How Does Depreciation Work for Rental Properties?

Rental property depreciation allows investors to reduce taxable income by spreading the cost of a property over 27.5 years. This article explains how depreciation works, how it offsets rental income, and how improvements are treated. It also covers what happens when a property is fully depreciated and how depreciation recapture impacts taxes when selling. Understanding these rules can help investors maximize tax efficiency and avoid costly surprises.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Depreciation is one of the most important tax benefits of owning rental property. It allows property owners to offset part of the cost of owning the property against the rental income they receive, which can significantly reduce taxes in the early years of ownership.

In this article, we’ll cover:

What depreciation is and how it works

The 27.5-year depreciation rule for rental properties

How depreciation can offset rental income

How improvements are depreciated

What happens when depreciation runs out

What depreciation recapture is when you sell the property

What Is Depreciation?

Depreciation is a tax deduction that allows rental property owners to recover the cost of a property over time. Even though real estate often increases in value, the IRS allows you to treat the property as if it is wearing out over time and deduct a portion of its value each year.

This deduction can be used to offset rental income, which may reduce how much tax you owe on the income the property generates.

The 27.5-Year Depreciation Rule

Residential rental properties are typically depreciated over 27.5 years.

This means you take the purchase price of the property (excluding land value) and divide it by 27.5 to determine your annual depreciation deduction.

Example:

So, if you purchased a rental property for $300,000, you can depreciate roughly $11,000 per year.

How Depreciation Offsets Rental Income

Depreciation is considered a non-cash expense, meaning you don’t actually write a check for it, but you still get the tax deduction.

Example Scenario:

Rental income: $11,000 per year

Depreciation: $11,000 per year

In this example, the depreciation deduction offsets the rental income, which may result in little to no taxable rental income for that year.

This is one of the reasons rental real estate can be a very tax-efficient investment.

Depreciation on Improvements

Many rental property owners make improvements to their property, such as:

New roof

New furnace or heating system

Kitchen renovation

Bathroom remodel

Flooring

Additions

These are called capital improvements, and each improvement typically has its own depreciation schedule separate from the original property purchase.

For example:

Appliances: Often 5-year depreciation

Carpeting: Often 5–7 years

Roof: Often 27.5 years

HVAC systems: Often 15–27.5 years depending on classification

There are also situations where bonus depreciation or Section 179 may allow you to deduct a larger portion of the improvement cost upfront.

This is an area where working with a knowledgeable tax professional is very important, because depreciation schedules vary depending on the type of improvement.

What Happens When a Property Is Fully Depreciated?

After 27.5 years, the property is considered fully depreciated.

This means:

You no longer receive the annual depreciation deduction

More of your rental income becomes taxable

Your tax liability on rental income may increase

However, you still own the property and still collect rental income — you just don’t get the depreciation tax benefit anymore.

What Is Depreciation Recapture?

Depreciation is a great tax benefit while you own the property, but when you sell the property, the IRS requires something called depreciation recapture.

When you sell a rental property:

You pay capital gains tax on the profit from the sale

You also pay tax on all the depreciation you took over the years

Depreciation recapture is taxed at a flat 25% federal tax rate

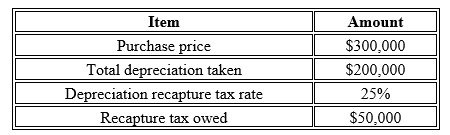

Example:

So in this example, when the property is sold, the owner would owe:

Capital gains tax on the profit plus

$50,000 in depreciation recapture tax

This surprises many real estate investors if they are not prepared for it.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

How long do you depreciate a rental property?Residential rental property is depreciated over 27.5 years.

-

What happens if I don't take depreciation?The IRS assumes you took it anyway, and you may still have to pay depreciation recapture when you sell.

-

Can I depreciate renovations on my rental property?Yes, but renovations and improvements typically have their own depreciation schedules.

-

What is bonus depreciation?Bonus depreciation allows you to deduct a large portion of certain improvements upfront instead of spreading the deduction over many years.

-

Do I have to pay depreciation back when I sell the property?When you sell the property, you may be subject to depreciation recapture, which taxes the total depreciation amount taken by 25%.

-

What happens after 27.5 years of depreciation?The property is fully depreciated and you no longer receive the annual depreciation deduction.

-

Does depreciation reduce my capital gains when I sell?No. Depreciation actually lowers your cost basis, which can increase your taxable gain and trigger depreciation recapture.

-

Can depreciation create a loss on paper?Yes. Depreciation can sometimes create a taxable loss even if the property is producing positive cash flow.

-

Should I work with a CPA if I own rental property?It's highly recommended. Depreciation, improvements, and recapture rules are complex, and a knowledgeable CPA can help you maximize tax benefits and avoid costly mistakes.

What Happens to an HSA Account When Someone Passes Away?

Health Savings Accounts offer powerful tax benefits, but those benefits can change significantly after death. This article explains how HSAs are treated when inherited by a spouse, non-spouse, or estate. Learn key tax rules, planning strategies, and how to reduce the tax burden on beneficiaries. Proper beneficiary designation is critical to maximizing HSA value.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

Health Savings Accounts (HSAs) are one of the most tax-advantaged accounts available, but many people don’t realize that what happens to an HSA after death depends entirely on who the beneficiary is. The tax consequences can be very different depending on whether the beneficiary is a spouse, a non-spouse, or if no beneficiary is named at all.

In this article, we’ll cover:

What happens if a spouse is the beneficiary

What happens if a non-spouse is the beneficiary

What happens if no beneficiary is named

Strategies to reduce taxes on inherited HSAs

Why beneficiary designations are so important

Scenario 1: Spouse Is the Beneficiary

If a spouse is listed as the beneficiary of an HSA, the outcome is very favorable.

When the account owner passes away:

The spouse can assume ownership of the HSA

The transfer of ownership is not taxable

The spouse can continue using the HSA tax-free for qualified medical expenses

If the spouse already has their own HSA, they can roll the inherited HSA into their own HSA

This is the best-case scenario from a tax perspective because the account simply continues as an HSA with all the same tax benefits:

Pre-tax contributions

Tax-deferred growth

Tax-free withdrawals for medical expenses

In other words, the surviving spouse steps into the shoes of the original account owner.

Scenario 2: Non-Spouse Is the Beneficiary

If the beneficiary is not a spouse (for example, a child, grandchild, or friend), the rules change significantly.

When a non-spouse inherits an HSA:

The account ceases to be an HSA as of the date of death

The beneficiary cannot continue the HSA

The beneficiary cannot roll it into their own HSA

The fair market value of the HSA becomes taxable income to the beneficiary in the year of death

This means inheriting an HSA as a non-spouse can create a large immediate tax bill.

