Tax Secret: R&D Tax Credits…You May Qualify

When you think of Research and Development (R&D) many people envision a chemistry lab or a high tech robotics company. It’s because of this thinking that millions of dollars of available tax credits for R&D go unused every year. R&D exists in virtually every industry and business owners need to start thinking about R&D in a different light because

When you think of Research and Development (R&D) many people envision a chemistry lab or a high tech robotics company. It’s because of this thinking that millions of dollars of available tax credits for R&D go unused every year. R&D exists in virtually every industry and business owners need to start thinking about R&D in a different light because there could be huge tax savings waiting for them.

Most companies don't realize that they qualify

Road paving companies, manufactures, a meatball company, software firms, and architecture firms are just a few examples of companies that have met the criteria to qualify for these lucrative tax credits.

Think of R&D as a unique process within your company that you may be using throughout the course of your everyday business that is specific to your competitive advantage. The purpose of these credits is to encourage companies to be innovative with the end goal of keeping more jobs here in the U.S. If you have an engineers on your staff, whether software engineers, design engineers, mechanical engineers there is a very good chance that these tax credits may be available to you. The R&D tax credits also allow you to look back to all open tax years so for companies that discover this for the first time, the upside can be huge. Tax years typically stay open for three years.

Accountants may not be aware of these credits

One of the main questions we get from business owners is “Shouldn’t my accountant have told me about this?” Many accounting firms are unaware of these tax credits and the process for qualifying which is why there are specialty consulting firms that work with companies to determine whether or not they are eligible for the credit. Some of our clients have worked with these firms and the company only pays the consulting firm if you qualify for the tax credits. Kind of a win-win situation.

We recently attended a seminar that was sponsored by Alliantgroup out of New York City and on their website it listed the following description of companies that qualify for these credits:“

Any company that designs, develops, or improves products, processes, techniques, formulas, inventions, or software may be eligible. In fact, if a company has simply invested time, money, and resources toward the advancement and improvement of its products and processes, it may qualify”.

We love helping our clients save taxes and in this case, like many others, we were looking at R&D in a different light.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Financial Planning To Do's For A Family

My wife and I just added our first child to the family so this is a topic that has been weighing on my mind over the last 40 weeks. I will share just one non-financial takeaway from the entire experience. The global population may be much lower if men had to go through what women do. That being said, this article is meant to be a guideline for some of the important financial items to consider with children. Worrying about your children will never end and being comfortable with the financial aspects of parenthood may allow you to worry a little less and be able to enjoy the time you have with the

My wife and I just added our first child to the family so this is a topic that has been weighing on my mind over the last 40 weeks. I will share just one non-financial takeaway from the entire experience. The global population may be much lower if men had to go through what women do. That being said, this article is meant to be a guideline for some of the important financial items to consider with children. Worrying about your children will never end and being comfortable with the financial aspects of parenthood may allow you to worry a little less and be able to enjoy the time you have with them.

There is a lot of information to take into consideration when putting together a financial plan and the larger your family the more pieces to the puzzle. It is important to set goals and celebrate them when they are met. Everything cannot be done in a day, a week, or a month, so creating a task list to knock off one by one is usually an effective approach. Using relatives, friends, and professionals as resources is important to know what should be on that list for topics you aren’t familiar with.

Create a Budget

It may seem tedious but this is one of the most important pieces of a family’s financial plan. You don’t have to track every dollar coming in and out but having a detailed breakdown on where your money is being spent is necessary in putting together a plan. This simple Expense Planner can serve as a guideline in starting your budget. If you don’t have an accurate idea of where your money is being spent then you can’t know where you can cut back or afford to spend more if needed. Also, the budget is a great topic during a romantic dinner.

You will always want to have 4-6 months expenses saved up and accessible in case a job is lost or someone becomes disabled and cannot work. Having an accurate budget will help you determine how much money you should have liquid.

Insurance

You want to be sure you are sufficiently covered if anything ever happened. One terrible event could leave your family in a situation that may have been avoidable. Insurance is also something you want to take care of as soon as possible so you know the coverage is there if needed.

Health Insurance

Research the policies that are available to you and determine which option may be the most appropriate in your situation. It is important to know the medical needs of your family when making this decision.

