a form of investment income, they are listed here because IRA and retirement plan owners can only access the gains from their investments in these accounts by taking distributions. Normal distributions are always taxed as ordinary income.

Tax Forms

Each income type listed above is broken out on a corresponding 1099 form issued by the broker or issuer of the income generated. Every form includes the name, address and tax ID number of the issuing entity. These forms are listed as follows:1099-INT – Breaks out the interest paid to the investor. This form is issued for anyone who owns bonds, CDs or mutual funds that invested in fixed income securities or cash or has an interest-bearing bank or brokerage account.

Box 1 shows total taxable interest paid

Box 2 shows the amount of early withdrawal penalty, if any

Box 3 shows the amount of U.S. Treasury security interest paid

Box 4 shows the amount of tax withheld

Box 5 shows investment expenses

Box 6 shows foreign tax paid

Box 7 shows the foreign payor

Box 8 shows tax-exempt interest

Box 9 shows interest from special private activity bonds

Box 10 shows the CUSIP number for tax-free bond interest

Boxes 11-13 show state ID information and withholding

1099-DIV – This breaks down the total amount of dividends paid to an investor. It is issued to holders of any common stock, preferred stock, or mutual fund that invests in them. However, it is not issued to owners of cash value life insurance policies, as those dividends are merely a return of premium.

Box 1a shows total ordinary dividends

Box 1b shows total qualified dividends

Boxes 2a-d break down capital gains from mutual funds, REITs and collectibles

Box 3 shows nondividend distributions

Box 4 shows federal tax withheld

Box 5 shows investment expenses

Boxes 6 and 7 show foreign tax paid and the foreign payor

Boxes 8 and 9 show cash and noncash liquidation distributions

Box 10 shows private interest dividends

Box 11 shows specified private activity bond interest dividends

Boxes 12-14 show state ID information and withholding

1099-B – This form breaks down the amount of capital gain or loss that the investor realized for that tax year. It is issued to everyone who bought or sold publicly traded securities at a gain or loss. Many brokerage firms issue additional statements that break down the loss or gain for each trade and then quantify them into net long- and/or short-term gains and losses for the year.

Box 1a shows the date of sale or exchange

Box 1b shows the date of acquisition

Box 1c shows whether it is a long- or short-term gain or loss

Box 1d shows the ticker symbol of the security

Box 1e shows the quantity sold

Box 2a shows the gross proceeds reported to the IRS both before and after commission and expenses

Box 2b shows a checkbox if loss not allowed due to amount shown in box 2a

Box 3 shows cost or other basis

Box 4 shows federal tax withheld

Box 5 shows any amount of wash sale loss that was disallowed

Box 6 has checkboxes for noncovered securities and for sales where the basis in box 3 was reported to the IRS

Box 7 shows income from bartering

Box 8 is for a description of the security if needed

Boxes 9-12 break down realized and unrealized gains and losses from derivatives contracts

Boxes 13-15 show state ID information and withholding

1099-R – This form is issued to everyone who receives distributions from IRAs, qualified retirement plans or annuity contracts that are not housed inside a tax-deferred account or plan.

Box 1 shows the gross distribution amount

Box 2a shows the amount of taxable distribution

Box 2b has checkboxes for taxable amount not determined and total distribution

Box 3 shows amount of capital gain included in box 2a

Box 4 shows federal tax withheld

Box 5 shows employee/Roth contributions

Box 6 shows net unrealized appreciation in employer securities

Box 7 shows the distribution code that determines how the distribution is taxed

Box 8 shows the value of any annuity contract included in the distribution

Box 9a shows the value of distribution percentage that belongs to the recipient

Box 9b shows the amount of the employee's investment for annuity distributions where the exclusion ratio must be computed

If Box 10 is filled, refer to instructions on Form 5329

Box 11 shows the year the recipient first made a Roth contribution of any kind

Boxes 12-17 show state and local ID information and withholding

1099 MISC – Although most of this form pertains to earned income, it is also used to report royalty income (box 1) and working interest income (box 7) in oil and gas leases.Form 5498 – The receiving custodian of a qualified plan rollover or IRA transfer issues this to the account holder as proof that the transfer was not a taxable event and should not be counted as a distribution.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Should I Establish an Employer Sponsored Retirement Plan?

Employer sponsored retirement plans are typically the single most valuable tool for business owners when attempting to:

Reduce their current tax liability

Attract and retain employees

Accumulate wealth for retirement

establishing an employer sponsored retirement plan

Employer-sponsored retirement plans are typically the single most valuable tool for business owners when attempting to:

Reduce their current tax liability

Attract and retain employees

Accumulate wealth for retirement

But with all of the different types of plans to choose from, which one is the right one for your business? Most business owners are familiar with how 401(k) plans work, but that might not be the right fit given variables such as:

# of Employees

Cash flows of the business

Goals of the business owner

There are four main stream employer-sponsored retirement plans that business owners have to choose from:

SEP IRA

Single(k) Plan

Simple IRA

401(k) Plan

Since there are a lot of differences between these four types of plans, we have included a comparison chart at the conclusion of this newsletter, but we will touch on the highlights of each type of plan.

SEP IRA PLAN

This is the only employer-sponsored retirement plan that can be set up after 12/31 for the previous tax year. So, when you are sitting with your accountant in the spring and they deliver the bad news that you are going to have a big tax liability for the previous tax year, you can establish a SEP IRA up until your tax filing deadline plus extension, fund it, and take a deduction for that year.