How to Reduce the Tax Impact

There is one strategy that can reduce the tax burden:

If the deceased had unpaid medical expenses at the time of death, the HSA can be used to pay those expenses. Any amount used to pay the decedent’s qualified medical expenses reduces the taxable amount that passes to the beneficiary.

Example:

HSA value at death: $50,000

Unpaid medical bills: $10,000

Taxable amount to beneficiary: $40,000

This can make a meaningful difference in the taxes owed.

Scenario 3: No Beneficiary Is Named

If no beneficiary is listed on the HSA:

The HSA becomes part of the deceased person’s estate

The fair market value of the HSA becomes taxable income on the final tax return

The account terminates as an HSA

This is usually the least favorable outcome, which is why it is very important to make sure beneficiaries are properly listed on your HSA account.

Planning Strategy: Should You Spend Your HSA If Your Beneficiaries Are Non-Spouse?

Because HSAs are not very tax-efficient to leave to non-spouse beneficiaries, it may make sense to use the HSA during your lifetime especially if:

You are single, or

Your beneficiaries are children or other non-spouse individuals

Remember, when you use HSA money for medical expenses, those dollars come out tax-free. But if a non-spouse inherits the account, the entire account can become taxable immediately.

After Age 65: Your HSA Works Like a Traditional IRA

Another important rule:

After age 65, you can take money out of an HSA for non-medical expenses and:

You will not pay a penalty

But you will pay ordinary income tax

It works similar to a traditional IRA

This creates a planning opportunity.

If it looks like:

You may not use all your HSA for medical expenses, and

You are in a lower tax bracket

It may make sense to intentionally withdraw money from the HSA and pay the tax at your lower tax rate, instead of leaving the entire account to a non-spouse beneficiary who may have to recognize the entire balance as income in a single year.

This strategy can help reduce the overall family tax bill.

Final Thoughts

HSAs are excellent savings vehicles, but they are not great assets to leave to non-spouse beneficiaries due to the immediate tax consequences.

That’s why good HSA planning includes:

Naming the correct beneficiaries

Using the HSA strategically during your lifetime

Coordinating HSA withdrawals with your tax bracket in retirement

When used properly, an HSA can be a powerful tool for retirement healthcare planning — but like all financial accounts, beneficiary planning matters.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs)

-

Does an HSA avoid probate?Yes, if a beneficiary is named, the HSA typically passes directly to the beneficiary.

-

Can my spouse continue my HSA after I die?Yes, a spouse can assume ownership of the HSA and continue using it as their own.

-

Do non-spouse beneficiaries pay taxes on inherited HSAs?Yes, the full value of the HSA is taxable income to the beneficiary in the year of death.

-

Can a child roll an inherited HSA into their own HSA?No, non-spouse beneficiaries cannot continue or roll over the HSA.

-

Can HSA funds be used to pay medical bills after death?Yes, HSA funds can be used to pay the deceased person's qualified medical expenses, which reduces the taxable amount to beneficiaries.

-

What happens if I forgot to name a beneficiary?The HSA becomes part of your estate and the value becomes taxable on your final tax return.

-

After age 65, can I use my HSA for non-medical expenses?Yes, you can withdraw funds penalty-free, but you will pay ordinary income tax.

-

Is an HSA a good account to leave to children?Generally, no. Because the account becomes fully taxable to them immediately.

-

Who should be the beneficiary of my HSA?In many cases, naming your spouse as beneficiary is the most tax-efficient option.

-

Should I spend down my HSA before I die?If your beneficiaries are non-spouse beneficiaries, it may make sense to use the HSA during your lifetime to avoid leaving them a large taxable account.

Tax Rules for Selling Your House to a Family Member

Selling a home to a family member involves more than just agreeing on a price. This guide explains tax implications, gift rules, cost basis considerations, and seller financing strategies. Learn how fair market value, the primary residence exclusion, and the Applicable Federal Rate impact your decision. Understand how to structure the transaction to avoid unintended tax consequences. Ideal for parents helping children navigate today’s housing market.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

This article was inspired by a conversation with a client who is considering selling their primary residence to their child. One of the biggest challenges in today’s housing market is affordability for first-time homebuyers. With housing prices and interest rates rising dramatically over the past five years, many parents who were already planning to downsize, relocate, or move into a more retirement-friendly home are now considering selling their home directly to their children to help them afford their first house.

While this can be a great strategy, there are a number of tax rules, gift rules, and financing considerations that need to be understood before entering into an intrafamily real estate transaction. In this article, we’re going to walk through the key areas families should consider before moving forward.

Discounting the Price of the House

One of the most common questions we get from clients is whether they should sell the house to their child at full market value or discount the price.

For example, if a house is worth $600,000, can you sell it to your child for $400,000?

The answer is yes, you can sell your house for whatever price you want. However, if you sell the home significantly below fair market value, the difference between the market value and the sale price may be considered a gift.

So if:

Market value = $600,000

Sale price = $400,000

Difference = $200,000

That $200,000 could be treated as a gift to the child.

For most families, this does not mean you will owe gift tax. However, you may need to file a gift tax return because the gift exceeds the annual gift exclusion. The amount above the annual exclusion simply reduces your lifetime gift exemption, which is currently $15 million per person at the federal level.

Why Selling at Fair Market Value May Be Better

From a tax standpoint, it may actually make more sense to sell the home at full market value rather than at a discount, because of the primary residence capital gain exclusion.

Single filer: Can exclude $250,000 of gain

Married filing jointly: Can exclude $500,000 of gain

Example

Purchase price: $200,000

Current value: $600,000

Gain: $400,000

If the parents are married, the $400,000 gain is below the $500,000 exclusion, meaning they would owe no capital gains tax even if they sell the home for full market value.

But the bigger planning opportunity is actually for the child’s future taxes.

If the child buys the home for $600,000, that becomes their cost basis. If they later sell the home for $1,000,000, their gain is $400,000, which may be fully covered by the primary residence exclusion.

However, if the parents sold the home for $400,000, the child’s cost basis is $400,000. If they later sell for $1,000,000, the gain is $600,000, and $100,000 could become taxable.

So in many situations, a better strategy may be:

Sell the home at fair market value and gift money for the down payment, instead of discounting the purchase price.

This can create a better long-term tax outcome.

Do the Parents Hold the Mortgage?

The next big question is how the child will finance the purchase. There are two main options:

Option 1: Traditional Mortgage

The child gets a mortgage through a bank, and the parents receive cash from the sale.

Option 2: Parents Hold the Mortgage (Seller Financing)

If the parents do not need the cash from the sale, they can hold the mortgage and essentially act as the bank. The child makes mortgage payments directly to the parents.

This is commonly called seller financing or an intrafamily mortgage.

Minimum Interest Rate (AFR)

If parents hold the mortgage, they must charge a minimum interest rate called the Applicable Federal Rate (AFR) to satisfy IRS rules. For a long-term loan such as a mortgage, the long-term AFR applies.