Turning one spouse’s single coverage into family coverage is one of the more common ways people obtain coverage for a family. Insurance companies will usually only allow changes to policies through open enrollment or when a “qualifying event” occurs. Having a child is usually a qualifying event but this may only allow the child to be added to one’s coverage, not the spouse. If that is the case, the spouse will want to make sure they have their own coverage until they can be added to the family plan.

It is important to use the resources available to you and consult with your health insurance provider on the ins and outs. If neither spouse has coverage through work, the exchange can be a resource for information and an option to obtain coverage (https://www.healthcare.gov/).

Life Insurance

The majority of people will obtain Term Life Insurance as it is a cost effective way to cover the needs of your family. Life insurance policies have an extensive underwriting process so the sooner you start the sooner you will be covered if anything ever happened. How Much Life Insurance Do I Need?, is an article that may help answer the question regarding the amount of life insurance sufficient for you.

Disability Insurance

The probability of using disability insurance is likely more than that of life insurance. Like life insurance, there is usually a long underwriting process to obtain coverage. Disability insurance is important as it will provide income for your family if you were unable to work. Below are some terms that may be helpful when inquiring about these policies.

Own Occupation – means that insurance will turn on if you are unable to perform YOUR occupation. “Any Occupation” is usually cheaper but means that insurance will only turn on if you can prove you can’t do ANY job.

60% Monthly Income – this represents the amount of the benefit. In this example, you will receive 60% of your current income. It is likely not taxable so the net pay to you may be similar to your paycheck. You can obtain more or less but 60% monthly income is a common benefit amount.

90 Day Elimination Period – this means the benefit won’t start until 90 days of being disabled. This period can usually be longer or shorter.

Cost of Living or Inflation Rider – means the benefit amount will increase after a certain time period or as your salary increases.

Wills, POA’s, Health Proxies

These are important documents to have in place to avoid putting the weight of making difficult decisions on your loved ones. There are generic templates that will suffice for most people but it is starting the process that is usually the most difficult. “What Is The Process Of Setting Up A Will?, is an article that may help you start.

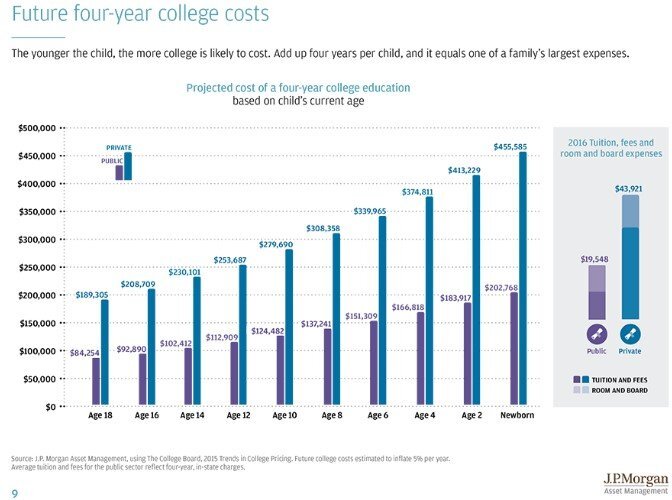

College Savings

The cost of higher education is increasing at a rapid rate and has become a financial burden on a lot of parents looking to pick up the tab for their kids. 529 accounts are a great way to start saving early. There are state tax benefits to parents in some states (including NYS) and if the money is spent on tuition, books, or room and board, the gain from the investments is tax free. Roth IRA’s are another investment vehicle that can be used for college but for someone to contribute to a Roth IRA they must have earned income. Therefore, a newborn wouldn’t be able to open a Roth IRA. Since the gain in 529’s is tax free if used for college, the earlier the dollars go into the account the longer they have to potentially earn income from the market.

529’s can also be opened by anyone, not just the parents. So if the child has a grandparent that likes buying savings bonds or a relative that keeps purchasing clothes the child will wear once, maybe have them contribute to a 529. The contribution would then be eligible for the tax deduction to the contributor if available in the state.

Below is a chart of the increasing college costs along with links to information on college planning.