However, if the company has employees who meet the plan's eligibility requirement, these plans become very expensive very quickly if the owner(s) want to make contributions to their own accounts. The reason is that these plans are 100% employer-funded, which means there are no employee contributions allowed, and the employer contribution is uniform for all plan participants. For example, if the owner contributes 15% of their income to the SEP IRA, they have to make an employer contribution equal to 15% of compensation for each employee who has met the plan's eligibility requirement. If the 5305-SEP Form, which serves as the plan document, is set up correctly, a company can keep new employees out of the plan for up to 3 years, but often it is either not set up correctly or the employer cannot find the document.

Single(k) Plan or "Solo(k)"

These plans are for owner-only entities. As soon as you have an employee who works more than 1000 hours in a 12-month period, you cannot sponsor a Single(k) plan.

The plans are often the most advantageous for self-employed individuals who have no employees and want to have access to higher pre-tax contribution levels. For all intents and purposes, it is a 401(k) plan, with the same contribution limits, ERISA protected, they allow loans and Roth contributions, etc. However, they can be sponsored at a much lower cost than traditional 401(k) plans because there are no non-owner employees. So there is no year-end testing, it's typically a boilerplate plan document, and the administration costs to establish and maintain these plans are typically under $400 per year compared to traditional 401(k) plans, which may cost $1,500+ per year to administer.

The beauty of these plans is the "employee contribution" of the plan, which gives it an advantage over SEP IRA plans. With SEP IRA plans, you are limited to contributions up to 25% of your income. So if you make $24,000 in self-employment income, you are limited to a $6,000 pre-tax contribution.

With a Single(k) plan, for 2025, I can contribute $23,500 per year (another $7,500 if I'm age 50-59 or 64 or over or $11,250 if I’m age 60-63) up to 100% of my self-employment income and in addition to that amount I can make an employer contribution up to 25% of my income. In the previous example, if you make $24,000 in self-employment income, you would be able to make a salary deferral contribution of $23,500 and an employer contribution of $500, effectively wiping out all of your taxable income for that tax year.

Simple IRA

Simple IRA's are the JV version of 401(k) plans. Smaller companies that have 1 – 50 employees that are looking to start are retirement plan will often times start with implementing a Simple IRA plan and eventually graduate to a 401(k) plan as the company grows. The primary advantage of Simple IRA Plans over 401(k) Plans is the cost. Simple IRA's do not require a TPA firm since they are self-administered by the employer and they do not require annual 5500 filings so the cost to setup and maintain the plan is usually much less than a 401(k) plan.

What causes companies to choose a 401(k) plan over a Simple IRA plan?

Owners want access to higher pre-tax contribution limits

They want to limit to the plan to just full time employees

The company wants flexibility with regard to the employer contribution

The company wants a vesting schedule tied to the employer contributions

The company wants to expand investment menu beyond just a single fund family

401(k) Plans

These are probably the most well-recognized employer-sponsored plans since, at one time or another, each of us has worked for a company that has sponsored this type of plan. So we will not spend a lot of time going over the ins and outs of these types of plan. These plans offer a lot of flexibility with regard to the plan features and the plan design.

We will issue a special note about the 401(k) market. For small business with 1 -50 employees, you have a lot of options regarding which type of plan you should sponsor but it's our personal experience that most investment advisors only have a strong understanding of 401(k) plans so they push 401(k) plans as the answer for everyone because it's what they know and it's what they are comfortable talking about. When establishing a retirement plan for your company, make sure you consult with an advisor who has a working knowledge of all these different types of retirement plans and can clearly articulate the pros and cons of each type of plan. This will assist you in establishing the right type of plan for your company.

Michael Ruger

About Michael.........

Hi, I'm Michael Ruger. I'm the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Do I Have to Pay Taxes on my Social Security Benefit?

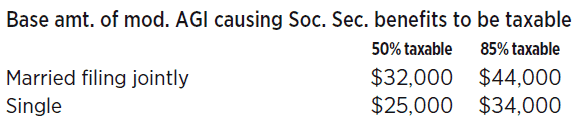

If your “combined income” exceeds specific annual limits, you may owe federal income taxes on up to 50% or 85% of your Social Security benefits. The limits for federal income tax purposes are listed in the chart below.

paying taxes on social security

If your “combined income” exceeds specific annual limits, you may owe federal income taxes on up to 50% or 85% of your Social Security benefits. The limits for federal income tax purposes are listed in the chart below.

percent of social security taxed

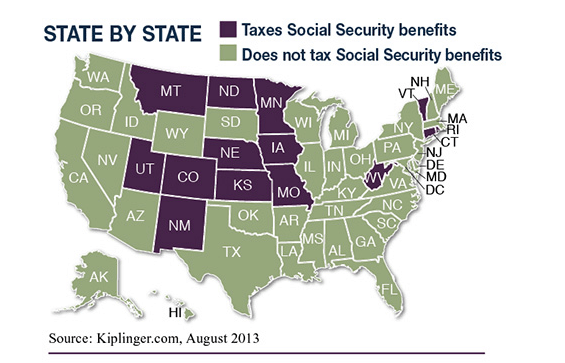

The federal income thresholds are not indexed for inflation, so they are the same every year. “Combined income” is defined as adjusted gross income plus any tax-exempt interest plus 50% of your Social Security Benefit. Some states tax Social Security Benefits, whereas others do not tax them. See the chart below:

what states do not tax social security benefits

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.