As of March 2026, the long-term AFR is approximately 4.6%.

So the process typically looks like this:

Determine purchase price

Determine down payment

Remaining balance becomes the mortgage

Mortgage must charge at least the AFR rate

Child makes monthly payments to the parents

Tax Treatment of Payments

As the child makes mortgage payments:

The Principal portion is not taxable to the parents

The Interest portion of each payment is taxable income to the parents

Forgiving the Mortgage

Another question that comes up with intrafamily mortgages is:

“Can we forgive payments or forgive the loan later?”

The answer is yes, but this brings us back to the gift rules.

Forgiving Monthly Payments

Let’s say the child’s mortgage payment is $3,000 per month and the parents decide to waive the payments for a year.

That would equal:

$3,000 × 12 = $36,000 per year

If the parents are married, they can gift up to the annual gift exclusion amount each year without filing a gift tax return (for example, $38,000 combined in 2026). If the forgiven amount is below the annual exclusion, no gift tax return is required.

If the forgiven amount exceeds the annual exclusion, then a gift tax return must be filed, but again, no gift tax is owed unless the parents exceed their lifetime exemption.

Forgiving the Entire Mortgage

If the parents decide at some point to forgive the remaining balance of the mortgage, that is considered a gift of the remaining loan balance, and a gift tax return would need to be filed for that year.

This shows that there is actually a lot of flexibility when families use intrafamily mortgages. Payments can be structured, forgiven, or adjusted over time, but the gift rules must be tracked.

Summary

If parents are in the fortunate position where they can sell their home to their child, we are seeing this strategy more and more due to the challenges first-time homebuyers face in today’s housing market.

However, it’s important to understand the key planning areas:

Should you sell at fair market value or discount the price?

Should the child get a traditional mortgage or should the parents hold the mortgage?

What are the Applicable Federal Rate (AFR) rules?

How do the gift tax rules apply if you discount the house or forgive payments?

How does this affect the child’s future cost basis?

How does this fit into the parents’ estate plan?

These transactions involve tax planning, estate planning, and financial planning, so we strongly recommend working with a tax professional and financial advisor when considering an intrafamily real estate transaction.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions

-

Can I sell my house to my child for less than market value?Yes, but the difference may be considered a gift.

-

Do I have to pay gift tax if I sell the house at a discount?Usually no, but you may need to file a gift tax return.

-

Do I pay capital gains tax if I sell to my child?You may qualify for the primary residence capital gain exclusion.

-

Is it better to sell at market value and gift the down payment?In many cases, yes, for long-term tax planning reasons.

-

Can I be the bank for my child’s mortgage?Yes, this is called seller financing.

-

What interest rate do I have to charge?At least the IRS Applicable Federal Rate (AFR).

-

Is the interest my child pays me taxable?Yes, interest is taxable income to the parents.

-

Can I forgive mortgage payments?Yes, but the forgiven amount may be considered a gift.

-

What happens if I forgive the entire loan?It is treated as a gift of the remaining balance.

-

Should we work with a professional for this type of transaction?Yes, you should coordinate with a CPA, financial advisor, and real estate attorney.

Planning for Healthcare Costs in Retirement: Why Medicare Isn’t Enough

Healthcare often becomes one of the largest and most underestimated retirement expenses. From Medicare premiums to prescription drugs and long-term care, this article from Greenbush Financial Group explains why healthcare planning is critical—and how to prepare before and after age 65.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

When most people picture retirement, they imagine travel, hobbies, and more free time—not skyrocketing healthcare bills. Yet, one of the biggest financial surprises retirees face is how much they’ll actually spend on medical expenses.

Many retirees dramatically underestimate their healthcare costs in retirement, even though this is the stage of life when most people access the healthcare system the most. While it’s common to pay off your mortgage leading up to retirement, it’s not uncommon for healthcare costs to replace your mortgage payment in retirement.

In this article, we’ll cover:

Why Medicare isn’t free—and what parts you’ll still need to pay for.

What to consider if you retire before age 65 and don’t yet qualify for Medicare.

The difference between Medicare Advantage and Medicare Supplement plans.

How prescription drug costs can take retirees by surprise.

The reality of long-term care expenses and how to plan for them.

Planning for Healthcare Before Age 65

For those who plan to retire before age 65, healthcare planning becomes significantly more complicated—and expensive. Since Medicare doesn’t begin until age 65, retirees need to bridge the coverage gap between when they stop working and when Medicare starts.

If your former employer offers retiree health coverage, that’s a tremendous benefit. However, it’s critical to understand exactly what that coverage includes:

Does it cover just the employee, or both the employee and their spouse?

What portion of the premium does the employer pay, and how much is the retiree responsible for?

What out-of-pocket costs (deductibles, copays, coinsurance) remain?

If you don’t have retiree health coverage, you’ll need to explore other options:

COBRA coverage through your former employer can extend your workplace insurance for up to 18 months, but it’s often very expensive since you’re paying the full premium plus administrative fees.

ACA marketplace plans (available through your state’s health insurance exchange) may be an alternative, but premiums and deductibles can vary widely depending on your age, income, and coverage level.

In many cases, healthcare costs for retirees under 65 can be substantially higher than both Medicare premiums and the coverage they had while working. This makes it especially important to build early healthcare costs into your retirement budget if you plan to leave the workforce before age 65.

Medicare Is Not Free

At age 65, most retirees become eligible for Medicare, which provides a valuable foundation of healthcare coverage. But it’s a common misconception that Medicare is free—it’s not.

Here’s how it breaks down:

Part A (Hospital Insurance): Usually free if you’ve paid into Social Security for at least 10 years.

Part B (Medical Insurance): Covers doctor visits, outpatient care, and other services—but it has a monthly premium based on your income.

Part D (Prescription Drug Coverage): Also carries a monthly premium that varies by plan and income level.

Example:

Let’s say you and your spouse both enroll in Medicare at 65 and each qualify for the base Part B and Part D premiums.

In 2025, the standard Part B premium is approximately $185 per month per person.

A basic Part D plan might average around $36 per month per person.

Together, that’s about $220 per person, or $440 per month for a couple—just for basic Medicare coverage. And this doesn’t include supplemental or out-of-pocket costs for things Medicare doesn’t cover.

NOTE: Some public sector or state plans even provide Medicare Part B premium reimbursement once you reach 65—a feature that can be extremely valuable in retirement.

Medicare Advantage and Medicare Supplement Plans

While Medicare provides essential coverage, it doesn’t cover everything. Most retirees need to choose between two main options to fill in the gaps:

Medicare Advantage (Part C) plans, offered by private insurers, bundle Parts A, B, and often D into one plan. These plans usually have lower premiums but can come with higher out-of-pocket costs and limited provider networks.