About Rob……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Avoid These 1099 “Employee” Pitfalls

As financial planners we are seeing more and more individuals, especially in the software development and technology space, hired by companies as “1099 employees”. “1099 employees” is an ironic statement because if a company is paying you via a 1099 technically you are not an “employee” you are a self-employed sub-contractor. It’s like having

As financial planners we are seeing more and more individuals, especially in the software development and technology space, hired by companies as “1099 employees”. “1099 employees” is an ironic statement because if a company is paying you via a 1099 technically you are not an “employee” you are a self-employed sub-contractor. It’s like having your own separate company and the company that you work for is your “client”.

There are advantages to the employer to pay you as a 1099 sub-contractor as opposed to a W2 employee. When you are a W2 employee they may have to provide you with health benefits, the company has to pay payroll taxes on your wages, there may be paid time off, you may qualify for unemployment benefits if you are fired, eligibility for retirement plans, they have to put you on payroll, pay works compensation insurance, and more. Basically companies have a lot of expenses associated with you being a W2 employee that does not show up in your paycheck.

To avoid all of these added expenses the employer may decide to pay you as a 1099 “employee”. Remember, if you are a 1099 employee you are “self-employed”. Here are the most common mistakes that we see new 1099 employees make:

Making estimated tax payments throughout the year

This is the most common error. When you are a W2 employee, it’s the responsibility of the employer to withhold federal and state income tax from your paycheck. When you are a 1099 sub-contractor, you are not an employee, so they do not withhold taxes from your compensation…………that is now YOUR RESPONSIBILITY. Most 1099 individuals have to make what is called “estimated tax payments” four times a year which are based on either your estimated income for the year or 110% of the previous year’s income. Best advice……..if 1099 income is new for you, setup a consultation with an accountant. They will walk you through tax withholding requirements, tax deductions, tax filing forms, etc. It’s very difficult to get everything right using Turbo Tax when you are a self-employed individual.

Tracking mileage and expenses throughout the year

Since you are self-employed you need to keep track of your expenses including mileage which can be used as deductions against your income when you file your tax return. Again, we recommend that you meet with a tax professional to determine what you do and do not need to track throughout the year.

The tax return is prepared incorrectly

No one wants a love letter from the IRS. Those letters usually come with taxes due, penalties, and a “guilty until proven innocent” approach. There may be additional “schedules” that you need to file with your tax return now that you are self-employed. The tax schedules detail your self-employment income, deductions, estimated tax payments, and other material items.

Important rule, do not cut corners by reducing the gross amount of your 1099 income. This is a big red flag that is easy for the IRS to catch. The company that issued the 1099 to you usually reports that 1099 payment to the IRS with your social security number or the Tax ID number of your self-employment entity. The IRS through an automated system can run your social security number or tax ID to cross check the 1099 payment and 1099 income to make sure it was reported.

Legal protection

As a 1099 sub-contractor, you have to consider the liability that could arise from the services that you are providing to your “client” (your employer). As a self-employed individual, the company that you “work for” could sue you for any number of reasons and if you are operating the business under your social security number (which most are) your personal assets could be at risk if a lawsuit arises. Advice, talk to an attorney that is knowledgeable in business law to discuss whether or not setting up a corporate entity makes sense for your self-employment income to better protect yourself.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Tax Secret: Spousal IRAs

Spousal IRA’s are one of the top tax tricks used by financial planners to help married couples reduce their tax bill. Here is how it works:

Spousal IRA’s are one of the top tax tricks used by financial planners to help married couples reduce their tax bill. Here is how it works:

In most cases you need “earned income” to be eligible to make a contribution to an Individual Retirement Account (“IRA”). The contribution limits for 2026 is the lesser of 100% of your AGI or $7,500 for individuals under the age of 50. If you are age 50 or older, you are eligible for the $1,100 catch-up making your limit $8,600.

There is an exception for “Spousal IRAs,” and there are two cases where this strategy works very well.

Case 1: One spouse works and the other spouse does not. The employed spouse is currently maxing out their contributions to their employer-sponsored retirement plan, and they are looking for other ways to reduce their income tax liability.

If the AGI (adjusted gross income) for that couple is below $236,000 in 2025, the employed spouse can make a contribution to a Spousal Traditional IRA up to the $7,500/$8,600 limit even though their spouse had no “earned income”. It should also be noted that a contribution can be made to either a Traditional IRA or Roth IRA but the contributions to the Roth IRA do not reduce the tax liability because they are made with after tax dollars.