Medicare Supplement (Medigap) plans, which work alongside traditional Medicare, help pay for deductibles, copayments, and coinsurance.

It’s important not to simply choose the lowest-cost plan. A retiree’s prescription needs, frequency of care, and preferred doctors should all factor into the decision. Choosing the cheapest plan could lead to much higher out-of-pocket expenses in the long run if the plan doesn’t align with your actual healthcare needs.

Prescription Drug Costs: A Hidden Retirement Expense

Prescription drug coverage is one of the biggest cost surprises for retirees. Even with Medicare Part D, out-of-pocket expenses can add up quickly depending on the medications you need.

Medicare Part D plans categorize drugs into tiers:

Tier 1: Generic drugs (lowest cost)

Tier 2: Preferred brand-name drugs (moderate cost)

Tier 3: Specialty drugs (highest cost, often with no generic alternatives)

If you’re prescribed specialty or non-generic medications, you could spend hundreds—or even thousands—per month despite having coverage.

To help, some states offer programs to reduce these costs. For example, New York’s EPIC program helps qualifying seniors pay for prescription drugs by supplementing their Medicare Part D coverage. It’s worth checking if your state offers a similar benefit.

Planning for Long-Term Care

One of the most misunderstood aspects of Medicare is long-term care coverage—or rather, the lack of it.

Medicare only covers a limited number of days in a skilled nursing facility following a hospital stay. Beyond that, the costs become the retiree’s responsibility. Considering that long-term care can easily exceed $120,000 per year, this can be a major financial burden.

Planning ahead is essential. Options include:

Purchasing a long-term care insurance policy to offset future costs.

Self-insuring, by setting aside savings or investments for potential care needs.

Planning to qualify for Medicaid through strategic trust planning

Whichever route you choose, addressing long-term care early is key to protecting both your assets and your peace of mind.

Final Thoughts

Healthcare is one of the largest—and most underestimated—expenses in retirement. While Medicare provides a foundation, retirees need to plan for premiums, prescription costs, supplemental coverage, and potential long-term care needs.

If you plan to retire before 65, early planning becomes even more critical to bridge the gap until Medicare begins. By taking the time to understand your options and budget accordingly, you can enter retirement with confidence—knowing that your healthcare needs and your financial future are both protected.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQ)

Why isn’t Medicare enough to cover all healthcare costs in retirement?

While Medicare provides a solid foundation of coverage starting at age 65, it doesn’t pay for everything. Retirees are still responsible for premiums, deductibles, copays, prescription drugs, and long-term care—expenses that can add up significantly over time.

What should I do for healthcare coverage if I retire before age 65?

If you retire before Medicare eligibility, you’ll need to bridge the gap with options like COBRA, ACA marketplace plans, or employer-sponsored retiree coverage. These plans can be costly, so it’s important to factor early healthcare premiums and out-of-pocket expenses into your retirement budget.

What are the key differences between Medicare Advantage and Medicare Supplement plans?

Medicare Advantage (Part C) plans combine Parts A, B, and often D, offering convenience but limited provider networks. Medicare Supplement (Medigap) plans work alongside traditional Medicare to reduce out-of-pocket costs. The right choice depends on your budget, health needs, and preferred doctors.

How much should retirees expect to pay for Medicare premiums?

In 2025, the standard Medicare Part B premium is around $185 per month, while a basic Part D plan averages about $36 monthly. For a married couple, that’s roughly $440 per month for both—before adding supplemental coverage or out-of-pocket expenses. These costs should be built into your retirement spending plan.

Why are prescription drugs such a major expense in retirement?

Even with Medicare Part D, out-of-pocket drug costs can vary widely based on your prescriptions. Specialty and brand-name medications often carry high copays. Programs like New York’s EPIC can help eligible seniors manage these costs by supplementing Medicare coverage.

Does Medicare cover long-term care expenses?

Medicare only covers limited skilled nursing care following a hospital stay and does not pay for most long-term care needs. Since extended care can exceed $120,000 per year, retirees should explore options like long-term care insurance, Medicaid planning, or setting aside savings to self-insure.

How can a financial advisor help plan for healthcare costs in retirement?

A financial advisor can estimate future healthcare expenses, evaluate Medicare and supplemental plan options, and build these costs into your retirement income plan. At Greenbush Financial Group, we help retirees design strategies that balance healthcare needs with long-term financial goals.

Special Tax Considerations in Retirement

Retirement doesn’t always simplify your taxes. With multiple income sources—Social Security, pensions, IRAs, brokerage accounts—comes added complexity and opportunity. This guide from Greenbush Financial Group explains how to manage taxes strategically and preserve more of your retirement income.

By Michael Ruger, CFP®

Partner and Chief Investment Officer at Greenbush Financial Group

You might think that once you stop working, your tax situation becomes simpler — after all, no more paychecks! But for many retirees, taxes actually become more complex. That’s because retirement often comes with multiple income sources — Social Security, pensions, pre-tax retirement accounts, brokerage accounts, cash, and more.

At the same time, retirement can present unique tax-planning opportunities. Once the paychecks stop, retirees often have more control over which tax bracket they fall into by strategically deciding which accounts to pull income from.

In this article, we’ll cover:

How Social Security benefits are taxed

Pension income rules (and how they vary by state)

Taxation of pre-tax retirement accounts like IRAs and 401(k)s

Developing an efficient distribution strategy

Special tax deductions and tax credits for retirees

Required Minimum Distribution (RMD) planning

Charitable giving strategies, including QCDs and donor-advised funds

How Social Security Is Taxed

Social Security benefits may be tax-free, partially taxed, or mostly taxed — depending on your provisional income. Provisional income is calculated as:

Adjusted Gross Income (AGI) + Nontaxable Interest + ½ of Your Social Security Benefits.

Here’s a quick summary of how benefits are taxed at the federal level:

While Social Security is taxed at the federal level, most states do not tax these benefits. However, a handful of states — including Colorado, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, Rhode Island, Utah, and Vermont — do impose some form of state tax on Social Security income.

Pension Income

If you’re fortunate to receive a state pension, your state of residence plays a big role in determining how that income is taxed.

If you have a state pension and continue living in the same state where you earned the pension, many states exclude that income from state tax.

However, with state pensions, if you move to another state, and that state has income taxation at the stateve level, your pension may become taxable in your new state of domicile.

If you have a pension with a private sector employer, often times those pension payment are full taxable at both the federal and state level.

Some states also provide preferential treatment for private pensions or IRA income. For example, New York excludes up to $20,000 per person in pension or IRA distributions from state income tax each year — a significant benefit for retirees managing taxable income.

Taxation of Pre-Tax Retirement Accounts

Pre-tax retirement accounts — including Traditional IRAs, 401(k)s, 403(b)s, and inherited IRAs — are typically taxed as ordinary income when distributions are made.

However, the tax treatment at the state level varies:

Some states (like New York) exclude a set amount – for example New York excludes the first $20,000 per person per year — from state taxation.

Others tax all pre-tax distributions in full.

A few states offer income-based exemptions or reduced rates for lower-income retirees.

Because these rules differ so widely, it’s important to research your state’s tax laws.

Developing a Tax-Efficient Distribution Strategy

A well-designed distribution strategy can make a big difference in how much tax you pay throughout retirement.

Many retirees have income spread across:

Pre-tax accounts (401(k), IRA)

After-tax brokerage accounts

Roth IRAs

Social Security

Let’s say you need $70,000 per year to maintain your lifestyle. Some of that may come from Social Security, but you’ll need to decide where to withdraw the rest.

With smart planning, you can blend withdrawals from different accounts to minimize your overall tax liability and control your tax bracket year by year. The goal isn’t just to reduce taxes today — it’s to manage them over your lifetime.

Special Deductions and Credits in Retirement

Your Adjusted Gross Income (AGI) or Modified AGI doesn’t just determine your tax bracket — it also affects which deductions and credits you can claim.

A few important highlights:

The Big Beautiful Tax Bill that just passed in 2025 introduces a new Age 65+ tax deduction of $6,000 per person over and above the existing standard deduction.

Certain deductions and credits, however, phase out once income exceeds specific thresholds.

Your income level also affects Medicare premiums for Parts B and D, which increase if your income surpasses the IRMAA thresholds (Income-Related Monthly Adjustment Amount).

Managing your taxable income through careful distribution planning can therefore help preserve deductions and keep Medicare premiums lower.

Required Minimum Distribution (RMD) Planning

Once you reach age 73 or 75 (depending on your birth year), you must begin taking Required Minimum Distributions (RMDs) from your pre-tax retirement accounts — even if you don’t need the money.

These RMDs can significantly increase your taxable income, especially when stacked on top of Social Security and other income sources.

A proactive strategy is to take controlled distributions or perform Roth conversions before RMD age. Doing so can reduce the size of your future RMDs and potentially lower your lifetime tax bill by spreading taxable income across more favorable tax years.

Charitable Giving Strategies

Many retirees are charitably inclined, but since most take the standard deduction, they don’t receive an additional tax benefit for their donations.

There are two primary strategies to consider:

Donor-Advised Funds (DAFs) – You can “bunch” several years’ worth of charitable giving into one tax year to exceed the standard deduction, then direct the funds to charities over time.

Qualified Charitable Distributions (QCDs) – Once you reach age 70½, you can donate directly from your IRA to a qualified charity. These QCDs are excluded from taxable income and count toward your RMD once those begin.

Final Thoughts

Retirement opens up new opportunities — and new complexities — when it comes to managing taxes. Understanding how your various income sources interact and planning your distributions strategically can help you:

Reduce taxes over your lifetime

Preserve more of your retirement income

Maintain flexibility and control over your financial future

As always, it’s wise to coordinate with a financial advisor and tax professional to ensure your retirement tax strategy aligns with your goals, income sources, and state tax rules.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQ)

How are Social Security benefits taxed in retirement?

Depending on your provisional income, up to 85% of your Social Security benefits may be subject to federal income tax. Most states don’t tax these benefits, though a few—including Colorado, Minnesota, and Utah—do.

How is pension income taxed, and does it vary by state?

Pension income is typically taxable at the federal level, but state rules differ. Some states exclude public pensions from taxation or offer partial exemptions—like New York’s $20,000 per person exclusion for pension or IRA income. If you move to another state in retirement, your pension’s tax treatment could change.

What taxes apply to withdrawals from pre-tax retirement accounts?

Distributions from Traditional IRAs, 401(k)s, and similar pre-tax accounts are taxed as ordinary income. Some states offer exclusions or partial deductions, while others tax these withdrawals in full. Understanding your state’s rules is essential for accurate tax planning.

What is a tax-efficient withdrawal strategy in retirement?

A tax-efficient strategy blends withdrawals from different account types—pre-tax, Roth, and after-tax—to control your annual tax bracket. The goal is not just to lower taxes today but to reduce lifetime taxes by managing income across multiple years and minimizing required minimum distributions later.

What new tax deductions or credits are available for retirees?

The 2025 tax law introduced an additional $6,000 deduction per person age 65 and older, in addition to the standard deduction. Keeping taxable income lower through smart planning can also help retirees preserve deductions and avoid higher Medicare IRMAA surcharges.

How do Required Minimum Distributions (RMDs) impact taxes?

Starting at age 73 or 75 (depending on birth year), retirees must withdraw minimum amounts from pre-tax retirement accounts, which increases taxable income. Performing partial Roth conversions or strategic withdrawals before RMD age can help reduce future tax exposure.

What are Qualified Charitable Distributions (QCDs) and how do they work?

QCDs allow individuals age 70½ or older to donate directly from an IRA to a qualified charity, satisfying all or part of their RMD while excluding the amount from taxable income. This strategy helps maximize charitable impact while reducing taxes in retirement.

401(k) Catch-Up Contribution FAQs: Your Top Questions Answered (2026 Rules)

Got questions about 401(k) catch-up contributions? You’re not alone. With updated 2025 limits and new Roth rules on the horizon, this article answers the most common questions about who qualifies, how much you can contribute, and what strategic moves to consider in your 50s and early 60s.

As retirement gets closer, many individuals start to wonder how they can supercharge their savings and make up for lost time. For those age 50 and older, catch-up contributions offer a powerful opportunity to contribute more to retirement accounts beyond the standard annual limits. Below, I’ve addressed some of the most common questions I get from clients about catch-up contributions, especially with the updated 2026 rules in play.

Can I make catch-up contributions if I’m working part-time in retirement?

Yes, as long as you have earned income from a job, and you have met the plan’s eligibility requirements. So, even if you’ve scaled back your hours or semi-retired, you may still be eligible to make additional contributions.

For example, if you're age 65 and working part-time and eligible for your company’s 401(k) plan, you can contribute up to $23,500, plus an extra $7,500 in catch-up contributions for a total of $31,000 in 2025, assuming you have at least $31,000 in W2 compensation.

If you have less than $31,000 in W2 comp, you will be capped by the lesser of the annual contribution limit or 100% of your W2 compensation.

Are Roth catch-up contributions allowed?

Yes. If your employer plan offers a Roth option, you can choose to make your catch-up contributions as Roth dollars. This means you contribute after-tax money now and take qualified distributions tax-free in retirement.

This option is popular for individuals who are in the same tax bracket now as they plan to be in retirement. The Roth source also avoids required minimum distributions (RMDs) starting at age 73 or 75.

How do catch-up contributions impact required minimum distributions (RMDs)?