Case 2: One spouse is over the age of 70 ½ and still working (part-time or full-time) while the other spouse is retired. IRA rules state that once you are age 70½ or older, you can no longer make contributions to a traditional IRA. However, if you are age 70½ or older BUT your spouse is under the age of 70½, you still can make a pre-tax contribution to a traditional IRA for your spouse.

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Should I Buy Or Lease A Car?

This is one of the most common questions asked by our clients when they are looking for a new car. The answer depends on a number of factors:

How long do you typically keep your cars?

How many miles do you typically drive each year?

What do you want your down payment and monthly payment to be?

This is one of the most common questions asked by our clients when they are looking for a new car. The answer depends on a number of factors:

How long do you typically keep your cars?

How many miles do you typically drive each year?

What do you want your down payment and monthly payment to be?

We typically start off by asking how long clients usually keep their cars. If you are the type of person that trades in their car every 2 or 3 year for the new model, leasing a car is probably a better fit. If you typically keep your cars for 5 plus years, then buying a car outright is most likely the better option.

“How many miles do you drive each year?”

This is often times the trump card for deciding to buy instead of lease. Most leases allow you to drive about 12,000 miles per year but this varies from dealer to dealer. If you go over the mileage allowance there are typically sever penalties and it becomes very costly when you go to trade in the car at the end of the lease. We see younger individuals get caught in this trap because they tend to change jobs more frequently. They lease a car when they live 10 miles away from work but then they get a job offer from an employer that is 40 miles away from their house and the extra miles start piling on. When they go to trade in the car at the end of the lease they owe thousands of dollars due to the excess mileage.

We also ask clients how much they plan to put down on the car and what they want their monthly payments to be. If you think you can stay within the mileage allowance, a lease will more often require a lower down payment and have a lower monthly payment. Why? Because you are not “buying” the car. You are simply “borrowing” it from the dealership and your payments are based on the amount that the dealership expects the car to depreciate in value during the duration of the lease. When you buy a car……you own it……and at the end of the car loan you can sell it or continue to drive the car with no car payments.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

NY Free Tuition - Facts and Myths

On April 9th New York State became the first state to adopt a free tuition program for public schools. The program was named the “Excelsior Scholarship” and it will take effect the 2017 – 2018 school year. It has left people with a lot of unanswered questions

On April 9th New York State became the first state to adopt a free tuition program for public schools. The program was named the “Excelsior Scholarship” and it will take effect the 2017 – 2018 school year. It has left people with a lot of unanswered questions

Do I qualify?

How much does it cover?

What’s the catch?

Can I move my finances around to qualify for the program?

This article was written to help people better understand some of the facts and myths surrounding the NY Free Tuition Program.

Who qualifies for free tuition?

It’s based on the student’s household income and it phases in over a three year period:

2017: $100,000

2018: $110,000

2019: $125,000

MYTH #1: “If I reduce my household income in 2017 to get under the $100,000 threshold, it will help my child qualify for the free tuition program for the 2017 – 2018 school year.” WRONG. The income “determination year” is the same determination year that is used for FASFA filing. FASFA changed the rules in 2016 to look back two years instead of one for purposes of qualifying for financial aid. Those same rules will apply to the NY Free Tuition Program. So for the 2017 – 2018 school year, the $100,000 free tuition threshold will apply to your income in 2015.

MYTH #2: “If I make contributions to my retirement plan it will help reduce my household income to qualify for the free tuition program.” WRONG. Again, the free tuition program will use the same income calculation that is used in the FASFA process so it is not as simple as just looking at the bottom line of your tax return. For FASFA, any contributions that are made to retirement plans are ADDED back into your income for purposes of determining your income for that “determination year”. So making big contributions to a retirement plan will not help you qualify for free tuition.

What does it cover?

MYTH #3: “As long as my income is below the income threshold my kids (or I) will go to college for free.” DEFINE “FREE”. The Excelsior Scholarship covers JUST tuition. It does not cover books, room and board, transportation, or other costs associated with going to college. Annual tuition at a four-year SUNY college is currently $6,470. Here are the total fees obtained directly from the SUNY.edu website:

Tuition: $6,470 Covered

Student Fee: $1,640 Not Covered

Room & Board: $12,590 Not Covered

Books & Supplies: $1,340 Not Covered

Personal Expenses: $1,560 Not Covered

Transportation: $1,080 Not Covered

Total Costs $24,680

When you do the math for a student living on campus, the “Free” tuition program only covers 26% of the total cost of attending college.

What’s the catch?

There are actually a few:

CATCH #1: After the student graduates from college they have to LIVE and WORK in NYS for at least the number of years that the free tuition was awarded to the student OTHERWISE the “free tuition” turns into a LOAN that will be required to be paid back. Example: A student receives the free tuition for four years, works in New York for two years, and then moves to Massachusetts for a new job. That student will have to pay back two years of the free tuition.

CATCH #2: The student must maintain a specified GPA or higher otherwise the “free tuition” turns into a LOAN. However, the GPA threshold has yet to be released.

CATCH #3: It’s only for FULL TIME students earning at least 30 credit hours every academic year. This could be a challenge for students that have to work in order to put themselves through college.

CATCH #4: This is a “Last Dollar Program” meaning that students have to go through the FASFA process and apply for all other types of financial aid and grants that are available before the Free Tuition Program kicks in.

CATCH #5: The free tuition program is only available for two and four year degrees obtained within that two or four year period of time. If it take the student five years to obtain their four year bachelor’s degree, only four of the five years is covered under the free tuition program.

Summary

There are many common misunderstandings associated with the NYS Free Tuition Program. In general, it’s our view that this new program is only going to make college “more affordable” for a small sliver of students were not previously covered under the traditional FASFA based financial aid. Given the rising cost of college and the complexity of the financial aid process it has never been more important than it is now for individuals to work with a professional that have an in depth knowledge of the financial aid process and college savings strategies to help better prepare your household for the expenses associated with paying for college.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Strategies to Save for Retirement with No Company Retirement Plan

The question, “How much do I need to retire?” has become a concern across generations rather than something that only those approaching retirement focus on. We wrote the article, How Much Money Do I Need To Save To Retire?, to help individuals answer this question. This article is meant to help create a strategy to reach that number. More

The question, “How much do I need to retire?” has become a concern across generations rather than something that only those approaching retirement focus on. But what if you, or in the case of married couples, your spouse, are not covered by an employer-sponsored retirement plan? In this article we are going to cover retirement savings strategies for individuals that may not be covered by an employer-sponsored retirement plan.

Married Filing Jointly - One Spouse Covered by Employer Sponsored Plan and is Not Maxing Out

A common strategy we use for clients when a covered spouse is not maxing out their deferrals is to increase the deferrals in the retirement plan and supplement income with the non-covered spouse’s salary. The limits for 401(k) deferrals in 2026 is $24,500 for individuals under 50, $32,500 for individuals 50-59 and 64+ and $35,750 for individuals 60-63. For example, if I am covered and only contribute $8,000 per year to my account and my spouse is not covered but has additional money to save for retirement, I could increase my deferrals up to the plan limits using the amount of additional money we have to save. This strategy is helpful as it allows for easier tracking of retirement accounts and the money is automatically deducted from payroll. Also, if you are contributing pre-tax dollars, this will decrease your tax liability.

Note: Payroll deferrals must be withheld from payroll by 12/31. If you owe money when you file your taxes in April, you would not be able to go back and increase your deferrals in your company plan for that tax year.

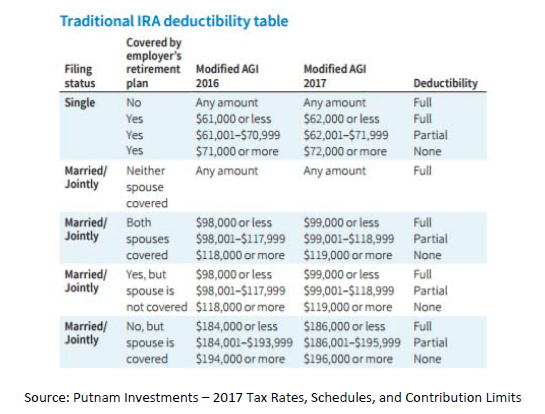

Married Filing Jointly - One Spouse Covered by Employer Sponsored Plan and is Maxing Out

If the covered spouse is maxing out at the high limits already, you may be able to save additional pre-tax dollars depending on your Adjusted Gross Income (AGI).