Catch-up contributions themselves don’t change the timing or calculation of RMDs. However, where you put the catch-up dollars can affect your future RMDs. If you contribute catch-up dollars to a Roth 401(k) and then roll over the balance to a Roth IRA prior to the RMD start age, RMDs are not required.

Adding more to the pre-tax employee deferral source within the plan may increase your future RMD requirement since pre-tax retirement accounts are subject to the annual RMD requirement once you reach age 73 (for those born 1951–1959) or 75 (for those born 1960 or later).

Should I prioritize catch-up contributions or pay down my mortgage?

This depends on your interest rate, your retirement timeline, tax bracket, and your overall financial goals. Generally, if your mortgage interest rate is below 4% and you’re behind on retirement savings, catch-up contributions may be a better use of your idle cash, especially if your investments are growing tax-deferred (pre-tax) or tax-free (roth).

However, if you’re already on track for retirement and the psychological benefit of being debt-free is important to you, putting extra cash toward your mortgage can make sense. It’s all about balancing the right financial decision with your personal preferences.

What happens if I forget to update my payroll deferrals after turning 50?

Unfortunately, you won’t automatically get the benefit since your employer’s payroll system won’t adjust your contributions just because you had a birthday. You need to take action and manually increase your deferrals to take advantage of the higher limits.

For example, if you turn 50 this year and forget to bump your 401(k) deferrals, you may miss out on contributing an additional $8,000. Worse yet, once the calendar year closes, you can't go back and make up for it.

Are there additional tax benefits associated with making catch-up contributions?

It’s common that the years leading up to retirement are often the highest income years for an individual. The additional pre-tax contributions associated with the catch-up contribution allow employees to take more of their income off the table during the peak income years and shift it into the retirement years, when ideally they are in a lower tax bracket.

What is the new age 60 – 63 catch-up contribution?

Starting in 2025, there is a new enhanced catch-up contribution available to employees covered by 401(k) and 403(b) plans who are aged 60 to 63. Instead of being limited to just the regular $8,000 catch-up contribution, in 2026, employees age 60 – 63 will be allowed to make a catch-up contribution equal to $11,250.

What is the Mandatory Roth catch-up for high income earners?

Starting in 2026, and for the following years, if an employee makes more than $150,000 in W2 compensation (indexed for inflation) with the same employer in the previous year, that employee will no longer be allowed to make pre-tax catch-up contributions. If they make a catch-up contribution, it will be required to be a Roth catch-up contribution.

Final Thoughts…

Whether you’re still decades from retirement or just a few years away, catch-up contributions are a crucial part of retirement planning for those age 50 and older. With the 2026 limits now in place and Roth rules continuing to evolve, understanding how these contributions fit into your broader plan can help you save smarter, and avoid costly mistakes.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What are catch-up contributions and who qualifies for them?

Catch-up contributions allow individuals age 50 and older to contribute additional funds to retirement accounts beyond the standard annual limits. For 2025, employees can contribute up to $23,500 to a 401(k) plus an extra $7,500 in catch-up contributions, for a total of $31,000 — provided they have sufficient earned income.

Can part-time workers make catch-up contributions?

Yes. As long as you have earned income and meet your employer plan’s eligibility requirements, you can make catch-up contributions even if you’re working part-time. The total contribution amount cannot exceed 100% of your W-2 compensation.

Are Roth catch-up contributions available?

If your employer plan offers a Roth option, you can make your catch-up contributions as Roth dollars. Roth contributions are made after tax, grow tax-free, and qualified withdrawals are also tax-free, offering flexibility for future tax planning.

How do catch-up contributions affect required minimum distributions (RMDs)?

Catch-up contributions do not change when RMDs begin, but the type of account matters. Pre-tax catch-up dollars increase your future RMDs, while Roth 401(k) contributions can be rolled into a Roth IRA before RMD age to avoid mandatory withdrawals altogether.

Should I prioritize catch-up contributions or pay down my mortgage?

It depends on your financial situation. If your mortgage rate is low (under 4%) and you’re behind on retirement savings, maximizing catch-up contributions may be beneficial. However, paying down your mortgage may make sense if you’re already on track for retirement and value being debt-free or if you have a higher interest rate on your mortgage.

What happens if I forget to increase my deferrals after turning 50?

Your employer’s payroll system won’t automatically adjust contributions, so you must update them manually. Missing the adjustment means forfeiting that year’s extra contribution opportunity — once the year ends, you can’t retroactively make up the difference.

What is the new enhanced age 60–63 catch-up contribution for 2025?

Starting in 2025, employees aged 60 to 63 can make a larger catch-up contribution of up to $11,250 to 401(k) and 403(b) plans, providing an additional savings boost in the final years before retirement.

What is the new rule for high-income earners and Roth catch-ups?

Beginning in 2026, employees earning more than $145,000 (indexed for inflation) in W-2 income with the same employer will be required to make catch-up contributions as Roth contributions — pre-tax catch-ups will no longer be allowed for this group.

Last updated June, 2026

401(k) Catch-Up Contributions Explained: Maximize Your Retirement Savings in 2026

Turning 50? It’s time to boost your retirement savings.

This article breaks down the updated 2025 401(k) catch-up contribution limits, new rules for ages 60–63, and whether pre-tax or Roth contributions make the most sense for your situation.

For individuals aged 50 or older, catch-up contributions allow for additional retirement savings during what are often their highest earning years. With updated limits and new provisions taking effect in 2026, this strategy can be especially valuable for those looking to strengthen their financial position ahead of retirement and maximize tax efficiency in what are typically their highest income years leading up to retirement.

Below, I break down the 2026 catch-up contribution limits, rules, and strategic considerations to help you make informed decisions.

What Are Catch-Up Contributions?

Catch-up contributions allow individuals aged 50 or older to contribute above the standard annual limits to retirement accounts. You’re eligible to make catch-up contributions starting in the calendar year you turn 50.

2026 Contribution Limits

Here are the updated 2026 401(k) contribution limits for each plan type:

401(k), 403(b), 457(b):

Standard limit: $24,500

Age 50 – 59 & Age 64+ catch-up: $8,000

Age 60 – 63 catch-up: $11,250

New 401(k) Age 60–63 Catch-Up Limits

Beginning in 2025, a new tier of higher catch-up limits will apply to individuals between ages 60 and 63. Under the SECURE 2.0 Act, these individuals can contribute an additional amount equal to 50% of the regular catch-up contribution for that plan year. For 2026, this equates to an extra $3,250, bringing the total possible contribution to $35,750 for 401(k), 403(b), and 457(b) plans. This enhanced catch-up contribution is optional for employers, so it's important to confirm with your plan sponsor whether this provision is available in your plan.