Below is the Traditional IRA Deductibility Table for 2026. This table shows how much individuals or married couples can earn and still deduct IRA contributions from their taxable income.

As shown in the chart, if you are married filing jointly and one spouse is covered, the couple can fully deduct IRA contributions to an account in the covered spouses name if AGI is less than $126,000 and can fully deduct IRA contributions to an account in the non-covered spouses name if AGI is less than $236,000. The Traditional IRA limits for 2026 are $7,500 if under 50 and $8,600 if 50+. These lower limits and income thresholds make contributing to company sponsor plans more attractive in most cases.

Single or Married Filing Jointly and Neither Spouse is Covered

If you (and your spouse if married filing joint) are not covered by an employer sponsored plan, you do not have an income threshold for contributing pre-tax dollars to a Traditional IRA. The only limitations you have relate to the amount you can contribute. These contribution limits for both Traditional and Roth IRA’s are $7,500 if under 50 and $8,600 if 50+. If married filing joint, each spouse can contribute up to these limits.

Unlike employer sponsored plans, your contributions to IRA’s can be made after 12/31 of that tax year as long as the contributions are in before you file your tax return.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.

Changes to 2016 Tax Filing Deadlines

In 2015, a bill was passed that changed tax filing deadlines for certain IRS forms that will impact a lot of filers. Not only is it important to know the changes so you can prepare and file your return timely but to understand why the changes were made.

In 2015, a bill was passed that changed tax filing deadlines for certain IRS forms that will impact a lot of filers. Not only is it important to know the changes so you can prepare and file your return timely but to understand why the changes were made.

Summary of Changes

IRS Form Business Type Previous Deadline New Deadline

1065 Partnership April 15 March 15

1120C Corporation March 15 April 15

NOTE: The dates in the chart above are for companies with years ending 12/31. If a company has a different fiscal year, Partnerships will now file by the 15th day of the third month following year end and C Corporations will now file by the 15th day of the fourth month following year end.

Why the Changes?

The most practical reason for the change to filing deadlines is that individuals with partnership interests will now have a better opportunity to file their individual returns (Form 1040) without extending. Form K-1 provides information related to the activity of a Partnership at the level of each individual partner. For example, if I own 50% of a Partnership, my K-1 would show 50% of the income (or loss) generated, certain deductions, and any other activity needed for me to file my Form 1040. The issue with the previous Partnership return deadline of April 15th is that it coincided with the individual deadline. This resulted in partners of the company not receiving their K-1’s with sufficient time to file their personal return by April 15th. With Partnerships now having a deadline of March 15th, this will give individuals a month to receive their K-1 and file their personal return without having to extend.

The deadline for Form 1120, which is filed by C Corporations, was also changed with this bill. Where the Form 1065 deadline was cut back by a month, the Form 1120 was extended a month. C Corporations, for tax purposes, are treated similar to individuals whereas they pay taxes directly when they file their return. Partnerships are not taxed directly, rather the income or loss is passed through to each individual partner who recognizes the tax ramifications on their personal return. For this reason, the deadline for Form 1120 being extended a month has little impact, if any, on individuals. The change gives C Corporations more time to file without having to extend the return.

S Corporations are another common business type. The deadlines for S Corporation returns (Form 1120S) were not changed with this bill. S Corporations are similar to Partnerships in that K-1’s are distributed to owners and the income or loss generated is passed through to the individuals return. That being said, Form 1120S already has a due date of March 15th, the same as the new Partnership deadline.

Extension Deadlines

IRS Form Business Type Deadline

1040 Individual October 15

1065 Partnership September 15

1120 C Corporation September 15

1120S S Corporation September 15

Extension deadlines were not immediately changed with the passing of the bill. Although Partnerships previously had the same filing deadline as individuals, the deadline with the filing of an extension was a month before. This was necessary because if a Partnership did not have to file an extended return until October 15th, individuals with partnership interests wouldn’t have a choice but to file delinquent.

The one change to the extension chart above set to take place in 2026 is the C Corporation extension being changed to October 15th.

Summary

Overall, the changes appear to have improved the filing calendar. This may be a big adjustment for Partnerships that are used to the April 15th deadline as they will have one less month to get organized and file. For this reason, you may see an increase in 2016 Partnership extensions.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally , professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, pleas feel free to join in on the discussion or contact me directly.