To learn more, read our article: New Age 60 – 63 401(k) Enhanced Catch-up Contribution Starting in 2025

Pre-Tax vs. Roth Catch-Up Contributions

Employer-sponsored retirement plans often allow participants to choose whether their catch-up contributions are made on a pre-tax or Roth (after-tax) basis. The best approach depends on income levels, expected tax rates in retirement, and broader financial planning goals.

Pre-tax contributions reduce your taxable income today but are taxed when withdrawn in retirement.

Roth contributions provide no current tax deduction but grow and distribute tax-free in retirement.

When Pre-Tax May Make Sense:

You're in a high tax bracket today (e.g., 24%+)

You expect to be a lower tax bracket during the retirement years

Example:

Tom is age 60, married, and earns $405,000 annually, placing him in the 32% federal tax bracket. In the next 5 years, Tom expects to retire and be in a lower federal tax bracket. By making pre-tax catch-up contributions now, it will allow him to reduce his current taxable income, while potentially taking distributions in a lower tax bracket later.

When Roth May Make Sense:

You expect your current tax rate to be roughly the same in retirement

You already have substantial pre-tax retirement account balances

You expect tax rates to rising in the future

Example:

Susan is age 52, single filer, earns $125,000 per year, and is in the 22% tax bracket. She expects her income to remain steady over time. By choosing Roth catch-up contributions, she pays tax now at a relatively low rate and avoids taxation on future withdrawals.

Mandatory Roth Catch-Up Contributions for High Earners (Effective 2026)

Starting in 2026, individuals earning $150,000 or more (adjusted for inflation) in wages from the same employer in the previous year will be required to make catch-up contributions to their workplace plan on a Roth basis. This rule applies only to employer-sponsored plans (like 401(k)s) and does not impact Simple IRA plans. For 2025, these Roth rules were delayed, giving high-income earners time to prepare.

To learn about the rules and exceptions for high earners, read our article: Mandatory 401(k) Roth Catch-up Details Confirmed by IRS January 2025

The Big Picture: Why This Strategy Matters Near Retirement

For individuals within five to ten years of retirement, catch-up contributions provide an opportunity to meaningfully increase retirement savings without relying on higher investment returns or making dramatic lifestyle changes. The added contributions also support strategic tax planning by allowing savers to choose between pre-tax and Roth treatment based on their broader income picture.

Catch-up contributions can help:

Maximize tax-advantaged savings when your income is typically at its highest

Take advantage of compound growth on a larger balance

Strategically shift assets into Roth accounts for future tax-free income

Consider the numbers:

A 60-year-old contributing the full $35,750 annual catch-up amount for three consecutive years could accumulate over $114,000 in additional retirement savings, assuming a 7% annual return. If contributed to a Roth 401(k), those funds would grow and be distributed tax-free, offering valuable flexibility in retirement.

Even if retirement is only a few years away, catch-up contributions can play a significant role in improving retirement readiness and reducing future tax burdens.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Frequently Asked Questions (FAQs):

What are catch-up contributions and who qualifies for them?

Catch-up contributions allow individuals aged 50 or older to contribute more to retirement accounts than the standard annual limit. Eligibility begins in the calendar year you turn 50, regardless of your income level or how close you are to retirement.

What are the 2025 catch-up contribution limits?

In 2025, employees can contribute up to $23,500 to a 401(k), 403(b), or 457(b) plan. Those aged 50–59 and 64 or older can contribute an additional $7,500, while individuals aged 60–63 can make an enhanced catch-up contribution of $11,250, for a total of $34,750 if allowed by their employer’s plan.

How does the new age 60–63 catch-up rule work?

Starting in 2025, individuals between ages 60 and 63 can make a higher catch-up contribution equal to 150% of the standard catch-up limit. This provision under the SECURE 2.0 Act lets older workers maximize savings during their final working years, but availability depends on whether an employer adopts the rule.

Should I make my catch-up contributions pre-tax or Roth?

The best option depends on your tax situation. Pre-tax contributions reduce taxable income now and are ideal if you expect to be in a lower tax bracket in retirement. Roth contributions are made after-tax but grow tax-free and are advantageous if you expect future tax rates to rise or your income to remain steady.

What is the mandatory Roth catch-up rule for high-income earners?

Beginning in 2026, employees earning $145,000 or more (adjusted for inflation) from the same employer in the previous year must make catch-up contributions on a Roth basis. This means contributions will be made after tax, and future withdrawals will be tax-free.

Why are catch-up contributions especially important near retirement?

Catch-up contributions help individuals nearing retirement boost savings during peak earning years without depending solely on market growth. They also provide tax planning flexibility by letting savers choose between pre-tax and Roth options based on their expected future income and tax rates.

Last updated June, 2026

Understanding Required Minimum Distributions & Advanced Tax Strategies For RMD's

A required minimum distribution (RMD) is the amount that the IRS requires you to take out of your retirement account each year when you hit a certain age or when you inherit a retirement account from someone else. It’s important to plan tax-wise for these distributions because they can substantially increase your tax liability in a given year;

Understanding Required Minimum Distributions & Advanced Tax Strategies For RMD’s

A required minimum distribution (RMD) is the amount that the IRS requires you to take out of your retirement account each year when you hit a certain age or when you inherit a retirement account from someone else. It’s important to plan tax-wise for these distributions because they can substantially increase your tax liability in a given year; consequentially, not distributing the correct amount from your retirement accounts will invite huge tax penalties from the IRS. Luckily, there are advanced tax strategies that can be implemented to help reduce the tax impact of these distributions, as well as special situations that exempt you from having to take an RMD.

Age 73 or 75

LAW CHANGE: There were changes to the RMD age when the SECURE Act was passed into law on December 19, 2019. Prior to the law change, you were required to start taking RMD’s in the calendar year that you turned age 70 1/2. For anyone turning age 70 1/2 after December 31, 2019, their RMD start age is now delayed to either age 73 or 75, depending on the individual’s date of birth.

The IRS has a special table called the “Uniform Lifetime Table”. There is one column for your age and another column titled “distribution period”. The way the table works is you find your age and then identify what your distribution period is. Below is the calculation step by step:

1) Determine your December 31 balance in your pre-tax retirement accounts for the previous year end

2) Find the distribution period on the IRS uniform lifetime table

3) Take your 12/31 balance and divide that by the distribution period

4) The previous step will result in the amount that you are required to take out of your retirement account by 12/31 of that year

Example: If you turn age 73 in March of 2025, you would be required to take your first RMD in that calendar year unless you elect the April 1st delay in the first year. After you find your age on the IRS uniform lifetime table, next to it, you will see a distribution period of 26.5. The balance in your traditional IRA account on December 31, 2024 was $400,000, so your RMD would be calculated as follows:

$400,000 / 26.5 = $15,094

Your required minimum distribution amount for the 2025 tax year is $15,094. The first RMD will represent about 3.8% of the account balance, and that percentage will increase by a small amount each year.

RMD Deadline

There are very important dates that you need to be aware of once you reach RMD start age. In most years, you have to make your required minimum distribution prior to December 31 of that tax year. However, there is an exception for the year that you turn age 73 or 75. In the year that you reach the RMD start date, you have the option of taking your first RMD either prior to December 31 or April 1 of the following year. The April 1 exception only applies to the year of your first RMD. Every year after that first year, you are required to take your distribution by December 31st.

Delay to April 1st

So why would someone want to delay their first required minimum distribution to April 1? Since the distribution results in additional taxable income, it’s about determining which tax year is more favorable to realize the additional income.

For example, you may have worked for part of the year that you turned age 73 so you’re showing earned income for the year. If you take the distribution from your IRA prior to 12/31 that represents more income that you have to pay tax on which is stacked up on top of your earned income. It may be better from a tax standpoint to take the distribution in the following January because the amount distributed from your retirement account will be taxed in a year when you have less income.

Very important rule:

If you decide to delay your first required minimum distribution past 12/31, you will be required to take two RMD‘s in that following year.

Example: I retire from my company in September 2024 and I also turned 73 that same year. If I elect to take my first RMD on February 1, 2025, prior to the April 1 deadline, I will then be required to take a second distribution from my IRA prior to December 31, 2025.

If you are already retired in the year that you turn age 73 and your income level is going to be relatively the same between the current year and the following year, it often makes sense to take your first RMD prior to December 31st, so are not required to take two RMD‘s the following year which can subject those distributions to a higher tax rate and create other negative tax events.

IRS Penalty

If you fail to distribute the required amount by the given deadline, the IRS will be kind enough to assess a 25% penalty on the amount that you should have taken for your required minimum distribution. If you were required to take a $12,000 distribution and you failed to do so by the applicable deadline, the IRS will hit you with a $3,000 penalty. If you make the distribution, but the amount is not sufficient enough to meet the required minimum distribution amount, they will assess the 25% penalty on the shortfall instead. Bottom line, don’t miss the deadline.

Exceptions If You Are Still Working

There is an exception to the RMD rule. If your only retirement asset is an employer sponsored retirement plan, such as a 401(k), 403(b), or 457, as long as you are still working for that employer, you are not required to take an RMD from that retirement account until after you have terminated from employment regardless of your age.

Example: You are age 73 and your only retirement asset is a 401(k) account with your current employer with a $100,000 balance; you will not be required to take an RMD from your 401(k) account in that year, even though you have reached your RMD start date.

In the year that you terminate employment, however, you will be required to take an RMD for that year. For this reason, be very careful if you’re working over the age of 73 / 75 and leave employment in late December. Your retirement plan provider will have a very narrow window of time to process your required minimum distribution prior to the December 31st deadline.

This employer sponsored retirement plan exception only applies to balances in your current employer’s retirement plan. You do not receive this exception for retirement plan balances with previous employers.

If you have retirement accounts such as IRA’s or other retirement plans outside of your current employer’s plan, you will still be required to take RMDs from those accounts, even though you are still working.

Advanced Tax Strategies

There are two advanced tax strategies that we use when individuals are age 73 or 75 and still working for a company that sponsors are qualified retirement plan.

It’s not uncommon for employees to have a retirement plan with their current employer, a rollover IRA, and some miscellaneous balance in retirement plans from former employers. Since you only have the exception to the RMD within your current employers plan, and most 401(k), 403(b), and 457 plans accept rollovers from IRAs and other qualified plans, it may be advantageous to complete rollovers of all those retirement accounts into your current employer’s plan so you can completely avoid the RMD requirement.

Strategy number two. If you are still working and you have access to an employer sponsored plan, you are usually able to make employee contributions pre-tax to the plan. If you are required to take a distribution from your IRA which results in taxable income, as long as you are not already maxing out your employee deferrals in your current employer’s plan, you can instruct payroll to increase your contributions to the plan to reduce your earned income by the amount of the required minimum distribution coming from your other retirement accounts.

Example: You are age 73 and working part time for an employer that gives you access to a 401(k) plan. Your 401(k) has a balance of $20,000 with that employer, but you also have a Rollover IRA with a balance of $200,000. In this case, you would not be required to take an RMD from your 401(k) balance, but you would be required to take an RMD from your IRA which would total approximately $7,500. Since the $7,500 will represent additional income to you in that tax year, you could turn around and instruct the payroll company to take 100% of your paychecks and put it pre-tax into your 401(k) account until you reach $7,500 which would wipe out the tax liability from the distribution that occurred from the IRA.

Or, if you have a spouse that still working and they have access to a qualified retirement plan, the same strategy can be implemented. Additionally, if you file a joint tax return, it doesn’t matter whose retirement plan it goes into because it’s all pre-tax at the end of the day.

5% or More Owner

Unfortunately, I have some bad news for business owners. If you are a 5% or more owner of the company, it does not matter whether or not you are still working for the company; you are required to take an RMD from the company’s employer-sponsored retirement plan regardless. The IRS is well aware that the owner of the business could decide to work for two hours a week just to avoid the required minimum distributions. Sorry entrepreneurs.

A Spouse That Is More Than 10 Years Younger

I mentioned above that the IRS has a uniform lifetime table for calculating the RMD amount. If your spouse is more than 10 years younger than you are, there is a special RMD table that you will need to use called the “joint life table” with a completely different set of distribution periods, so make sure you’re using the correct table when calculating the RMD amount.

Charitable contributions

There is also an advanced tax strategy that allows you to make contributions to charity directly from your IRA and you do not have to pay tax on those disbursements. The special charitable distributions from IRA’s are only allowed for individuals that are age 70.5 or older. If you regularly make contributions to a charity, church, or not for profit, or if you do not need the income from the RMD, this may be a great strategy to shelter what otherwise would have been more taxable income. There are a lot of special rules surrounding how these charitable contributions work. For more information on this strategy see the following article:

Lower Your Tax Bill By Directing Your Mandatory IRA Distributions To Charity

Roth IRA’s

You are not required to take RMD‘s from Roth IRA accounts at age 73 or 75, this is one of the biggest tax advantages of Roth IRAs.

Inherited IRA

When you inherit an IRA from someone else, those IRAs have their own set of required minimum distribution rules, which vary from the normal age 73/75 rules. The SECURE Act, which was passed in 2019, split non-spouse beneficiaries of IRAs into two categories. For individuals who inherited retirement accounts prior to December 31, 2019, they are still able to stretch the RMD over their lifetime, and the required minimum distributions must begin by December 31st of the year following the decedent's date of death. For individuals who inherited a retirement account after December 31, 2019, the New 10 Rule replaced the stretch option. For the full list of rules, deadlines, and tax strategies surrounding inherited IRAs, see the articles listed below:

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.